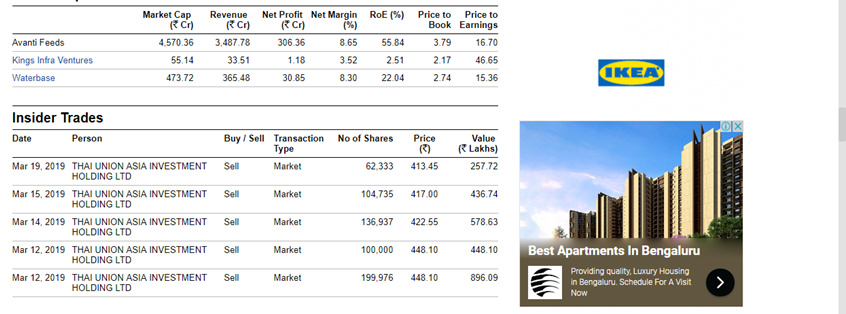

Sell quantity is not even .50% of outstanding share. When asked to management about Thai Union share sell in Q4 concall. Management said that Thai Union is committed to maintain the stake between 20% to 25% in Avanti. So that was the clarification.

Good Q1 results by avanti during testing times. Processing segment is showing good growth. Overall, on a consol basis 10% EPS growth yoy, 37% growth qoq. If raw material prices soften, it will further boost the performance

Given the few negatives above - thought of sharing some positives:

If one tracks the nos of competitors like Waterbase, IFB Agro both the cos reported material drop in income from feed sales in Q1FY20 while Avanti could maintain its turnover and gave a positive outlook. This clearly indicates and validates that Avanti is able to gain market share despite having a very high market share. I think this is a very rare phenomenon and generally seen only in very high quality FMCG names or few other areas. And all such cases trade at steep premium valuations.

Other positive is that the shrimp prices have been improving and now seem to be near pre-problem levels. Though in near term there must have been impact of floods etc but if such prices are to sustain, it helps the industry and farmers go for more farming in upcoming seasons.

Vietnam work as a value addition. They import from Ecuador ,India the raw shrimp and export value added product to EU and US market . In 2018 India exported 833 m dollar shrimp to vietnam. Dont think its an outright bad move for Indian shrimp industry. If there is traction in Vietnam then Ecuador and Indian shrimp will do increase business with vietnam.

The fortnight old strike by fish meal industry for GST exemption is likely to put shrimp feed manufacturers in the doldrums.

Ramakanth Akule, CEO, The Waterbase Ltd, Chennai, a leading manufacturer of shrimp feeds, told BusinessLine that fish meal is an important raw material for shrimp feed production. “Right now we have enough stock to meet the production requirements. There will be serious issues if the strike continues. We do not have any substitute and in the absence of this raw material, it is not possible to make nutritional food for shrimps”.

Thanks @yogansh for the well pointed summary. Adding below my notes as well as interpretation and analysis from annual report. Some of the points might be repetitive but want to keep it to look back at notes:

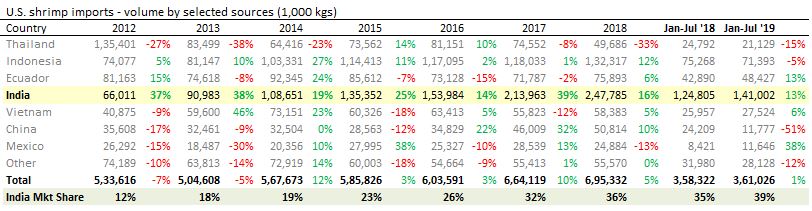

Notes from 2018-19 AR:

Key points:

Largest manufacturer in shrimp feed in India

5 feed manufacturing units and 2 shrimp processing and export units

4 windmills with 3.2 MW capacity

Shrimp feed: 6 L TPA capacity and 4.2L used at 66% capacity utilization

Shrimp processing and export: 22000 TP and 11065 TPA used at 50% capacity utilization

78% revenue from feed and 22% from shrimp processing

Overall market volume declined by 20% but Avanti’s volume declined by 2% without taking price cuts and Avanti gained market share

Added 1400 new farmers to customer base

Management compensation though at border of ceiling limit, the good thing is that lot of this is linked to performance and management adjusts its salary based on variable performance which looks in right direction for a cyclic business. However, this also highlights that management compensation would always remain around ceiling limit.

Key Positives and points liked:

For feed, company expanded beyond India in nearby countries like Bangladesh

For shrimp processing, geographical risk deleveraging by expanding to non-US countries like China, Japan, Korea etc. Exports to US declined from 85% to 74% through effective geographical diversification

Despite of turbulent times when there was pressure from demand cool off and increase in raw material price, company could not only maintain its normalized margins but also increased its market share to 48%.

The achievement of market share gain and maintenance of normalized margins was not done at the cost of stakeholder and the farmers were paid as usual. This helps in building customer ecosystem strength (to promote shrimp culture by farmers) and competitive advantage over other players and may be these are reasons why Avanti has progressed ahead of others. Still, it makes decent cash profit

Good growth in shrimp processing as well as better margins than feed even at relatively lower scale of operation

Higher growth into value added products in shrimp processing (347% growth rate)

Foray into shrimp hatchery

The regulatory requirement of US NOAA was launched in 2019 but Avanti has been proactively doing it from October 2018

Good to see 11% margin on shrimp processing businesses which is still growing at healthy rate which looks margin accreditive

Risks/Concerns/Negative Points:

Extended winter on customer end can lead to subdued demand through slow stock movement. Last year this led to demand issue. So, there is a cyclic behavior in demand due to:

Customer side weather condition

International supply in a highly competitive environment

Raw material price fluctuations (soya prices) and inability to pass through margins and hence business need to be viewed from cyclicity perspective in terms of valuation for normalized and sustainable metric values. Last year raw material prices increased steeply

Extended summer on shrimp cultivation side can lead to higher than expected diseases which can lead to decline in shrimp culture. Another risk to be watched out which also played this year

Outlook

Current year looks relatively better than last year on various risks and concerns highlighted

Company to keep investing operationally in areas identified in terms of geographical diversification, value added services and additional business lines

Disc: Hold a position and accumulated in last 30 days. Please do your own due diligence for any buy/sell decision

Have greyed out high margin Fy18 quarters (aberration) in the chart below. This is to cut noise. Avanti now has normalized margin in base data. In fact, Q2Fy19 seems below normal; depressed from top-line and bottom-line perspective. Historically Q1 and Q2 Fy are Avanti’s best quarters (seasonal). Q2Fy20 will have benefit of relatively low base for YoY comparison. Going forward Avanti’s financial performance will be largely dependent on its volume growth - as long as there is no sharp RM/shrimp price movement volatility hereafter.

Avanti continues to be high quality cash generating machine. Co has grown without debt and continue to do so. Co has a problem - problem of where to deploy cash - a good problem to have! Co continues to gain market share in feeds; no sign of tiredness. Farmers continue to trust and prefer co’s feed for better Feed Conversion Ratio (FCR) and Average Daily Growth measurable benefits.

Mix of remunerative farm gate prices and no deficient rainfall this year should bring back farmers. Better days ahead. Seems stock price is not factoring positives currently.