I don’t see any issue in paying 1 rupee to get 2.6 rupees every year after 30 years.

Consider a case if all goes well and dmart earns 2.6 lakh crores profit, going by terminal pe 30 (india becomes developed country and risk free bond rate is 3.3 %) it trades at mcap of 78 lakh crores which is 78 times current mcap, still a decent compounder at 15%.

Yes there are still many companies which are currently compounding at 15% and available at better valuations

Thanks for pointing out the ownership bias! One of the improvement areas is how to get dissenting voices be heard on a thread which consists mostly of bullish people. I agree it’s a cause for concern. Most people who post on a particular cos thread are generally optimistic about its prospects and sometimes people who have a different view to the consensus are ridiculed for having it and worse they stop posting their views altogether on the thread. I think this impacts the quality of discussion very seriously and some way needs to be devised to prevent this from happening

I completely agree . Ownership bias is good till the time it can give constructive viewpoints but once a person starts taking things personally, it deters different views . I believe the reciprocal tendency bias ( tendency to reciprocate to personal attack) then works even more to derail constructive discussion altogether . I guess moderators can help

We are not considering risk margin as one may not be able to execute this feat for 30 years. If we expect 20% probability, then we may have to apply risk margin to reflect it. Lot of things can go wrong in 30 years. Walmart is unique and Dmart may or may not follow the same path.

The ESOPs allotted will come to 0.59% of the total share capital. If this becomes a regular practice, existing share holders will definitely get affected. The option price is just Rs.299 which values the company at 18 times earnings.

FMCG, Groceries: Resilient but under pressure

Fastmoving consumer goods, the third-largest category in terms of buyers, weathered the impact better than most, the report indicated. The number of online shoppers in the segment saw a 17% increase over 2018 with spending increasing 91% during this period. Discounting in the space also more than halved over the past year in line with other categories.

With no profits yet and higher and higher accumulated losses every year,the slower growth will be a very tough time for ecommerce companies. With models slowly moving towards making profits vs accuring cutsomers… discounts would further decrease I think going forward. relatively better times for offline retail probably.

Well esop is not like equity dilution for raising capital… Infy, Wipro, TCS and many across other sectors have esop schemes running for several years and I don’t think that market ever took these negatively. In fact, as an investor, i am happy that company is taking care of their employees (in addition to their focus on customers). These things help in building a great organization which can last long and is a positive in my view.

ESOP is worse than equity dilution. Warren Buffett who is the gold standard never issues ESOPS. In equity dilution, atleast existing shareholders are mightily benefited if shares are issued at several times book value. However in this case, equity shareholders will foot the bill and employees will anyway dump the shares in the open market for getting 5 times returns.

Its always good to have good employers but do shareholders agree that esop should be huge as 0.59% and worth 590 Cr ++ (We must note that Employee benefit expenses in last FY was 335 Cr Only.)

Are we happy bearing it if it starts happening every year or so?

I agree completely. I too like the company. However would have to rethink if esop are on a continuing basis

Yes but its equity dilution only as ultimately it increases the equity base . Current effect isnt material but if its regular , it isnt taken kindly by the markets generally. One cant quote examples of infy and tcs to justify dilution. I don’t say that it’s a issue currently. But one needs to take notice if it’s a regular practice and has material impact over a period of time irrespective of the business . I agree on employee morale etc it’s good but it has the effect of diluting base which reduces value to shareholders. However I believe it’s a fantastic business and management and hopefully they shouldn’t keep on diluting equity regularly but this thing is worth monitoring

Disc - Invested with small Tracking position . I am not a sebi registered analyst. Pls do your own diligence before investing

retailing is all about the experience of the purchaser and what he get in the return . The long term view of the company in terms of value creation to various stack holders viz employee ( noumber of employment opportunities and growth of individual is mandate ) is customer ( they are getting the discount )environment( they are reducing power consumption and water usage ), government ( they are getting share of the pie in terms of taxes ) suppliers ( increasing consumption of their product ) is seems to be good but not the best .

though they are thinking differently they use ESOP to reach the minimum public shareholding obligations of the Company as a method under clause (ix) of Annexure to SEBI circular no. SEBI/HO/CFD/CMD/CIR/P/43/2018 dated February 22, 2018. which is good but if thinking about retail investors they are at loss because they are diluting the shares via backdoor and hammering the value to retail investor .

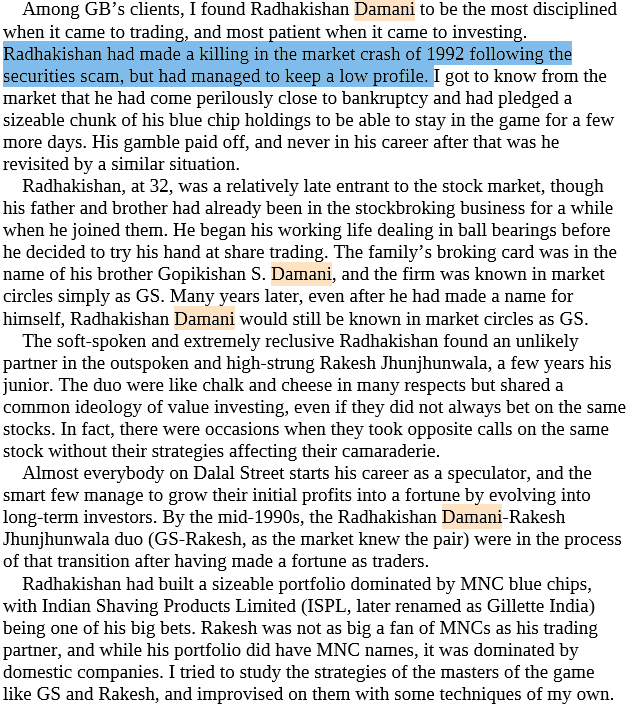

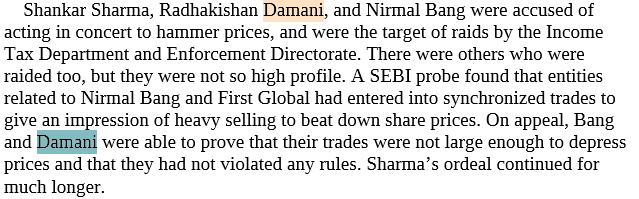

they may be some connection of pump and show as Damani being old fox in the game of the Share market has numerous connection in the investing circles .

I read in the book of Santosh nair

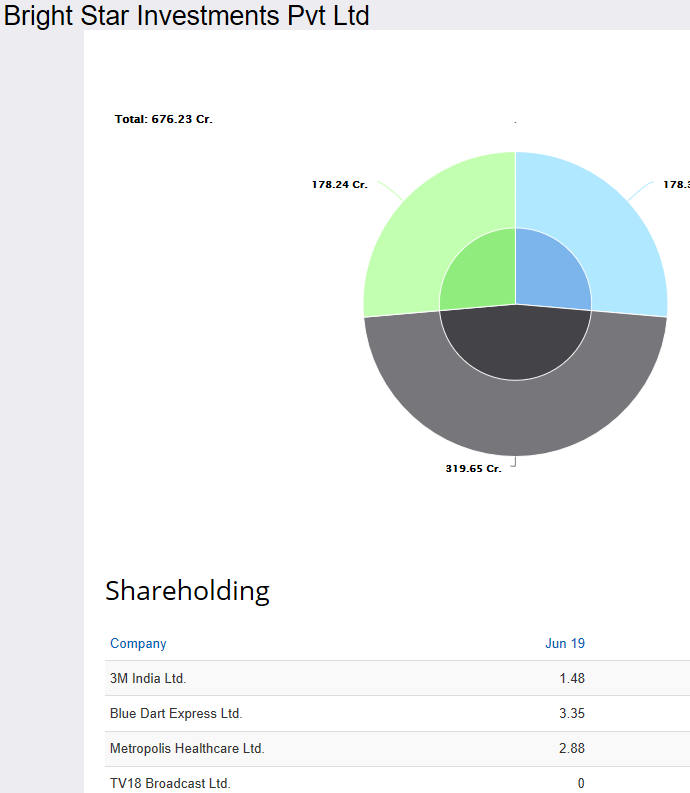

I try to find the details about avenue supermart or in bright star investments Company Not Found | Zauba Corp but not found the company’s details

disc : not holding and i am not sebi approved analyst

Good to see above information regarding promoter … we need to be aware of such information as performs balancing act … we need to understand that everything looks yellow to the jaundiced eye and if we don’t look in the past… we may get trapped.

On positive front I see that they have started utilizing approved NCDs which will bring down the interest expenses.