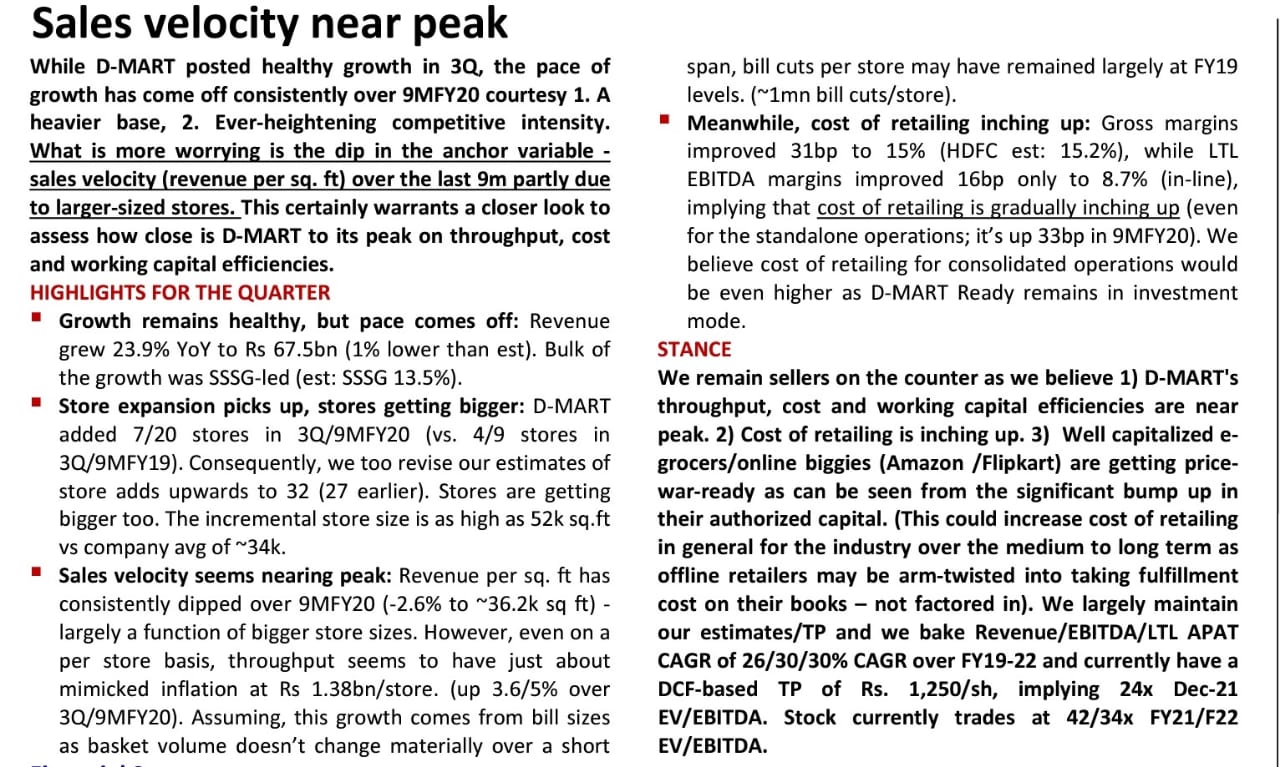

I have no interest in D-Mart given the stratospheric valuations. Came across this extremely brave SELL call on HDFC Securities research report (publicly accessible) - hence sharing a snapshot from the same

Avenue Supermarts (SELL)

Rising competition to hit margins, valuations

Target Price Rs 1,250 (25x Sep-21E EPS)

CMP Rs 1,926, MCap Rs 1,207bn

WHY

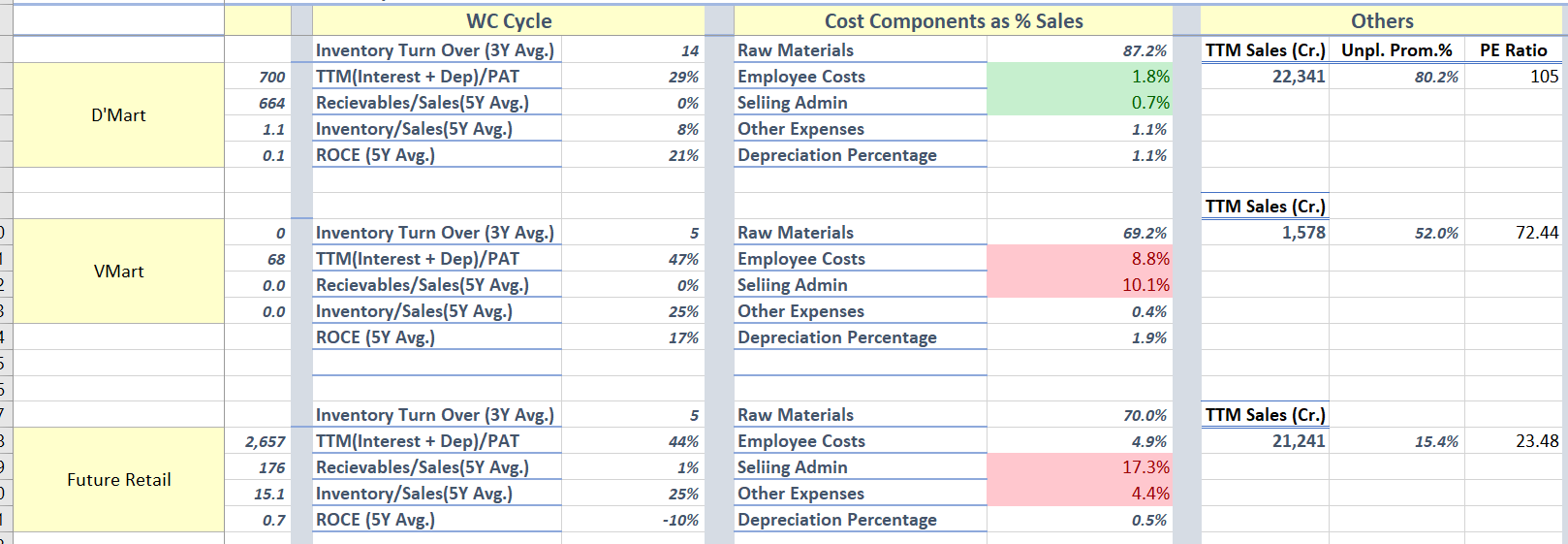

Select e-grocers closing in on D-MART’s key proposition – Pricing: While D-MART continues to remain cost/price leader in F&G, E-grocers have been closing in. Interestingly, this doesn’t come at the expense of deteriorating economics (trading margins for the latter have improved). Online biggies getting battle-ready too: Amazon/Flipkart have bumped up their authorized capital significantly in FY19 to Rs.35/18.5bn. We reckon most of these investments will find their way in supply chain and pricing as

both aggressively acquire customers. D-MART will have to defend turf. We are building in flat EBITDA margins over FY19-22E despite rising scale

Expansion target seems on track, there is a need to rev up run-rate: DMART is on track to add 27 stores in FY19. However, more needs to be done on this front as key peers have stepped up expansion. Our analysis on 460+ districts suggests that achieving/maintaining sales velocity in new

stores may be a challenge

Stock supply to weigh on performance: Per SEBI regulations, the promoter group needs to reduce stake to 75% by end FY20 (currently ~80%). With a QIP on the cards, supply will challenge already punchy valuations.

Valued to the moon and back: At 39x Sept-21 EV/EBITDA, there is just too much implied growth and its longevity, especially as competitive intensity rises in F&G. We build in revenue/EBITDA/APAT CAGR of 25/28/28% CAGR over FY19-22E. We assign a DCF-based TP of Rs. 1,250/sh (implying 25x

Sep-21 EV/EBITDA)

WHY NOT

Big peers such as Amazon/Walmart (via Flipkart) may struggle with assortment selection, trading margins and cost structures in the medium to long term.

With low float, the stock can command high valuation premium.

Link to report - https://www.hdfcsec.com/hsl.research.pdf/New_Year_Picks_2020_HDFC_sec.pdf