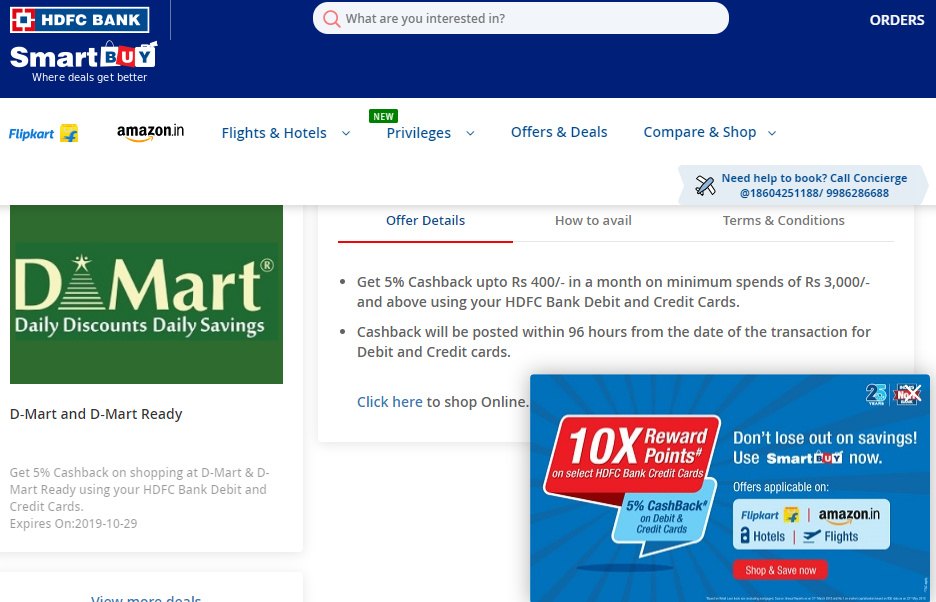

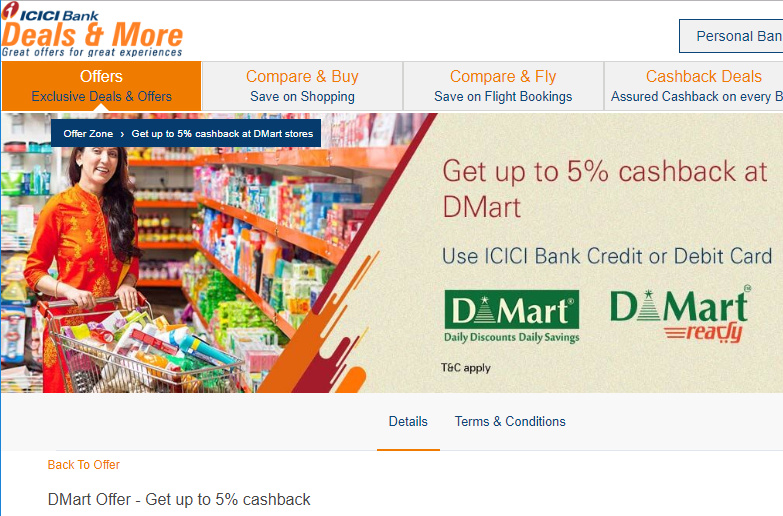

During recent visit to D’mart store, I could see promotions from ICICI / HDFC banks offering 5% extra discount on bills. I understand that banks bear the burden of such offers & D’mart is NOT going to loose anything with this. It should attract more customers. Posting here because I haven’t observed such promotional offers from D’mart earlier (a change from existing behavior where D’mart keeps away from such promotional activities)

If other community members see such change with a different angle, please feel free to share

We have enough of the examples and quotes of famous investors from you. Its time you came out with some original insights of your own which are relevant to the topic under discussion.

You can check the valuations of BF and Dmart since past few years (since listing in case of dmart) and come to your own conclusions.

If you still have anything against expensive companies I suggest you come out with specific post arguing against it. We have had enough of Ben Graham quotes till now and its time we had something meaningfully original from you.

In case you dont know, even Warren Buffett changed course after getting some gyaan from Charlie Munger and gave up the well trodden path laid out by Graham.

We cannot keep playing the same flute in all musical concerts. If the concert is a classical music concert, its okay but in a disco it wont work. Hope you get my point. That will save us from deleting a lot of posts.

just to add to the discussion, the high PE stocks trade at around 70-110 PE and there is a reason for the same. An HUL/ Titan/ Dmart can easily increase the prices of their products with nominal loss of revenue which can increase the EPS multifolds. But the prices are kept such that no new player can compete in the market at the same level. The advertising costs for Titan and HUL are excessively high. assuming if they even cut down advertising costs, their eps goes up manifold. the stocks where PE is excessively high also takes into account the entry barrier that these companies have created. for example, a friend bought a USB cable in a dmart pickup store at a price of Rs. 49 (mrp was rs. 149). they can easily increase the selling price to Rs. 59, which might just about nominally affect their revenues, but the increase in margin would be quite significant. (assuming the same applies to other products). Therefore, PE may not be the adequate parameter to value such companies. If you delve deep into the story of the stock, you will find that there are multiple reasons for the same (high entry barrier, brand name, etc.)

Disclosure : invested only in DMART. Not titan or HUL.

Why does Dmart sell at 165 PE at one point and 85 PE at another point? Why did an Hindustan Unilever always sell below 40 PE during 2016 and prior to that. And why did Titan sell at 50 pe during 2016 and some years before that? And everyone was dropping Bajaj Finance a few months back when it went to 1800 levels.

There is a special situation prevailing in the market during which quality sells at a premium. This is part of a cycle. When small caps rebound as they one day will, premium paid for quality will be curtailed. What is good and great today, need not be so tomorrow.

No doubt Dmart can increase prices and raise EPS. They can also collect membership fees like Costco. When market thinks like that they sell at 165 PE. When market is depressed they sell at 85 PE. Do you expect me to believe that? I would rather like to believe that it is a play of the operators, since the free float is so low.

Agree that in uncertain times people flock towards quality.

5 years mean PE of Indian retail companies are around 75. Trent at 125 PE is even more expensive on PE metrics. Also, high quality companies always tread at super premium in Indian scenario [e.g. P&G Hygiene, Nestle, Gillette, 3M, Honeywell etc.]. So, there is no material reason to suspect operator play in achieving high PE at a particular company.

good you admit dmart is quality. BTW, what is your suggestion here. sell Dmart and buy smallcap like yes bank, dhfl, manpasand ?..if you buy non-quality…there is a possibility of going bankrupt also…any non-quality company can be a future dsq software, hfcl, unitech, dhfl…Also not sure how you calculate PE…165 PE for Dmart…when? current PE is ~65-70 times FY21! i am not going into debate of valuation here…which is more personal…if you are comfortable…buy it…if not…don’t buy it. Simple!

In the end you say “it is a play of the operators, since the free float is so low”… you might be right…again…no one is inviting you to buy it… You are right not buying it because you think its a operators play…others(invested ones) are right because they think this is one of the best quality cum growth cum huge opportunity size(for its business) company available…everyone doesn’t need to invest in same set of stoks to become wealthy.

dmart has doubled in 3 years. So have other high book value / pe shares. You enjoy doubling in 3 years. I am happy to hold at CMP. and getting 15-20% p.a. to each his own

I request everyone to stick to discussing the business of dmart on this thread rather than rebutting someone’s views. They might be his own views and he is entitled to hold them at the cost of not littering this thread with repetitive posts.

So lets not take the bait and keep arguing and stick to what is in all our best interests which is to discuss what matters rather than keep trying to prove a point. There’s no end to these kind of arguments and nothing worthwhile comes out of it after a point.

In my view, one should realize that retailing and more broadly fmcg in US is fundamentally different compared to retailing and the fmcg business in India. In India we have an MRP system on almost all FMCG branded products which is absent in US. MRP changes the nature of how business is conducted compared to US. There are so many other structural differences in how retailing is done in US and India esp how customers pay for the stuff they buy. Our food habits are hugely different and vary from state to state and city to city.

As regards PE multiples, for a business like dmart they need to be evaluated based on how one thinks the future will unfold in the next 30-40-50 years and not trailing multiples. It’s a well discovered business everyone knows about it and knew about it even before it was listed.

If anyone is invested in dmart my suggestion is to give it a long rope and put a stop loss at an appropriate level because quite clearly it’s in a separate bull run of its own

Avenue Supermart; A Compounding Machine was how Shochis the member initiated the thread. I don’t have much to add.

Yes we can compound our capital. Sustainability, speed and rate depends on ‘many things’ ( which we know and which we don’t ) .

Broadly, here are my questions/conclusions

Are there any surprises in the Co.

( As earlier pointed out by seniors in other threads, What’s yet to be priced in ) ?

What can go wrong/right ?.

( We are paying close to 100 times earnings )

If there are any upside surprise, we can compound little faster.

Just in case if there is nothing or even slight headwinds crop up, we may see a massive correction.

( Simultaneously this has to play out -

DMART has to get stronger and other Global Giants n local ones have to cede this space for massive upside in DMART. Which i don’t expect to happen very fast/easily.

( Markets may throw better opportunities or new exciting ones to invest ).

Please Note - Just went through some latest comments. Haven’t yet read the entire thread.

Nil positions. Views are based on present context. May change

D’mart extends promotional offers with Deutsche Bank. This is the first quarter when D’mart has started these promotional associations with multiple banks hence It will be interesting to see the impact of these offers on topline of Q3. I understand that bottom line is immune to these activities.

I am not good at micro level, but what I am thinking is, in this phase of asset light business models why is DMART not trying it out… ( Prefers to own stores )…And in times of negative yield… There is also the possibility of rentals to come down…

As per my understanding of payment partnerships it is not Dmart who would be funding these offers. It is usually the issuer bank and then the payment networks. It is almost always the issuer banks.

Such offers provide a tailwind to top line at no additional expense. So it’s always a win for the merchant in this case Dmart.

Issuer banks are chasing credit/debit card spends. I won’t be surprised that soon we will see all sorts of payment instruments not just cards offering discounts and cashbacks on purchases at Dmart.

Had a look at the 1979 Annual report of Walmart when it had around 225 stores. The pre tax return on starting equity for Walmart is 59% against Dmarts 30%. Clearly Walmart was a superior business. What got me by total surprise was that Walmart was valued at 15 to 20 PE by the market at that time. As I read the 1989 and 1999 report I gathered that Walmart doubled the store count every 3 years, doing a lot of acquisitions along the way, and growth slowed down significantly after it reached the 1000 store mark.

You need to see that in context of S&P 500 PE ratio which was around 7 at that time. So Walmart was trading 2-3 times index PE, it was a pricey stock of its time. Yet, you would have made better returns by investing in Walmart instead of index.

That said not all pricey stocks are backed by good quality business. Can you elaborate more on what made Walmart a superior business model?

I have already mentioned the reason why Walmart is a superior business. Warren Buffett purchased several businesses without even visiting them once. All you need are the financial statements of several years. With practice you will recognise a good business in a few minutes. Warren Buffett mentions that he usually makes up his mind in less than five minutes. High ROE, high ROCE, no or low leverage are some of the hallmarks of great businesses.

The problem with Dmart is its somewhat lower ROE and an investor only gets as much as the ROE. I studied Walmart’s accounts to check whether the ROE will improve with bigger size. But I found that the ROE got lower with increasing size. To get more returns the business has to dilute capital at high price to book. But based on the planned CapEx, Dmart is not likely to dilute anytime soon. And 17.5% growth is what investors will get. The present PE will be justified only if 1. Company diluted equity and/or continues the 17.5% growth for a long long time into the future. Disc: Not invested

I must have missed your explanation. Yes, Walmart maintained high ROCE for many years. My question is what enabled Walmart to maintain such high ROCE? Usually you would expect the competition to copy your business model, especially if your business is generating high returns on capital invested, and that would drive down the future returns.

Stock price is all about the future earnings. So it is not sufficient to know that a business have given high ROCE in the past, it is more important to figure out how it is going to maintain high ROCE in the future.

Logistics is one of the main reasons. Mainly Walmart avoided the competition and set up shop in small towns where the biggies were not there. They treated customers as guests and managed to provide the right goods at the right time and at the right price. They were also rapidly acquiring other competitors (small well managed businesses) as it is futile to set up shop, where a good competitior is already there.

People frequently ask “What is the next Walmart”?.. And the answer is, Walmart is the next Wal-Mart.

Dmart has been making news about all good things but seems they are getting into negative things & it could certainly lead to lost in reputation,which will certainly reflect in customer confidence & trust levels. Nobusiness can grow with such acts.Hope it remains limited to few stores & doesn’t spread across.