Not much details mentioned in that news. I’ve seen retailers do such things for older stocks when the newer stocks have higher MRP. Would like to know if similar thing happened in this case also.

Even I couldn’t get more details but considering Dmart, it seems unlikely due to following

-

They don’t buy/ keep/ stock old inventory as they have a policy NOT to but old stocks (mainly considering expiry)

-

Cases were registered against the outlets under Section 18(2) of Legal Metrology PC rules 2011, I understand that they must cross check such silly things before filling case

The growth for Reliance retail shows available scope for other retailers (D’mart etc) as well… interesting study

I had gone through HDFC Sec report on Reliance Retail. Do read it. Has some interesting facts.

My observations are

- 40% of their sales are from 2 businesses. Petro Retail and Connectivity (don’t know exact details but this must be related to Jio distribution). Both these businesses are very low quality. Petrol business margin is below 1% and Connectivity fetches 1.5%. Both are comoditized businesses.

These two segments deserve max 3X EV/EBITDA valuations. HDFC Sec report aggress on this.

-

28% of sales comes from consumer electronics (Reliance Digital). This segment is doing well currently and contributes most to EBITDA. This is vulnerable segment and is already facing stiff competition from online players. World over offline consumer business is going out of favor.

-

Grocery retail gives 23% of sales. They are doing fine but go through any scuttlebutt on competitors and D-mart comes far ahead.

-

Fashion retail contributes rest of the sales (8-9%). This is best of their business and is doing very well on growth and margin front.

Overall we can’t compare Reliance retail to D-mart or any other company in market. Only way to value the business is SOTP. And when you come to it, you realize that 40% of business is crap. Another 30% is okay and only 30% part is worth it’s weight.

If we say valuation of D-mart is very expensive, 5L cr for Reliance Retail is a joke irrespective of whatever the unlisted market saying. Let’s see what happens when IPO is finally out and listed.

23 Likes

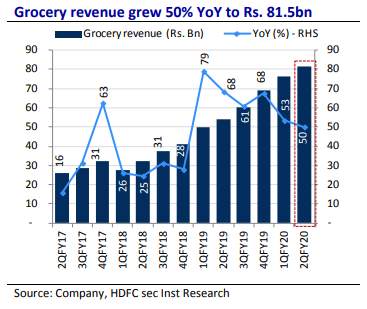

It makes more interesting as Grocery segment of Reliance Retail is growing >50% YOY

Grocery contribution in topline of Reliance Retail is 23% which translates to approx 27k Crore (FY19). Dmart is very close having 20K. Don’t we see scope of growth in this segment? The challenge is maintaining the margin & we have seen that D’mart is able to protect it with minor variations.

1 Like

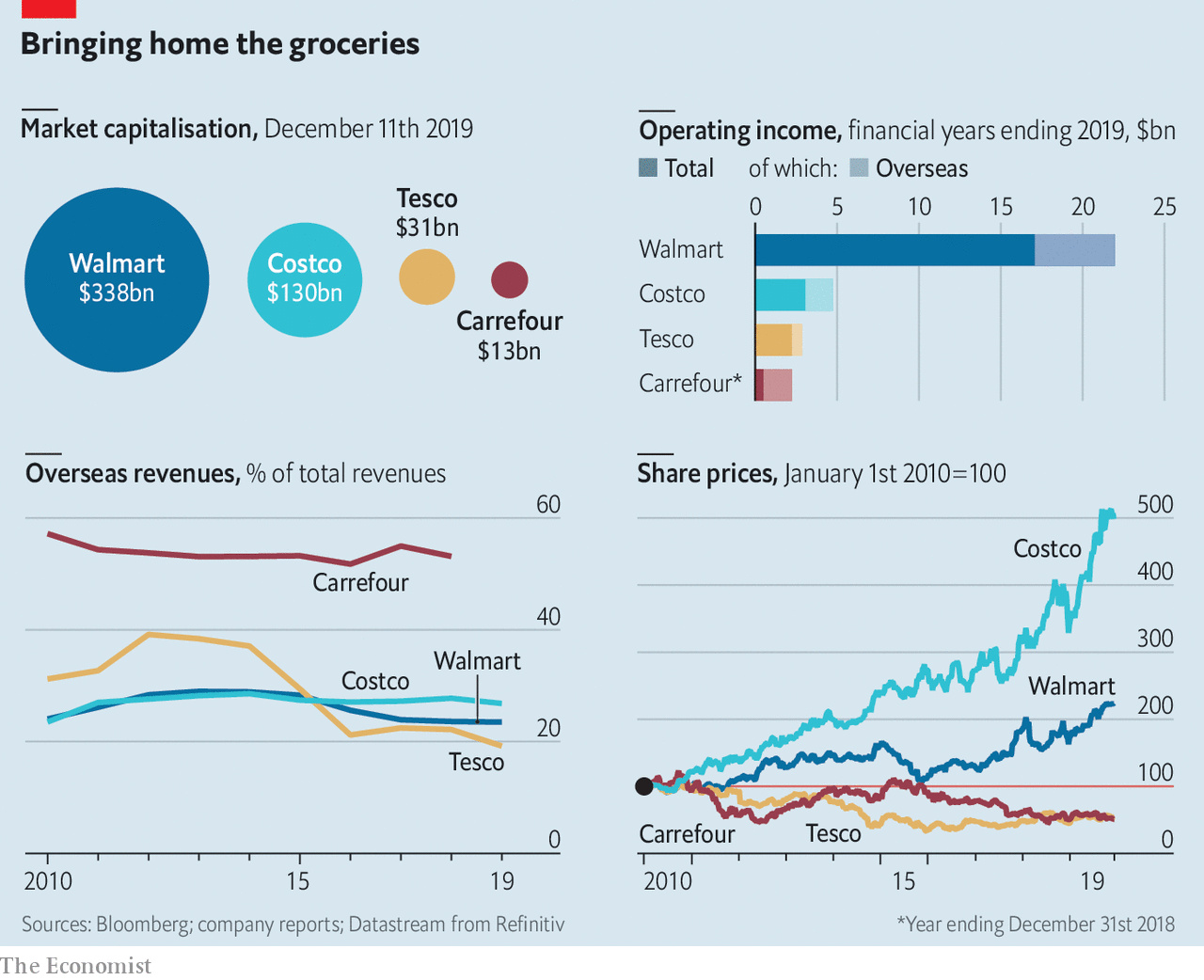

Pleasantly surprised to find an article on Dmart in The economist magazine

Somewhere it states that theres a delay in payment to suppliers , however this could be a one off i guess .

5 Likes

Again surprised to found that Dmart is having mcap of $16 billion [as of December 20, 2019]; which is more than Carrefour.

2 Likes

Here the size of untapped mkt is also greater

Also there are many comments on overvaluation, below quote to gain a balanced perspective

"On my time horizon, the calibre of a company is much more important than its value. You can be wrong about value in the short term, but still have a great investment over time. My worst errors have come from overestimating a company’s business model, not overestimating the worth of a fine companies " - Nick Train

Disc- invested . Not a sebi registered analyst

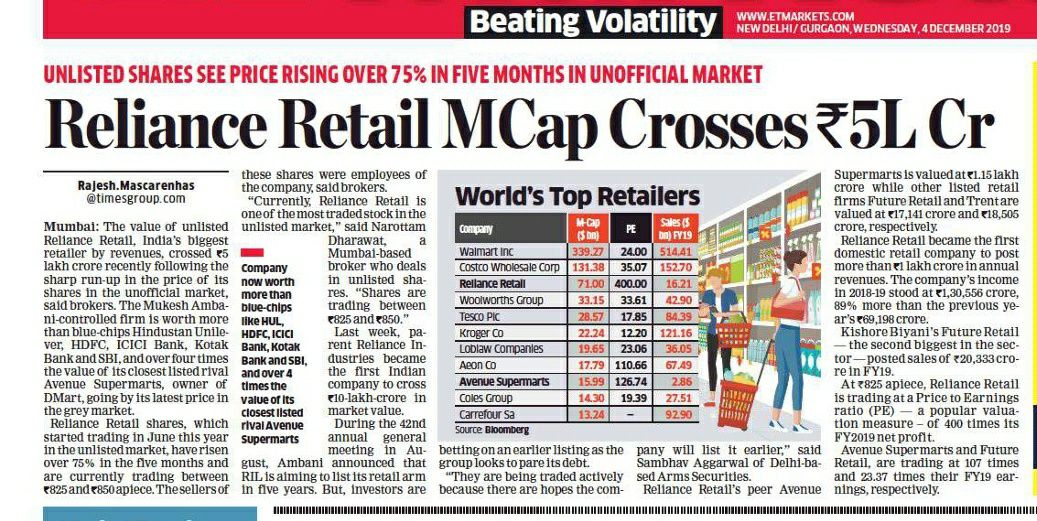

RIL has proposed swap of unlisted Reliance Retail with RIL shares. The swap valuing the retail business at double that of nearest rival D’Mart. Under this proposed scheme, Reliance Retail shareholders will get one share of RIL in exchange for four shares of Reliance Retail, details of the arrangement uploaded on the RIL website showed. The swap ratio values the retail business at Rs 2.5 lakh crore. Approx six months back, even Grey markets used to value Reliance retain at similar levels.

The report

On an qualitative basis, One needs to visit DMART/More/RR/BB…you feel why DMart is marching ahead…

1 Like

Indeed, this is in of their most differentiating factor. What would stop other players replicate this? Specially deep pockets ones like the Tatas…once you know the business volume and have control over your inventory and set up the cycle for your store, you can gradually work to get to what dmart does…i am no retail expert, would be great if someone could explain why others are not able to achieve this? Thanks

In fact this is the most difficult to replicate. My close friend who joined D-Mart in 2007 as a floor level executive retired in 2018/19 with three houses and own business, He used to say that D-Mart used to clear supplier dues in those days in 48 hours. If that was so easy to replicate why did not the others follow that example? Their ability to do so might be the outcome of running a very tight ship. Probably they are cutting costs elsewhere so as to improve cash flows to enable them to pay their suppliers on time. Basically they are not dependent on their suppliers’ money for their own working capital.

The other could be culture. There are individuals who borrow money and feel nothing about it. Then there are others who borrow money and will not have peace until they repay it. The former type can replicate the behaviour of the latter for some time, but cannot inherit the motivations of the former. In a company also D-mart might have begun with the premise treating the supplier with respect and that culture percolated in the company and has become their culture. In fact cultural changes are difficult to bring about.

I have been to TATA stores and they are no match for D-Mart in the current format. Tatas may improve. Like Westside. But Westside is a different category. I’ve been to Reliance and I stopped going there. The idea of grocery shopping is that you get the maximum number of items you want for your house from one store. For us it is D-Mart and for many of our family and close friends it is D-Mart. Reliance has been there in almost all localities of Navi Mumbai for about 5-10 years. So they have cracked open the marketplace. D-Mart comes along and takes away a significant chunk of the business. Because of its size Reliance needs to open more stores to grow by a certain percentage say 20%. D-Mart can choose to open a fewer number of stores for 20% growth. So they have little more wiggle room.

I personally feel D-Mart is doing a lot of things correct which are all coming together to create a smooth machine. Basically there is a multiplier effect. Every successful company will have their own set of gears which come together to form an efficient system.

21 Likes

Mohnish Pabrai talks about this:

Mohnish models – Started with Tom Peters who was “Jim Collins” of 1980s. Manager guru, wrote several books including In Search of Excellence. One story stuck out to Mohnish - the Gas station story – Two gas stations were diagonally across from each other, both self-serve. At one of the stations the owner would come out once an hour and pump their gas, clean window, service, at no charge. Owner across the street sees and says this is stupid you cannot do it for everyone, why do it for anyone? This manager never made changes. Over time guy providing extra service got more business. Competitor still had no change in behavior. Tom Peters said you can lay out your trade secrets completely to competitors; it will make no difference because they will not listen to you. Mohnish said he would prove Tom wrong by 1) forcing self to take ideas from customers and 2) I will observe in business when I see examples of people quoting good ideas. Mohnish gave competitors candid answers for how he was doing what he was doing and they haven’t acted on his comments.**

15 Likes

The question is more about what you as an investor will get after buying companies at such valuations. One should have a clear picture of this, especially when buying for long term at current levels. No matter how good a business is, at expensive valuations, there is not much juice left for new investors. Simply believing that the stock will continue to quote at such expensive valuations is pure speculation.

You can write all positives for a company like Dmart, but all of those positives should reflect in one thing only- earnings and its growth relative to the price it is trading at. Because this is what that ultimately matters.

4 Likes

The entire dmart thesis is predicated on how long it can sustain its growth rate. If Dmart can grow its earnings at even 15% for lets say the next 30-40-50 years (which is possible with a business model like Dmart), then it’s a good value buy at these levels. If not, then it may not be a good investment. While a lot of growth is built into the price however if a business can sustain a good growth rate for 5 decades into the future then it’s a different question altogether as there are vanishingly small number of businesses who have achieved that feat.

In the former (where Dmart is a value buy), hyperbolic discounting is at play. In the latter (where Dmart is ridiculously priced), extrapolation is at play. Both biases are valid. People have lost out on investments that appeared expensive but continued to grow their margins and topline for decades and have also suffered when past growth rates were extrapolated into the future. On the balance however, I feel that people have suffered more from extrapolation rather than hyperbolic discounting.

16 Likes

Hi Bheeshma

If Dmart grows at a modest 15%, even then it will take 20 years for the earnings of the company to catchup with the current price. And I haven’t taken inflation into account in this. If I take an inflation rate of 7.5%, then it will be nearly 31 years. Yes, 31 years just to get even with the current price levels! I dont know how than can be a good valuable buy and also a lot can change in 30 years time period including inflation.

Good thing is Dmart has grown at a rate much higher than 15%, even though past 12 months has been relatively poor (@12%) but the company in the past 5 years has posted a solid 40% growth rate. So the business definitely has the capability, but there is only upto a limit a business can continue to post such numbers. There are things that are beyond company’s control like the current slowdown in economy, logistics and infrastructure needed to expand into smaller towns etc. and current price levels are not leaving any room of error.

1 Like

Hi @Abhishek16

As mentioned by you a lot of years of growth are built into the price so that is the part which makes it a really bad investment at current prices.

The other part is a good growth rate for decades without employing too much capital.Its stores are such that once they are in place they will not need to be replenished. So once its store addn slows down then it will have considerable excess capital which hopefully it will share with shareholders while still maintaining its growth rate. A growth rate of 15% with 100% capital retained v/s a growth rate of 15% with lets say 70% capital retained makes a huge difference to the exit PE. In the former the ROE is 15% (15%/100%) while in the later the ROE is 21.5% (15%/70%) Ofc as mentioned by you there are many unknowns which are not possible to predict

If all these things pan out one can expect a reasonable return (15% types at current CMP) provided one is willing to go through large periods of underperformance and exercise commitment to hold onto it forever. These are things which are quite difficult to achieve

On balance, while i think there is still value on the table, but now there are also many ifs and buts. Those who got in early have been rewarded amply but at the current CMP extrapolating the past growth rate into the future may not be rewarding.

Best

Bheeshma

12 Likes

Mr Radhakishan Damani seems to be investing heavily in real estate.

As per report, Damani may be looking to raise Rs 5,870 crore through sale of 5.2% in Avenue Supermarts. Damani has to sell more shares before the end of March to meet a minimum requirement for public float.

On other hand Reliance retail is ready with it’s JIO Disruption technology.

JIOMart app is not only connecting consumers, but also enabling kiranas to order at wholesale rates from Reliance’s cash-and-carry stores, Reliance Market, to refill their stocks.

At present, the web portal is offering pre- registration discounts of Rs 3000, claims to have 50,000 plus grocery products with free home delivery and no minimum order value, no-questions-asked return policy and an express delivery promise.

Let us see its impact on Dmart.

2 Likes

Dmart Sept 19 Total Number of share was 61,09,43,380 where Promoter Holds 50,05,47,156 (80.21%)

As per latest ESOP announcement , Total Number of share is 627,774,691 means promoter holding is now 79.73% . So by March ,promoter need to do QIP or OFS to reduce the remaining 4.73% holding . Due to ESOP , 2.75% EPS dilution already happened from last quarter.

1 Like