One more thing I have noticed that General Merchandise & Apparel share has slightly dipped from last year. This category enjoys higher margin.

If they invest all of the capital raised from QIP and NCD approximately 3000 +1500 = 4000/- Cr and their Asset turnover ration is around 4.3

Revenue increase is = 4000 * 4.3 = 17200 cr

at net margin 4.7% they will increase earning by 740/- cr it can increase EPS by 11.92 /- almost 83% increase this can bring down p/e to 48 at current share price.

I am not sure if this really works in this manner. I leave others to validate this theory.

One point come across my mind that this whole investment can take around 2-3 years. However all said and done if they can raise this kind of money look at the benefits for the business. This tells why an investor should stay invested in such a business.

Nice quick play with numbers, you missed one part… NCDs will cost approx 150 Cr per year & that will bring earning in your calculation down by same.

Regarding share of general merchandise & apparel, I do observe same & at one of the store, I visit frequently… its almost 25%… earlier they had 4 floors & now operating on 3 floors. Important point is that the store celebrated its first anniversary few months back.

Pricing cheap does not determine success. EDLC before EDLP

PAT Margins of 4-5% - anything more than that is a rarity

Prefer to buy and construct stores, however its becoming increasingly difficult to do that. Until malls offer favorable terms - not interested in going there

Our own weaknesses limit our growth, working on improving capabilities

Currently no loyalty programs - treat all shoppers same

The only promise we give is that we will focus on the business

It will take a few more years for mall owners to understand the value a retailer like D-Mart brings to the entire mall. A D-Mart store could bring in revenue per square feet that is 5-7 times that of a mall, but our margins are extremely thin. Hence malls must offer rent at reasonable rates to us if they want footfalls to significantly increase for the entire mall.

We prefer to open more stores in states where we are already present and penetrate deeper in those areas. There is no aspiration or strategy to become a pan India player. Quality growth is good growth, irrespective of the region it comes from. We do not mind being called a “regional retailer”.

The market is extremely large.

It’s in our DNA not to lose money recklessly.

We just did one thing all through those years - single minded focus on the business. The only promise we can make is that we will continue to do so.

They wish to open more stores than current year & they themselves are not satisfied with target achieved in opening new store.

It says a lot as revenue growth was quite OK… mainly due to support from SSSG.

In market capacity terms, they are just 0.3% of available opportunity.

In near future… may be 3-4 years or earlier… we can expect Dmart in Malls as well… timing is just guess but when they have started thinking… it will click sometime & that will provide a big breakthrough in quick & fast expansion in terms of no of stores.

Will D-Mart will be opening store for next 10 years ??

Damani being value investor himself know where we as investors look for SO …Numbers ( CAN it be Cooked to serve you before offering one to god )… I don’t Know …

Valuations are very expensive … … Greed Vs opportunity

They are creating values as they are Solid model to have OWN STORES so their value will appreciate over the time But having creation of value among the shareholders … ???

Issuing commercial papers will that help or an escape from paying taxes ???

Being INDian means MUJHE SASTA KAHAN Milega … BUT still 5Rs Packs of snacks are hit Though they offer Maximum profit to manufactures and least VALUE t consumer … but WHO CARES… THEY DON"T want to PAY Memberships … Rather they take friend card to get the Things at Discount … E.g NETFLIX account is shared among the hostel friends …so there might be some platform leakages …

Reliance / Biyanis all are in this race … ( i know SABKO MILEGA as the MARKET IS HUGE but at the same time the MARGIN is THIN )

MEbership fee 18% GST is applicable BUT IS Company is paying or not ???

Disc : Not invested in watch list .this is not any stock recommendation to buy or sell

Good questions, which are necessary for balancing people with ONLY positive thoughts about Dmart

I would share my view & remain open for comments form others

Similar concerns are raised earlier also on forum, although those were reported SELL by employees / insiders. My reply remains same even for current concern

With current fund raising plans, I can smell atleast for next 2-3 years… will have a revisit once the fund is utilized

They are open to lease & even exploring options with Malls (recent CFO interview), being positive I feel it will materialize & could be next spike…

Will be interesting to see, if they continue to do after NCD & QIP.

Dmart has only 0.3% so no concerns on this… atleast for now

Interestingly there is a community on facebook called ALDI Nerd, where people share interesting deals and price discoveries and then people flock the stores to buy that.

D Mart is taking calibrated approach to reduce margins and to make up it with larger sales. This way they are creating moat for them. To compete with D Mart, one needs to creat the business on a scale like D Mart. Only operational efficiency will play. Lot of research reports now a days are focusing on falling margins of D Mart. Without understanding the business plan of D Mart, how can these analysts comment on profit margins ? They reach on quick conclusion that competition is eating out margins. How funny it is. Damani said very clear in a call last year not to expect profit growth for some quarters. They were reducing prices and operational efficiency with time would play its role to protect and grow profits. If one tracks business, reads Conference calls, annual reports, one will not bother for margins, he will bother for sale. I think, these analysts don’t track business, they just see the profit loss account and build story.

According to market research agency Nielsen, there are around 12 million kirana stores in the country, accounting for 90 per cent of domestic retail and FMCG sales. Around 8 per cent of retail sales come from modern trade, while 2 per cent comes from e-commerce.

Future Group plans to take its small-store network from 1,200 now to 10,000 in the coming years.

Reliance Retail has already added over 2.5 million kiranas to its network in the past few months and is looking at another 50,000 stores as launch of the new commerce venture nears.

These clearly state that life is not easy for any retailer.

I worked at a hyperlocal grocery startup a few years back. In the hyperlocal model small shops/supermarkets store inventory, whereas the startup will manage online orders and delivery. This was a win-win for everyone - the shop keeper (gets additional online orders), the consumer (convenience), startup (no headache of managing inventory). Long story short: The startup shut down after 2 years of operations. Read: Hyper funded PepperTap to shutdown operations this month.

PepperTap wasn’t the only one.

Prior to PepperTap, Localbanya and Townrush wound up their operations as they failed to raise risk capital and build sustainable business. Biggies like Paytm (Paytm joins hyper-local game, enters grocery segment in Bengaluru) and Flipkart (Flipkart shuts Nearby) also launched on-demand grocery verticals but have pulled the plug on their operations soon.

It seems the industry suffers from selective memory. They forget why ‘good ideas’ din’t work out in the past. Without fixing those past problems, you are simply going to replicate failure. Not success. Let me summarize why the hyperlocal model of tying up with local retailers for online orders does not work.

Similar ^ stats were thrown around about the size of the market, number of kirana stores, long runway for growth etc etc. Tying up with small retailers doesn’t help you in anyway. Here are some key reasons why such startups fail:

You have no control over inventory. Its difficult to sync up inventory between the store and the e-commerce portal. Main reason being small shop keepers or even medium to large super markets do not have accurate records about their inventory. Their inventory management systems are mainly used to store barcode-price data, not the quantity data. This results in poor experience for the customer if they see and order something online but the product is not available at the store. Sourcing from other stores adds to delivery time and costs.

You cannot have a large variety. Such companies just cannot offer the variety which DMart or More offers since they are limited by the size of the store.

Unit economics do not work out. I spoke with Grofers and BigBasket executives recently and they mentioned that their average per order amount is Rs 600-700. They are spending about Rs 70-80 for warehousing, delivery, customer service etc. Thats more than 10% of the avg order amount. To earn any profit you need to have high margin products (non-FMCG) and/or private labels. Things were pretty much the same 4 years back when I worked at the startup.

Grofers and BigBasket have been burning money and that is why they need to keep on raising venture capital.

I understand that Future Group & Reliance Retail must have think tank & I expect that they must be aware of mentioned challenges & failed historical cases.

Shall we write them off without having a look on their action plan? I take your points in true spirit & would love to keep a close watch on these big groups. My interest is how do they impact my business (Dmart). If they are harmless then I am the happiest person holding great business.

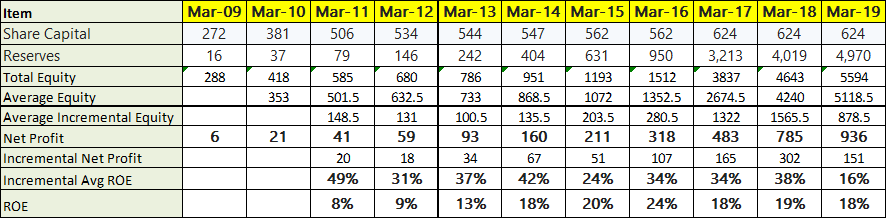

After doing exceedingly well in redeploying capital north of 35% for a very long time , Dmart in 2019 could manage an incremental ROE of 16%. Initially, i had thought that the ROE would cross 18% and settle at 25% or thereabouts however, that seems like a tall task in the hyper competitive world of retail. So have updated and upgraded my beliefs accordingly.

As i have come to understand in retail (many businesses in fact but especially in retail), the operating rule seems to be get rid of excess margins before excess margins get rid of you ( Dr Velumani are you listening?)

Can’t agree more with this. When companies attain pole position in the market or have an attractive product people are ready to pay any price for, they tend to lose focus on innovation (on process/product) and that invariably leads to a competitor taking the baton offering attractive pricing for a competitive offering. When there is elasticity in demand, it ought to be used to cut margins and increase sales to keep competition at bay and to keep the innovation fire burning. In competitive businesses like retail, this is all the more essential.

That was fantastic. Low operating margins are a moat against incompetent competitors who are in it to make a quick buck. Margins should be high enough for you to make sufficient profits at a returns higher than your cost of funds but low enough to keep competitors at bay. I personally feel higher the profit margins in an industry, the bigger chances of the industry players becoming inefficient. Case in point is the RE industry. IT services is another.

There are five entities that you can influence sharing of excess margins with

Customers, Employees, Suppliers, Government and Competitors

In the liquor and real estate industry, excess margins are shared with the government else you can go out of business.

In retail - customers seem to exact gravitational pull. This willingness to pass on margins is a source of advantage because if you don’t then you will have rivals take away margins and these rivals will pass on margins to customers which is what Dmart does so well.

In the software services industry - excess margins need to be shared with employees else the clever ones leave.

So depending on the industry this pans out differently.