Q4 is generally the worst quarter and still it gave a good results…With the point regarding how they will implement their experience to prevent EMS and the capacity expansions valuations are mouth watering…Peter Lynch’s quote seems to be apt in this situation-The best stock to buy may be the one you already own

I hope Avanti takes measures to perform QC on processed shrimp for presence of anti-biotics to avoid rejections. As mentioned in earlier post by @Tolaha , 6 entry lines were rejected by US.

I am new to this forum, and Avanti Feeds still look good on all valuation parameters, such as, reasonable P/E, low PEG, and low Price/Sales ratio. I am aware that, this is risky business due to its nature and dependency on living beings. Though it has gone up substantially it looks like that, due to consistent high growth and market opportunity worldwide, may continue to show good PAT and Revenue growth.

I am researching to find out reasons for low P/E ratio. Risky business seems to be the major reason and also low profit margins could be another reason.

Avanti has in-house Laboratory to conduct special tests to detect

the presence of micro organisms and anti-biotics to ensure the end

product is absolutely contamination free.

Avanti makes sure that every step is taken to make its products

entirely free of antibiotics and steroids.

The system of traceability adopted by Avanti ensures tracking its

products from hatchery to the consumer.

This is a market with loads of shrimp exporters from India. The differentiating factor between biggies like Avanti when compared to small-timers should be the above 3 points. Even if Avanti’s quality check fails to prevent its export consignment from being tainted with antibiotics (yes it’s unacceptable but maybe unavoidable for a company handling thousands of tons of shrimps from various sources), hopefully the 3rd point above regarding traceability really works and Avanti manages to root out that particular farm from its supply chain.

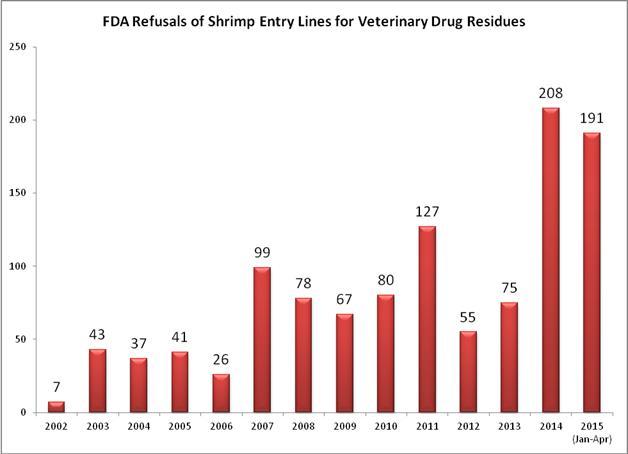

To bring those 6 rejected entry lines of Avanti into proper perspective, here are the number of shrimp entry lines refused for reasons related to veterinary drug residues by country since 2002.

In particular, of the 1,025 entry lines of shrimp refused for reasons related to veterinary drug residues since 2002, over 90% (928) were shipped from just five countries: China, Malaysia, Vietnam, India, and Indonesia.

Ayush, that news article is a HUGE development for Avanti Feeds. If I remember correctly from the annual report of 2013-2014, they had processed about 3000T of shrimps and earned great Net Profit Margins of 12% from the business. This is 5 times the capacity. At 2013-2014 prices, that itself will lend more than 1250 crore to the topline when the plant runs at full capacity. At half the margins of last year that is 75 crore to the bottom line. At current prices this may upto 150 crore! We are talking 275 crore bottom line for Avanti if the current situation holds! Upto last year more than 70% of profits came from feed division. Going forward this will change and majority profits in times to come will be from shrimp exports.

Do you any way of tracking where shrimp prices are in relation to last year and what kind of margins are possible at current prices? My understanding is that the current prices are down 10% from the peak. How good is their ability to maintain margins at even lower shrimp prices? Last 3 years irrespective of shrimp prices, their margins hovered at around 12% but the 3 years before that margins were negligible. Your comments?

Yes, over last few months the USFDA had got really strict on the screening of antibiotics in the shrimps and did reject a lot of containers. I believe its really important for companies to adopt the best of safety measures and control this problem at their end itself. Based on the industry feedback, we have learnt that Avanti has been one of the early adopters of strict screening. So what you are saying is correct - that if Avanti does this job well it bodes well for the company and its prospects.

Yes, it could be a big positive for Avanti as the article talks about bringing value-added products to India such as ready to eat etc…in which TUF is a big leader and would be having its own proprietor know how. So this could be one of its kind project in India and its good to see that Avanti is getting the majority stake of 60%. Regarding numbers from this project - I think your numbers might be way high. Lets be conservative.

Regarding drop in shrimp prices - yes, they have corrected almost 30-40% from the highs and should be at about $4.25-4.5. If we see the historical shrimp prices…then the prices used to be in the range of $3.5-4 till about 2-3 years back (before the EMS problem hit Thailand) and had gone to about $6 during the height of crisis. So the period of abnormal profits to the farmers is over. But even at these prices the shrimp farming should be remunerative.

Hi again Ayush,

What I notice is that in the last 3 years while the price has been steadily rising the margins have remained fairly constant at 12%. For example in 2012 while the prices of shrimp were much lower than today, yet margins were similar to current level. Perhaps, there is a strong correlation between pre processed raw material prices and processed shrimp. Also remember that last years prices were a temporary aberration, but if you average the prices out over 12 months perhaps they are close to where we are currently.

Abhishek.

If I remember correctly from the annual report of 2013-2014, they had processed about 3000T of shrimps and earned great Net Profit Margins of 12% from the business. This is 5 times the capacity.

Avanti had a capacity of 8000MT if I remember correctly. So if they could just manage to get raw materials worth 3000MT, it just means that they now have 5 times bigger problem in getting enough raw materials! Shrimp processors generally seem to be having trouble obtaining raw shrimps world over and not just in India.

My understanding is that the current prices are down 10% from the peak.

Prices have gone down by a huge margin.

Also, from what I hazingly remember reading here in the Q&A section, a number between 2.8 to 3$ on an average was supposed to be the price point above which shrimp farming was remunerative in India. But that was a while ago, so inflation and exchange rate would affect this number.

Last 3 years irrespective of shrimp prices, their margins hovered at around 12% but the 3 years before that margins were negligible.

The trend in Avanti so far has been decreasing numbers in shrimp processing and so the margin percentage would be skewed towards their Feed margins.

So what you are saying is correct - that if Avanti does this job well it bodes well for the company and its prospects.

@ayushmit Pardon my cautionary approach to good news. As Avanti is the major portion of my portfolio, I am focussed solely on negatives rather than positives!

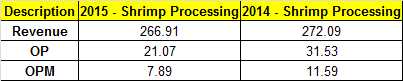

Tolaha, thanks for inputs. Just a small point though, when I said margins of 12%, I meant margins for shrimp processing. Margins for shrimp feed hover at around 8-9%.

Avanti formed about 12% of my portfolio at one point but I decided to trim. Too many things to track. Not worth losing sleep over a stock!

Also any idea of the next expansion of feed capacity? They had mentioned it in the last AGM but there has been no news since.

Abhishek, this is what I got from some recent reports on Avanti.

In FY 14, the shrimp feed manufacturing capacity of Avanti Feeds was 2 lac tons per annum. The company expanded capacities by 30000 MT and 50000 MT at Gujarat and Andhra Pradesh plants respectively last fiscal. Currently expanded capacity stands at 2.85 lac MT.

The shrimp processing capacity is 8000 MT currently.

Sorry for dup @ayushmit - seems our posts crossed :). I would have happily deleted my post, but thinking to keep it for “Key Takeaway” points. Many thanks for this wonderful stock pick. Cheers!!

The US Food and Drug Administration (FDA) announced the Veterinary Feed Directive (VFD) final rule, an important piece of the agency’s overall strategy to promote the judicious use of antimicrobials in food-producing animals. This strategy will bring the use of these drugs under veterinary supervision so that they are used only when necessary for assuring animal health.

The VFD final rule outlines the process for authorizing use of VFD drugs (animal drugs intended for use in or on animal feed that require the supervision of a licensed veterinarian) and provides veterinarians in all states with a framework for authorizing the use of medically important antimicrobials in feed when needed for specific animal health purposes.