While a lot has been consistently debated about astronomical valuation of D-Mart.

Let me put across my 2 cents based on the future projection as guided by my Guru(would not take name)

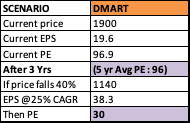

Lets say DMart which is at current price of 1900 falls down by 40% in 3 years( as most of the value investing folks say so) and Earnings grow by 25% annually. The 3 year earnings growth is 41%, so 25% is a very conservative figure; mind you Govt is after Amazon and Flipkart to to curb their discounting part(Bezos is in India tomorrow and read the kind of small retailers lobby/protest), if there are no online discounts, people will flock to D-Mart to buy their stuff, which I am sure is going to happen in a 1-2 years.

So,here is my calculation below. PE of 30 for D-Mart at the end of 3 years , a below average Jyothi Labs has a PE of 28 as of today.

I rest my case here

Disc: Invested but not a big part of my portfolio…

25% CAGR on profit / eps is what I think they should achieve…

So EPS after 5 years = 38.3, however if price remains at 1900, that means 5 yr forward PE of 49.60…

Only problem here is, that, may be we are buying 5 years early… I won’t say it should fall 40%, but I am in the camp who think it may not go up much for 3-4 years either… Take reliance (2008-2016), ITC (2016-??), HUL (1997-2010) to quote a few… there are many other examples…

On very high level I see a major flaw in HDFC analysis where they have considered only 27 new stores in current FY (they have already achieved 20 till Q3 and historically they do more in Q4). Moreover the report is considering only 30 new stores in each of next two financial years. We may agree that if new store addition gets capped and they can’t add new stores then certainly they will loose the premium they are enjoying. I am not sure why the HDFC analysis has projected this.

The analysis shows free cash flow of around 7000 Cr by FY 2022.

And the analyst brings down PE to 50x by FY 2022 itself.

While HDFC has given targets of 1250, we have other analysts predicting target of 2200 also

At the same time the real opportunities lie in deciphering hidden levers in a business model

Consider the huge footfalls it generates every single day which brings in the options to cross sell margin assertive products such as household utensils of different steel grades

The stores it own and the better rates at which it can get future stores at decent rates in slowing real estate. The future residual value of these properties and the ability it brings in to lower costs in uncertain future times

Increasing purchasing negotiable power with Biggie’s with improving scale of sales

Conservative and risk averse management

The advantage of low cost best value proposition and customer ring fencing it brings in especially in tough economic conditions where customers scout for best value propositions

Don’t go too far, There shall be benefit of tax cut to 25%

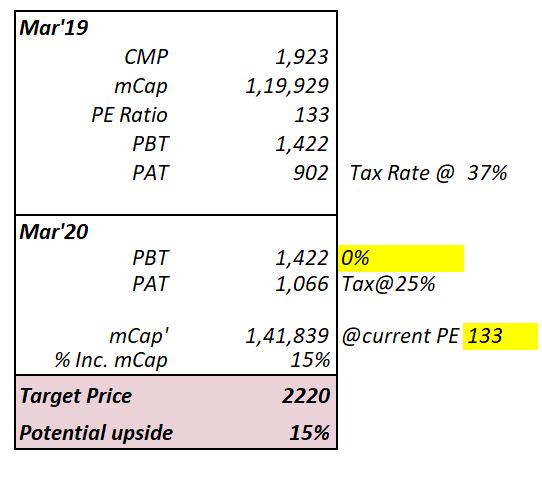

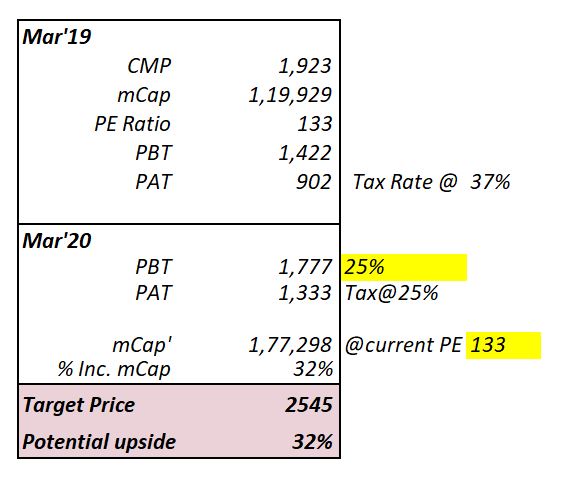

If one believe that the PE of 133 at current price 1923 is justifiable, then the fair price should have been at Rs. 2220. And if there is PBT growth of 25% in FY’20 them the fair price should have been Rs. 2545 at PE of 133.

DMART is always a contrarian bet (not low pe/pb wala) where all the Analysts and so called value investor have sell rating and it is preferred to be remain the same which will reduce the volatility of stock and also good for long term for the stock .

As an exceptional company need loyal customers,loyal employees to grow, in same way they need loyal investors also who have long term mindset ,not the myopic mindset ones who always emphasize on short term thinking and give more importance on PE more than it deserves.

Let us focus only for long term, not any short term price target based on PE.

If fresh shares are issued to reduce shareholding you may see about 5% dilution.

If the promoters sell via block deal,there will be no dilution.

All this depends on whether the promoters feel the need for additional equity,

even without that,the business is chugging along nicely reinvesting the existing cash flows.

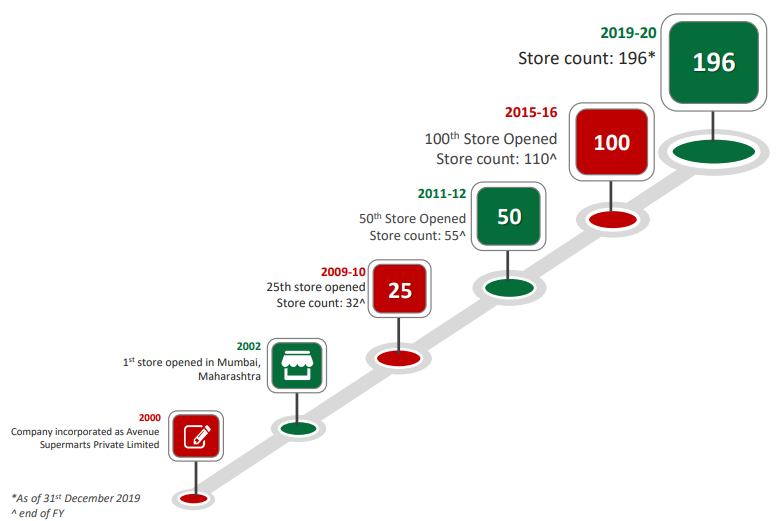

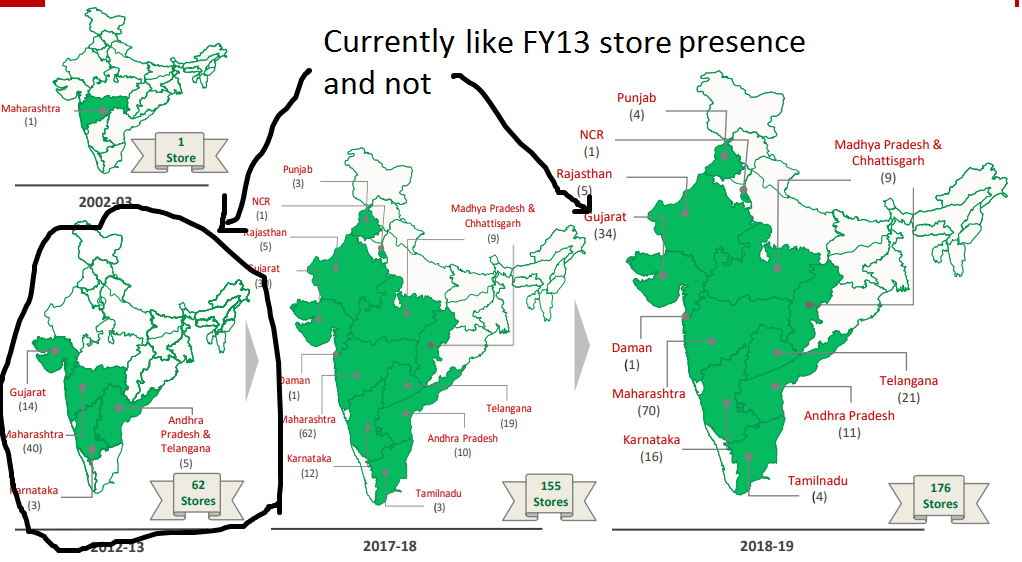

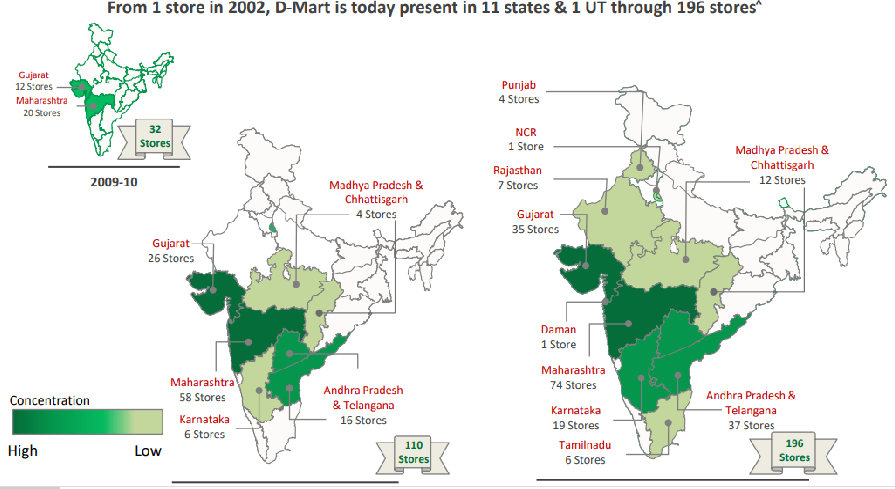

They started from Maharashtra + Gujrat and had 32 stores in 2009-10, expanded to 84 stores by 2015-16 & currently have ~110 stores by Dec2019. Total stores have gone 3.5 times in 10 years

Karnataka + AP(including Telangana) came next and had 22 stores in 2015-16, which has grown to 56 store by Dec2019. The addition seems to be following similar path of Step 1 (Maharashtra + Gujrat), although at a faster pace.

Next set of states seems to Tamilnadu + MP(including Chattisgarh) + Rajasthan, which has 25 stores by Dec2019

Above illustration shows that management has clear strategy of store addition and we can trust that fourth set of states could be Punjab + Delhi(including NCR)…

Looking at overall store addition … they achieved 25 stores mark in 2009-10 (ended FY with 32), reached 50 in 2 years. From 50 to 100 they took 4 years & again doubled (100 to 196) in next 4 years… so they have increased the pace & hope they continue same to reach 400+ in next 4 years

Other than above the financials including like LFL growth has also seen a uptick (although minor), which is major boost and augur well for future growth.

I feel that Avenue Supermarts is one of a kind company and the valuations reflect that. I will stick my neck out and say (sorry without any excel sheet analysis) Avenue Supermarts is IMHO is undervalued.

I guess there was never a doubt about the size of the addressable market, but how fast they grow!

Grocery retail in India has seen quite different kind of evolution than in most western developed countries and China, where organized retailing started with F&G in supermarkets and hypermarkets. F&G retail size in India is ~ 2/3 of total retail market and has an organized share of just ~ 3%. (Ref. HDFC Retail Sector Report).

I believe Indian populace still prefers to shop from Kinara shops (local mom-and-pop shops) and so these stores still hold sway, despite all the onslaught from offline and e-grocery players.

So, IMHO DMart should also trial the Convenience store format as well, if not doing already. Walmart have been experimenting with these formats for long. Spencers’ also has convenience formats.

I read that getting large space to open a conventional DMart store is getting tougher in metros. So, they should try this small sized Convenience store format at least in those places.

It’s a tough game to crack, since even Walmart is unsuccessful in US so far. However, Indian demography is quite different than US, and with more local knowledge Dmart should consider this foray worth attempting.

And, if they somehow get the formula right, we can be sure that Dmart will be able to maintain its super growth rate for many decades.

Doddaballapur is an industrial town with majority of people as lower middle class and rest as middle class

region has industries like Wrigley, Tata Steel, Bombay Rayon, etc.

region does also have huge apparel market with local people + nearby town people being employed there

upcoming largest IT park of Karnataka

Can this be termed as a refreshing switch from cities to districts with target segment? Or may be cities + districts? Are we looking at 2 verticals of Dmart [City Specific & District Specific]?

This is the reason why it’s extremely difficult to value some businesses with traditional DCF models. Longevity of growth and management‘s ability to experiment with new business models with min. cost impact is underrated. If in the long run, they manage to have the presence across the value chain I.e. Hypermarkets (large consumers), Cash and Carry (B2B) and C stores ( small ticket customers), this will take it into a different league altogether.