Since couple of days I am seeing the prices of some fast moving branded items expensive; but situation was totally different couple of months back for the same SKU’s.

Does this signify anything? Something like Dmart coming with more SKU’s under its own brand? Something like conditioning the mindset of customers? Something like focus on bottomline?

Very interesting points on Costco, appreciate the depth of the analysis. Few points - I used to be regular visitor of Big Bazaar (stopped few months back). They every time tried to pull me in their Profit Club which I always refused. Reasons were not just cost of membership alone. When I think deeper now, reasons were like - 1. Communication of the offer was not clear and it was like a sales push. Like selling credit card. Like most Retailers even in US do. 2. I would not say that Indians are not ready for this business model. I would rather say the retailers are not ready in India now. They do not know exactly how to get to this. 3. Level of trust was another thing and along with that the thought that I will stick to Big bazaar.

Also, you mentioned that in Costco you get only best product and only one option per product…this means couple of things and the most important to me is that Costco model does not involve private labels at all. Pls correct me if wrong. Business models of all Indian retailers - Dmart, Big Bazaar and Star are around private labels. These for integral part of their long term plan. None is focused on Costco type model even if India may actually be ready. Second important point is clearly Costco focuses on quality of discount and based on my personal experience with all Indian retailers so far, the best quality of discount I find so far is with Star. I am recent new entrant for Star as customer so maybe time will tell how good they are. Also, I feel if at all we see a Costco type model, it would be coming from stable of Tata or Reliance as a separate subsidiary. Dmart is too focused on quantity of discount and crowded stores to try this. At least not in medium future I would say.

As I would say we can have only one Walmart and one Costco in India also and not one which can be both

Disc: Have Trent and Dmart on watchlist. Looking for the right conviction level to build in

No sir, its best selling brand in most of the categories is it’s inhouse brand Kirkland Signature. From wikipedia - It accounts for almost a third of all Costco sales and is growing faster than Costco sales.

Trent’s Star Bazaar has opened a few months back near my house and I am amazed by the number of private label’s they are carrying. It’s Fabsta brand is there in most of the categories. I did not see so many public label in case of DMart.

Thanks for the Kirkland private label. Good to see it in Costco model. It reinforces my belief that Tata is closest to this model,at least now, when it takes of in India.

Tata is King of Private labels be it in Star or in Westside. Thats how Mr Noel Tata steered a profitable retail chain in earlier crisis

Key takeaways from analyst meet ( source : Edelweiss report) Strategic points

The company will continue to focus on profitable growth.

Consumers with monthly household income below INR50,000 are the company’s target

customers.

New growth avenue could be cash & carry; but its at an initial stage.

Value proposition of being low cost retailer maintained; but the gap with competition

has reduced since the latter has upped its discounting game.

Sales from FMCG branded products will be 40% and this is where all the competition

and discounting is happening. On balance items, essentially general merchandise and

apparel there is no price comparison.

In grocery, B&M has cost advantage and is a better model than the e-commerce format.

F&G is the least affected in online competition.

Compared to previous year, DMart’s investment in gross margin was higher in FY19.

E-commerce shoppers demand much more than DMart shoppers.

Focus is on expansion and conservation of capital rather than paying dividend.

Promoter has to reduce stake to 75% by March 2020. QIP has been announced and will

be driver to prune stake. Demand scenario

Focusing on improving the shopping experience within DMart stores.

SSSG uptick in FY19 was also backed by strong performance of new stores. Old stores

also posted decent single digit SSSG.

In new stores, volumes drive SSSG and in older ones value drives SSSG.

Profitability will be key criteria.

Revenue per sq ft incrementally can grow at inflation rate.

In Mumbai and other metros, sales per sq ft is significantly higher than INR35,000.

Will not look at membership program

Fresh has never been the focus area. It just doesn’t fit in to the model since management doesn’t see value in building the fresh business. It is a data-driven decision.

Whichever stores are seeing huge footfalls, management is extending operating time

for those. Initial traction in stores where timings have been extended is encouraging.

Does not consider staples as private label. Real private label can be in core FMCG

products. Very small currently in private labels. Will focus on private label only if quality

of products is superior. Private label is more like a 10-15 years’ story. Needs more good

quality vendors to scale up private label. Contribution is low single digit currently.

Whenever a competitor enters the city wherein DMart is already present, the revenue

run rate slows or may go in negative territory. But gradually it gains traction.

Discounting of 50% off etc, is a joint collaboration between brand owner and DMart. Product mix

In certain regions, DMart sells more apparel than core FMCG. Thus, in smaller towns,

the format makes more money. This is because general merchandise and apparel have

higher margins.

DMart has dynamic pricing between stores in same cities as well. The store manager

has the option to change pricing in a competitive scenario. Store expansion

Has a far better and stronger team to assess real estate for store expansion.

North is a new market for DMart. Performance in North is similar to Gujarat and South when it started in those markets.

Performance in South India is as good as Maharashtra market.

Will accelerate store expansion pace. Volatility in store expansion will remain since

permissions to open store are quite complicated and do not come easily.

New stores opened are of 50,000 sq ft against 30,000 sq ft in the past.

Some of the new stores have the option to expand in the future.

The company is also looking at long-term lease to speed up store expansion pace.

DMart is moving from extreme conservatism to controlled aggression.

Real estate prices have remained soft over the past three years.

Larger component of store expansion is through owning a property.

Finding right talent is also a challenge. Competition

Pie is growing rapidly and hence DMart is not worried about competition.

Wherever DMart has opened, not a single Kirana has shut down. This has happened

since retail ecosystem and size of market are huge. Margin

Happy with existing EBITDA and PAT margins.

Current gross margin of 14.5-15.0% is good enough.

Tie up with wallets has not worked in the past owing to volumes. The wallet company

ends up losing more money. Not looking to introduce its own wallet since DMart will

not focus on giving cash back, etc.

Logistics in India is not a hassle since DMart pays logistic cost for only one-way. Reverse

logistic will work only in small locations say 50-100km. For reverse logistic to play,

DMart will need to own the fleet.

Has not shut a single store so far. Broadly, a new store is opened in existing market, the

target revenue is achieved in 6-12 months. So eight year store makes pretty much same

margin as a new two-year store. DMart Ready

DMart ready format still in infancy. But FY19 has been better compared to FY18.

Seeing opportunity of scaling up this model in metros since possibility to open in some

regions is not feasible.

Very limited assortment and primarily doing only FMCG.

Average bill value of Big Basket, Grofers etc., is INR1,500. Hence, threshold of INR1,000

is here to stay.

Focus for FY19 was to get tech capability in place.

Now has 196 DMart Ready stores. Others

Within senior leadership also there is no excess KPI parameters.

Maintenance capex is limited.

Goldman Sachs added Avenue Supermarts back to the Conviction List for three main reasons. First, Avenue is likely to surprise investors on store additions. Investors have been concerned about Avenue new store additions, which missed expectations in FY19.

However, management was categorical about the company being well-positioned to accelerate store adds, with the delay in FY19 being due to regulatory factors.

Secondly, the company has significant room to grow SSSG through an increase in throughput per sqft or by increasing store area in areas where the cost of real estate is lower; and lastly, margin reset largely behind us.

Third, Avenue remains competitive on pricing while delivering strong returns. Its low-cost model is far more resilient to pricing-led competition than some peers with significantly higher operating costs.

Did management indicate this? I think this was main worry of market so far. Market is confident the revenue growth will be 30-35% for at least 3 years. If margin stabilizes, the PAT will be on same trajectory.

Milk is altogether a different ball game; and not at all an easy code to crack - where the major and only player is government dairies.

This government dairies calls the shots to build a fine tuning between supply [read: farmers] and demand [read: end users]. Many times [In fact, umpteen times] they raise the prices for farmers and on other end don’t raise the prices for end users; and at the same time squeezing the margins so that inflation for milk as a commodity is under control.

Moreover, as a second thought is selling milk 12% cheaper a scalable idea - because the supply [read farmers] is same which extends its offerings to Nandini, Amul, etc?

Now, you take decision whether it’s a smart move or me-too moment?

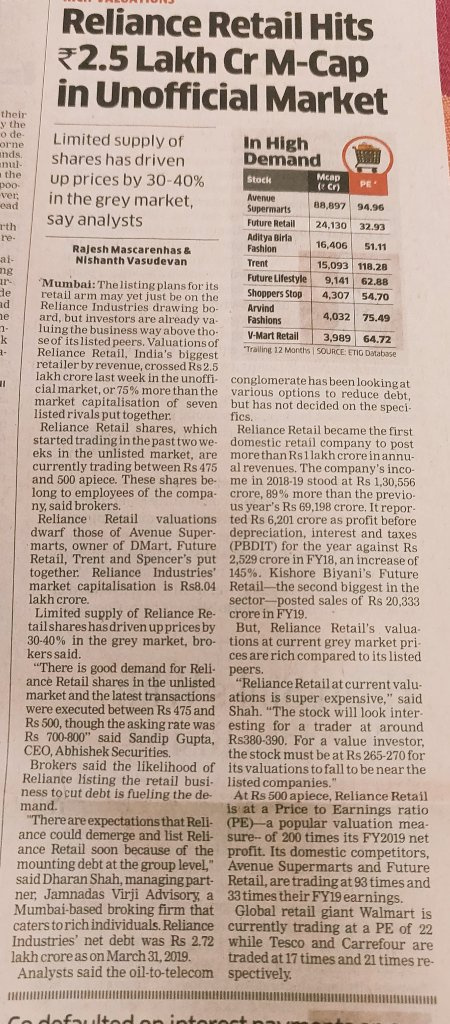

I believe that grey market valuations may not be driven by fundamentals. So grey market valuation of a pre IPO stock may not impact the valuation of Dmart over a longer term. Say 10 years from now, the grey market valuation of Reliance may not be even present. We have seen IPO prices stabilize after several years to reflect the intrinsic value.

Since there was a post on grey market premium, I am posting an example where we saw short term pricing at play. #DataPoints to show that short term IPO prices may not hold for very long if not backed by real intrinsic value.

I also recently invested in DMart after reading the Walmart article shared earlier in this thread and below CEO interview which was also shared earlier in this thread. Opportunity is huge and all sorts of players will co-exist - online only, omni channel, physical store.

Big Basket and other e-commerce players are gaining market share in the grocery segment. Their growth is more than that of DMart. But if that’s the case, how is D-Mart gearing up for that?

The market is extremely large. Right now, our own weaknesses limits our growth. We are working hard to improve our own capabilities. Just to give you some perspective, market size of retail in India is expected at ~USD 960 billion by 2020 and is likely to grow at 8-10% every year. Every retailer growing is good for all of us. It’s nice to see momentum in all channels of retail. Even local kiranas are doing good business.

I think Reliance Retail’s valuation appears high because its profit margins are suppressed. OPM less than 5% and NPM less than 1% compared to Avenue’s OPM of 8% and NPM of 4.6%. So to compare both of them just based on P/E may be wrong. There is some chance of margin expansion in Reliance’s case and growth is faster too.