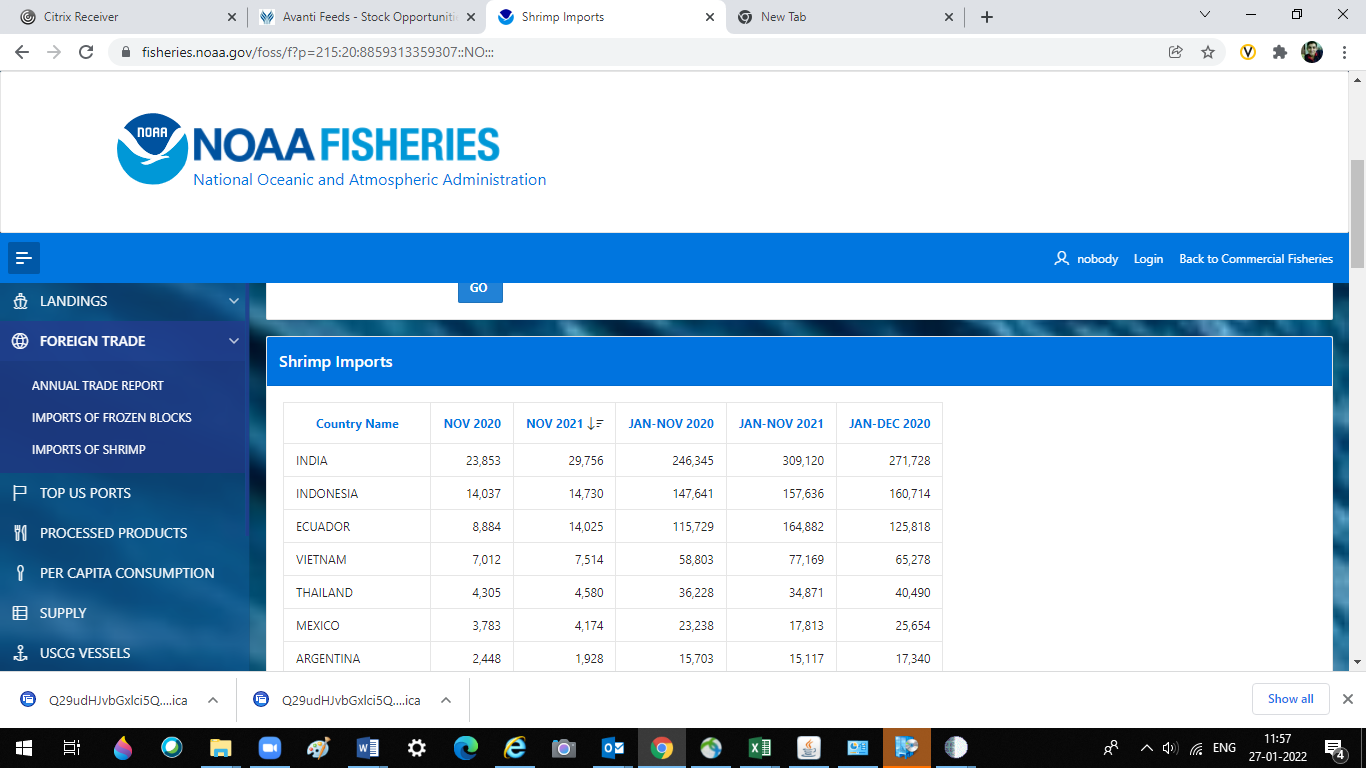

November 2021 Exports are good too, Dec 2021 figures will be posted once the month is over.

2 Likes

2 Likes

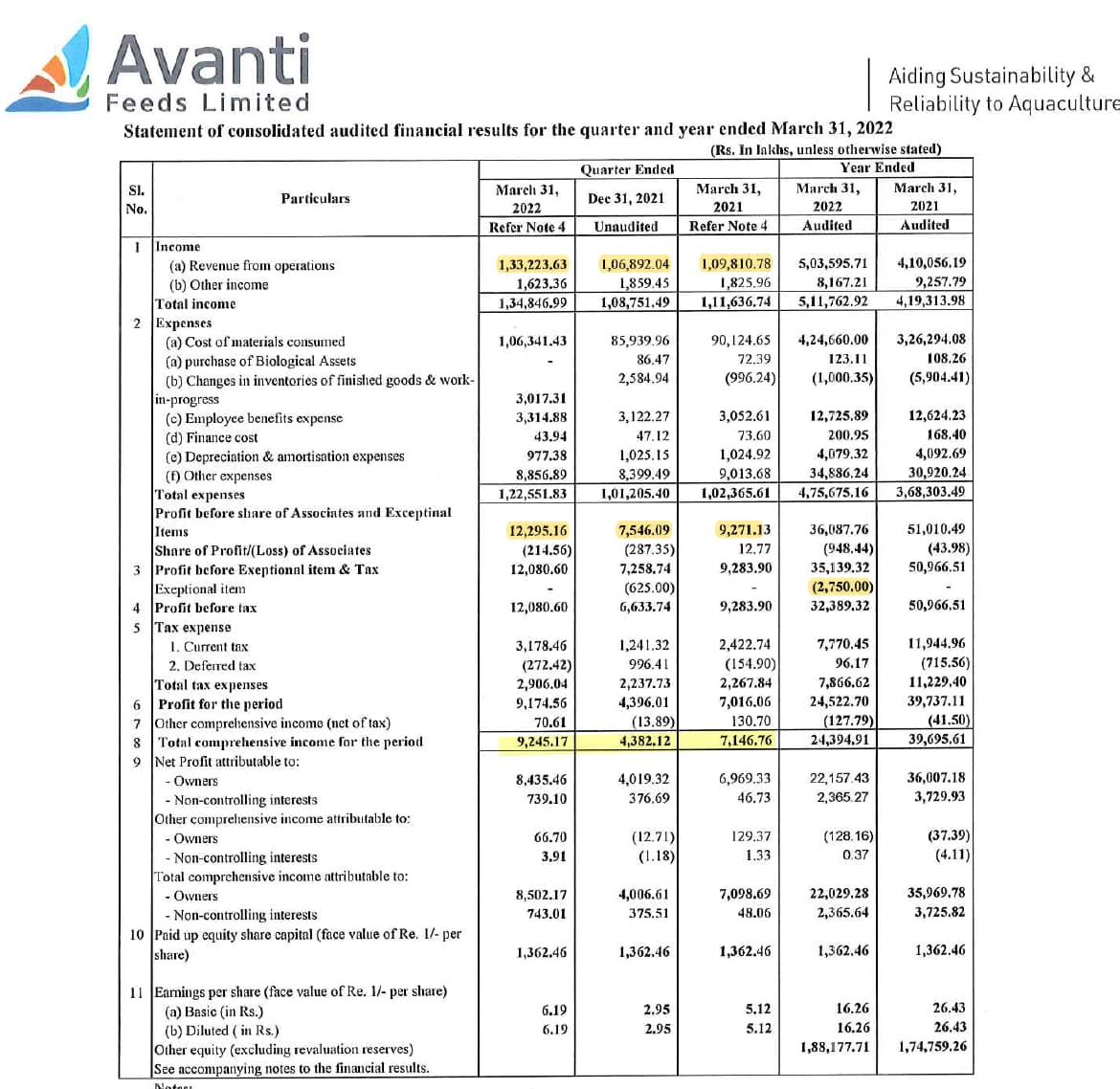

Results for the quarter

Results .pdf (4.6 MB)

OPM on a year on year basis has been hit badly and stands at 6.32% VS 10%.PAT is down almost 50%.

Avanti Feeds and Cp Feeds are increasing feed prices @Rs.4~5/kg from 1/3/22.

2 Likes

Hi,

Regarding the comments on yesterdays investor call by the management on a question on what some investors see as red flags such as holding high cash, recent investment with RBF/Thai Union via Srinivasa Cystine outside the purview of the main company and the recent management remuneration hike :

While the management was able to justify their actions on all these points just wanted to get an opinion from long term and seasoned investors who have been following this company from a long time if the justification is satisfactory.

Q3FY22 concall notes

Revenue guidance for FY23 and FY24? Revenue growth 10-15% in FY23. Current margin is 6%, we are aiming for 10-12% EBITDA margins.

Feed business

-

Fish meal was avg 89rs/kg in FY20, 94rs/kg in FY21 and hit a high of 102 in FY22. Shortage in supply and export demand.

-

Soya meal also increased sharply. Govt permitted imports, suspended trading on NCDEX and good crop, but prices not coming in control. Avg 70rs/kg in 9mFY22 compared to 43rs in FY21. Govt prohibited stocking beyond some level.

-

Wheat flour- less volatile 21-24 rs/kg in 9mFY22

-

Price hike- 8.07rs increased thrice in 9 months- 2+3.15+4.25. RM increased by 10.48rs/kg, leaving 2.41rs gap. Expecting RM to stabilize. Cautious approach to increase price due to govt regulatory constraints. In budget, govt reduced customs duty on feed from 15% to 5%. It was increased to 15% in july 21. Representations made to govt to increase the duty again to protect domestic industry as they are suffering due to feed imports. We are looking into price hike by March first week, working out the amount. Matches with post by @ravurusaipraveen that Avanti Feeds and CP Feeds are increasing feed prices @Rs.4~5/kg from 1/3/22.

-

Outlook- Favourable environment, promising year ahead for shrimp culture. Shrimp production expected to increase to 8Lakh MT as farmgate price at ATH. Feed consumption in India expected to be 12-13 Lakh MT, Avanti expecting 6-6.5 Lakh (growth of 15-20%, maintain market share 48-50%). Industry did 9.55L in 2020, 11L in 2021 (Avanti did 5.36L).

-

Expansion of 1.75L MT with Rs 125cr expected to start in June 2022.

-

Fish feed- Working seriously, process is on. Will take 6 months to 1 year.

-

Third quarter is seasonally weak

Processing

-

9month income increase 7% due to volumes. Price realization remained at same level. PBT fell 36% qoq due to inclusion of MEIS benefit received in Q2FY22. Excluding MEIS benefit, PBT was flat qoq. PBT fell 19% yoy due to impact of freight cost. Avg freight rate for 9month was 5.41L per container vs 2.67L in FY21.

-

RODTEP- effective jan 21. 18.48 cr benefit in 2021 has not been accounted for and will be accounted when received

-

Recall- June21, Aug21 (expanded). Liable to compensate for destruction charges and replacement. Liable to reimburse medical expenses to customers who fell sick. Co has product liability insurance coverage, but none for replacement etc. These costs were met by co. We made 27.5cr provision. It will take some time for USFDA to close the recall. Shipped 5 containers cooked shrimp to USFDA. Green list will be restored in 45 days and we will be able to accelerate exports to US. We had already made an application to USFDA in June 21 to which they had responded with an additional query. To answer the queries, we have engaged an international food consultant team who analysed our processes and we have created a response to the USFDA. It should be approved in 45-60 days. 25-30% sales are to cooked products. We are focusing on products where we are not on red alert. If there was no red alert, our volumes would be up 10-15%, but we are trying to cover the volumes on our existing products.

-

PLI application- 11 processing units incl Avanti qualified to get 933cr. Each applicant will get 79.44cr. Benefits are for incremental production in 2023.

-

Outlook- Exports from India 6.5L MT in 2021, expecting 7.5-8 L MT, growth of 10-15%. Avanti exported 12219 MT, expecting 13500Mt, growth 10-12%.

-

Capex- 81.32cr to set up pre-processing and processing units with capacity of 7000Mt per year. We are in process of land acquisition so we should be able to start commercial production in 1 year. There was expansion in aug-sept last year in our old unit in Gopalpuram, we increased the production by 12% in 9months.

-

Existing customers have the appetite to take increased production. COVID impacted our growth rate because we are labour intensive industry and there were restrictions in footfall of labours

Salary hike to management? Isnt it better to increase dividend, or do a buyback to reward promoter also? We are giving good dividend and may increase it if performance is good. Salary hike reasons- Whole time directors- Fixed+ % of profits. The limit was fixed long time back at inception of companies act and increase is within companies act limits. Fixed portion increase is to cover increase in cost of living. Companies act is allowing to take more percentage so that is why we are going for an increase (?? beats me!) Work has increased, challenges have increased, competition has increased, expansion is taking place. There are external factors like RM costs that affect the profits. We are paying 43% income tax- it is a constraint. Remuneration has been stagnant over the years. We expect investors to understand and cooperate because we are taking care of you. (didnt sound good to me)

Unlisted Company formed with Thai union. Why is it kept out of Avanti? The business of RBF is manufacture and distribution of food ingredients is much related to poultry meat. Its a trading activity while Avanti is more of manufacturing. 51% held by RBF and 19% by Thai Union so 70% is held by the foreign co and they want to trade their own products under their brand. We will own only 30% stake and management us by them only. They have considered us as partner due to presence in India as a large group. We want to keep our focus on feed and processing rather than getting into altogether new business where we dont have experience. It will be a small business 5-10 cr so we have kept it out. Brands and management are not ours.

Cash level- the high cash level has helped us to buy RM 5% lower because of better payment terms. If this was not available, we would have to borrow from bank and increase cost. There is lot apprehension by banks to give credits because of market situation (???). If we dont have these cash levels, it is very difficult to maintain this level of performance.

17 Likes

Thanks for the summary and comments. I agree, my thoughts too were that the comments on the red flag issues raised did not sound investor friendly at all and lacked transparency.

1 Like

They mean to say, the management is paying 43% tax? Why not just leave the money to compound in the company and increase their wealth instead of paying 43% tax on remuneration?

“According to leading feed producers and trade sources, Indian aquaculture production is likely to increase 15-20% year-on-year given the good demand” - quoted in the article

Is this an indication of good times for the shrimp exports sector?

1 Like

Thank you for the update!! To summarise, disgusting Corp Governance practices!! Nothing been done over the last few years ( expansion into fish feed was being said since many years and haven’t seen any major development). On the contrary, company/ industry has been hit by major negative developments. And some negative developments even due to company’s oversight!! All in all, no improvement in earnings over the last few yrs… and amidst all this, they r announcing salary hike for management & independent directors!! And that too to meet their living needs!!! If 20 Cr annual salaried person is unable to meet his/ her needs, God save many of us!!! One of the classic example of how minority shareholders r kicked away and management keeps becoming richer & richer…I feel, with these hikes, any motivation left in the management would further be killed to improve status quo affairs. Hope such idiotic things r not passed through

1 Like

Sales is not issue here, Margins are. Due to steep hike in Raw material prices ,EBITDA margins are not sustained.

1 Like

Superb execution by Avanti. Contrasting results vs the competitor.

Shows market leadership.

Ayush

Disc: Invested in family acs

24 Likes

Return of margins?

“Domestic soymeal prices have continued to correct in the month of May itself. Prices corrected over the last one month following a decline in edible oil prices. Price is currently at Rs 49/kg down from highs Rs 95/kg seen in Q2FY22.”

Soymeal price falling since March, auguring well for shrimp companies Soymeal price falling since March, auguring well for shrimp companies

5 Likes

As per concall, Soyameal in May was at 69rs and the management mentioned that they had high inventory of RM. FY22 vs FY21- Fishmeal inventory of 242cr vs 118cr, Soyameal 197cr (28568 MT) vs 53cr (10,274 MT). …

“So, what you’re seeing in the balance sheet is on the date of 31st March, which happens to be the financial year ending day which coincides with the commencement of our season, subsequently April, May, June, okay. So that’s the reason why we keep enough stocks for production in April, May, June, but this year, we have kept more than what is required. See normally what we do is when the Soyabean was freely available in the market, we were storing around 15 to 20 days only. But now because there is a shortage of Soyabean we are we increased the stocking levels to one month now”

"The present prices are higher than what inventory cost that we have as on 31st March. So, we are at the advantageous position. If we were to buy today, it would have costed much more to us. "

I think the drop in soyameal spot price may not reflect immediately in the numbers. There will be a lag for RM price correction to reflect in numbers. My guess is that margins in feed should start to improve from Q2.

There was also this comment “we are booked with the government permitted input we have booked the 14,000 tons which we are expecting would cost us around rs54, but we normally use most of our products with high protein which will be higher by 5,000 per metric ton. The normal plus rs 5000 is our cost, high protein”

8 Likes

Hi Rohit,

You are right that as the co is carrying very high inventory vs their normal levels, I think it may take time before the margin expansion happens (though they did good margins in Q4 and perhaps the same should continue).

I feel that given the leadership of the company and contrastingly better executions vs peers, the market would be forward-looking to such positive industry changes.

Lets see how things unfold.

Ayush

Disc: Invested in family and client acs

9 Likes

Venkys declared their Q1 result and their margin got affected due to High price of soya and corn

Soya price rise could also affect earnings of Avanti Feed ?

3 Likes

in the recent con call management clarified that ![]()

- supply from ecuador is not of any concern , in short term as well as long term)

- not carrying much inventory

- hoping for Aug-Oct q better than last year

- optimistic for price rise in aug-sep , based on discussion with regulators and farmers.

Muted set of nos from the feed division of Avanti. Margin revival is still a couple of quarters away. Concall notes below

- Estimate shrimp feed consumption of 12.5-13 lakh MT in CY22 with production of 8-8.5 lakh MT shrimp

- Could not meet the demand due to capex delay which impacted shrimp feed volumes. Projecting sales of 5.7-5.8 lakh MT feeds in calendar year 2022

- Almost completed shrimp feed expansion of 1.75 lakh MTPA with estimated capex of 125 cr. (vs 50 cr. mentioned earlier). Commercial production should start in September 2022

- Should be able to meet the excess demand in next growing season with capacity coming on stream

- Out of 1.75 lakh MTPA of new capacity coming in, only about 80% is realizable as it’s a seasonal business

- Seeing soft shrimp demand in US, expect it to revive in November

- As FDA has terminated recall in May 2022, company has applied for removal of import alert

Disclosure: Invested (position size here, no transactions in last-30 days)

8 Likes