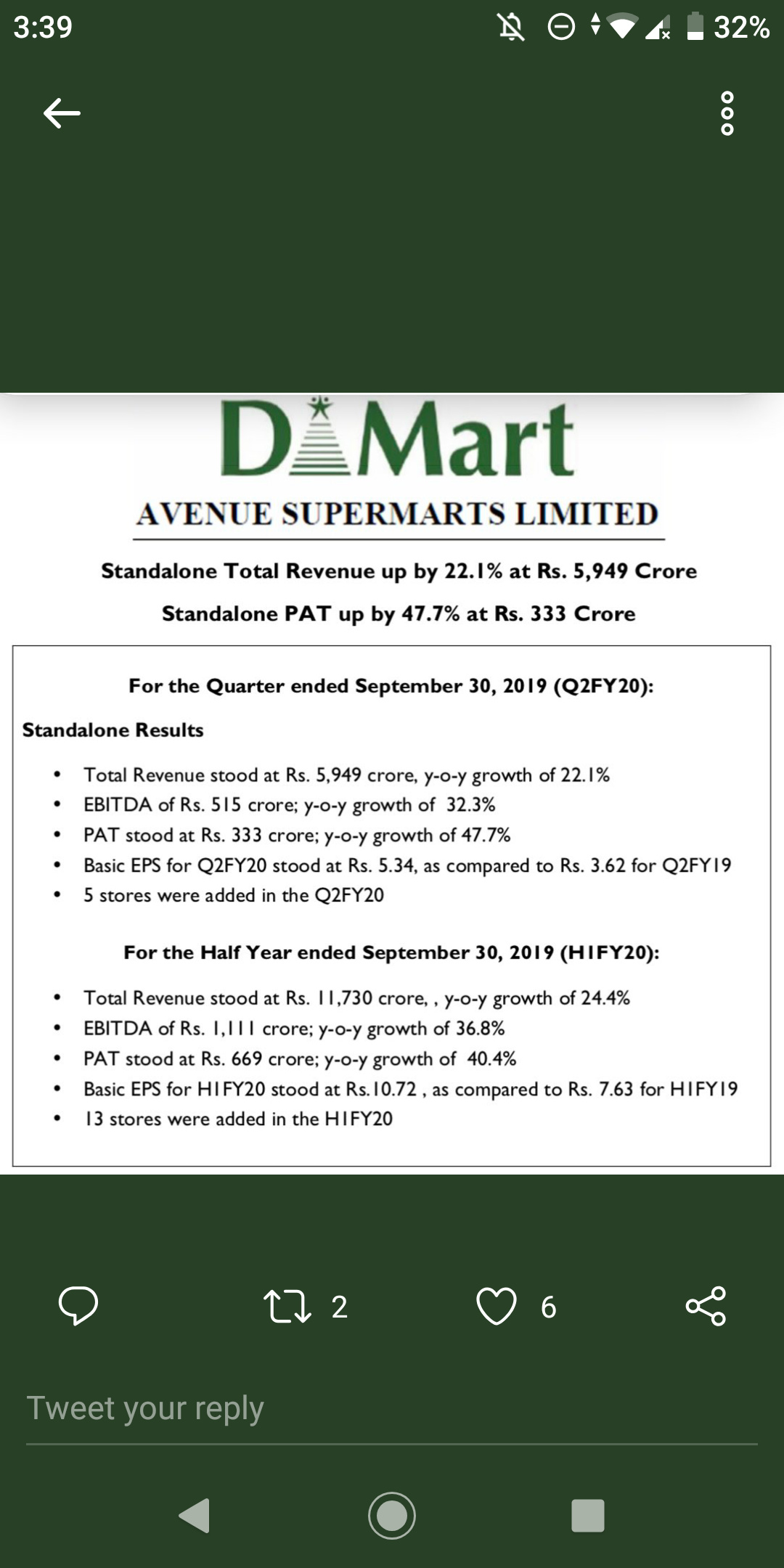

Q2FY20 result declared.

@bheeshma waiting for your analysis on this result, please.

Q2FY20 result declared.

@bheeshma waiting for your analysis on this result, please.

PAT looks higher on YoY basis due to lower tax rate, otherwise in line with revenue growth.

you need to check it from EBTIDA font. Higher D&A provisioning turning PBT at 21% level…

Commenting on the financial performance of the company Neville Noronha, CEO & Managing Director, Avenue Supermarts, said, “Revenue growth for the quarter was slightly lower than our estimates while gross margin saw improvement over the corresponding period last year due to better revenue mix. PAT margin improvement is in line with revenue growth and also aided by revision in corporate tax rates”.

The commentary of the management is revealing. Everything is going as per plan. As per CRISIL report a CapEx of 1000 crore was planned for this year. If the company is going to grow this way, they will not require any equity dilution in the near future. Warren Buffett has said that there in No company in the world with capital employed more than 7100 crores (one billion dollars) that can grow consistently at 20% or more with full retention. Hence growth of Dmart should slow down leading to PE derating.

@Julian ,The interview which you have posted is old one during 2017 DMART IPO after which DMART increased 3 times.

BTW , here is a snippet from the recent interview of RT when PPFAS invested in 2019 Feb in Amazon at 90 PE where he explained PE is not appropriate measure to judge valuation of great businesses like amazon.

Thakkar goes on to explain the rationale behind the investment. He also tries to answer queries like whether there is a drift from the approach of investing only in stocks trading at less than intrinsic value, what changed the stance, as in the past PPFAS Mutual has said that they do not know how to value Amazon.

“If one uses a typical metric of say price/earnings ratio, the stock looks very very expensive. We have been railing against expensive consumption related stocks in India for more than two years now. Amazon may seem to fall in the same category. The answer is that P/E ratio is not very helpful if the reported earnings are not ‘correct’ for some reason,” said Thakkar.

“The reported earnings may be ‘correct’ from the accounting perspective and indeed may have been audited by the best of the auditors. However, they should be representative of investors true economic earnings and sustainable. If the earnings are overstated or depressed due to certain factors, they give a misleading P/E ratio,” adds Thakkar.

In his note, Thakkar gives reasons why in the case of Amazon, the P/E ratio is not representative:

I believe alpha is the only truth in market everything else is narrative.

A very important reason for Avenue to keep doing well from a price perspective is it very low float in the hands of investors. So, in a way it is a stock which is pegged up due to lack of sellers which amplifies action of the minuscule number of sellers. This could continue for a long time as the promoters probably do not need capital on a personal level post the promoter holding being reduced to 75% as per regulation.

Opportunity size is large. So, Dmart can continue to grow at healthy rates for a very long time. A word of caution to those who are extrapolating the 1980s Walmart growth story here need to also factor in the changes in retail business that has happened in the last decade, including the aggressive advancement of ecommerce and the penetration of mobiles, payment systems etc.

It is a good business, run by very focused promoter and extremely able management. Valuation is rich but can remain so for a long time.

The call to buy/hold/sell has to be based on personal choice.

One way I have played such companies in the past is to buy a very small allocation - around 2% and then keep buying on the way up as long as the business keeps performing well. That could be a sensible strategy here as well for those who are interested in the business but are scared of valuations.

Disclosure: No holding. But like the business and watching. Could change my views in the future.

The interview of Rajiv Thakkar regarding Dmart was given in April 2018. Amazon for several years was making only revenue and negligible profits. In 2016 for example the profits were just 0.5 billion against revenues of 100 billion. Hence the real profit of Amazon is yet to emerge and the comments of Thakkar should be seen in that context. Perhaps IndiaMART may be in the same category but not Dmart.

In this dynamic world 6 quarters are too long and views of analysts keep on changing. During same period EPS has expanded (12.57 to 18.08) by approx 50% hence most of the numbers quoted in interview will need revision in current context else they give a false representation of facts based on performance of growing business.

It has been downgraded several brokers several times since ipo. Non believers continue to not believe but the stock has been rewarding pretty handsomely to the believers. People are clearly missing the big picture by focusing too much on the PE, period.

Dada , I am an amateur investor and not able to understand how averaging up works although I know for the fact that all great investors value on the way up rather than down . But doesnt that dilute returns as it brings the average up ? Request you to pls explain for amateur like me

Think simply. Say a stock is priced at 100. You buy some shares. Then it moves up to 120. You buy some more shares. Then it moves to 150. Buy few more shares. And so on. As long as you keep doing this and every purchase is the same or fewer number of shares, your average price will be lower than the market price.

Yes, the profits will be lesser than if you had bought all the shares together in the beginning. But, in a lot of cases, I have seen both with myself and others, that thet are unable to buy any shares. The reasons could be many - a perception of high price, some possible negative newsflow in the near term, some macro fear etc. In such a case, this is a very sound strategy because it slowly helps you build a position.

I personally use this strategy nearly all the time, because I like to buy stocks where I will be invested for many years (hopefully). Then, it helps to build the position slowly (sometimes over months). The more time I am invested the more I tend to know about the company because I am more engaged with it.

You can read an academic take on averaging up here - Average Up: Overview of the Trading Strategy

In Dmart I took the opposite method starting from 11th April to 8th may. I did averaging down starting from price 1477 to 1235. And luckily it worked for me. I like averaging down rather than averaging up. As @basumallick said it keep you engaged with your target stock.

Though this is not the right thread for this, but I will put in one comment and then leave it there.

Averaging down is a very dangerous strategy, especially in very overvalued stocks. History is replete with examples where stocks keep falling and the buyer exhausts his funds for buying more. Beyond a point, one ends up with no more cash and a falling stock price and declining holding power. I personally only average down if I am very very very very sure of the stock, which unfortunately, I rarely am.

On the other hand averaging up has psychological advantage that your market price is always higher than your buy price, so you are in profits. That is a huge mindset advantage to have.

Putting down my thoughts about corporate tax impact on D-Mart:

D-Mart may not benefit from the tax cut in the long run and may pass down the benefits to the end consumer. This is because it has no competitive advantage on the product front and the products it sells can be obtained at any mart.

Retailers with low footfalls might look at this as an opportunity and lower their prices to better their game. D-Mart which is respected for its lower prices will eventually have to follow them and lower their prices to stay respected.

D-Mart’s competitive advantage is mainly on the operations and execution front. This edge might still help them stay ahead of competition even few years down the line. But this is not going to help them retain the tax-cut advantage.

Request other VP-ers to comment on this regard.

Good point.

To make my case, I will like to draw your attention to the fact that tax cut will benefit higher margin business more. Say we have two business, A with 3% margin, B with 6% margin. If we have 33% tax rate, then for a revenue of 100, A gives 1% to tax while B gives 2% to tax. That means B gains more margin from tax relief. If you take the case where tax is completely waived off, A’s profit after tax margin increases by 1% while B gains 2%. Even accounting for increased competition, B can still retain the excess 1%.

The argument holds for all companies having low cost competitive advantage. In our case, Dmart indeed has the higher profit margins due to its cost efficiencies, so even accounting for increased competition, it will be able to retain some of the excess gains from tax cut.

In my view, this comparison may not be completely representative as the composition of the basket is very different for an average dmart shopper and the rest of the rivals mentioned here. Any comparison which does not control for profile and household income will not be reliable. Having said that foundational competitive strategy of dmart is everyday low prices and it is executing it well as it understands local consumers tastes and preferences well enough to stay ahead in the game.

Agree.

Surprisingly the comparison has escaped Big Bazaar, who always take their own desired sample basket & display the comparison with D’Mart in most of their locations

Such sample can be taken from any shop & obviously everyone wants to show them cheapest to attract customers…

In longer term these may not help as customers are intelligent & they find their own liking based on prices / convenience