Further recalls from US market. This is not good for track record of Avanti

Your kind attention is invited to the Corporate Announcement dated 29.06.2021 by the

Company on recall of cooked shrimps processed by AFFPL between 23.10.2020 and 09.11.2020, on the basis of potential for contamination for containing Salmonella in those products, corresponding to import and distribution in US from late December,2020 to late February,2021.

Such recalled products constituted 177.242 Mts valued of Rs.16.11 crores. Out of the recalled products, 36.258 Mts valued Rs.4.10 crores have been received back and

destroyed or in the process of destruction during the period 25-06-2021 (date of recall)

till 10-08-2021 and the same has been charged off in the Q1 FY22 financial statements.

Further return of the products, if any, will be valued and charged off as and when claims are received.

On 21-07-2021, the CDC, USA has announced that “Salmonella Weltevreden Shrimp outbreak ends with 6 cases”. This outbreak was linked to recalled shrimps imported from India by Avanti Frozen Foods Pvt Ltd.

On 11-08-2021, FDA, USA communicated that additional 3 cases, apart from 6 cases earlier (initial recall), detected by CDC tracing to contamination of shrimps exported by AFFPL, for presence of Salmonella. Further, atleast one case is found to be out of the recalled products initially.

After discussion with FDA, AFFPL expanded recall of cooked shrimp products

imported and distributed upto May,2021. Initial recall was upto late February,2021.

As a result of expanded recall, a further 613.862 Mts of cooked shrimps valued Rs.50.12 crores has been included in the recall. The precise details of quantity and value of returned/destroyed products under this recall is expected to be received in due course and will be evaluated to take appropriate action.

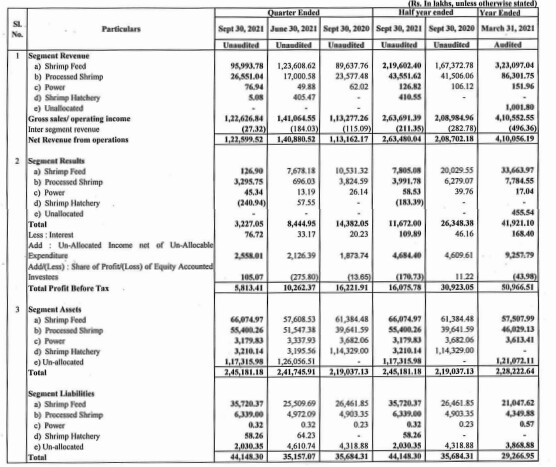

Growth 58%, PBT down 17%. Uncontrolled steep increase in RM costs such as soya, fishmeal.

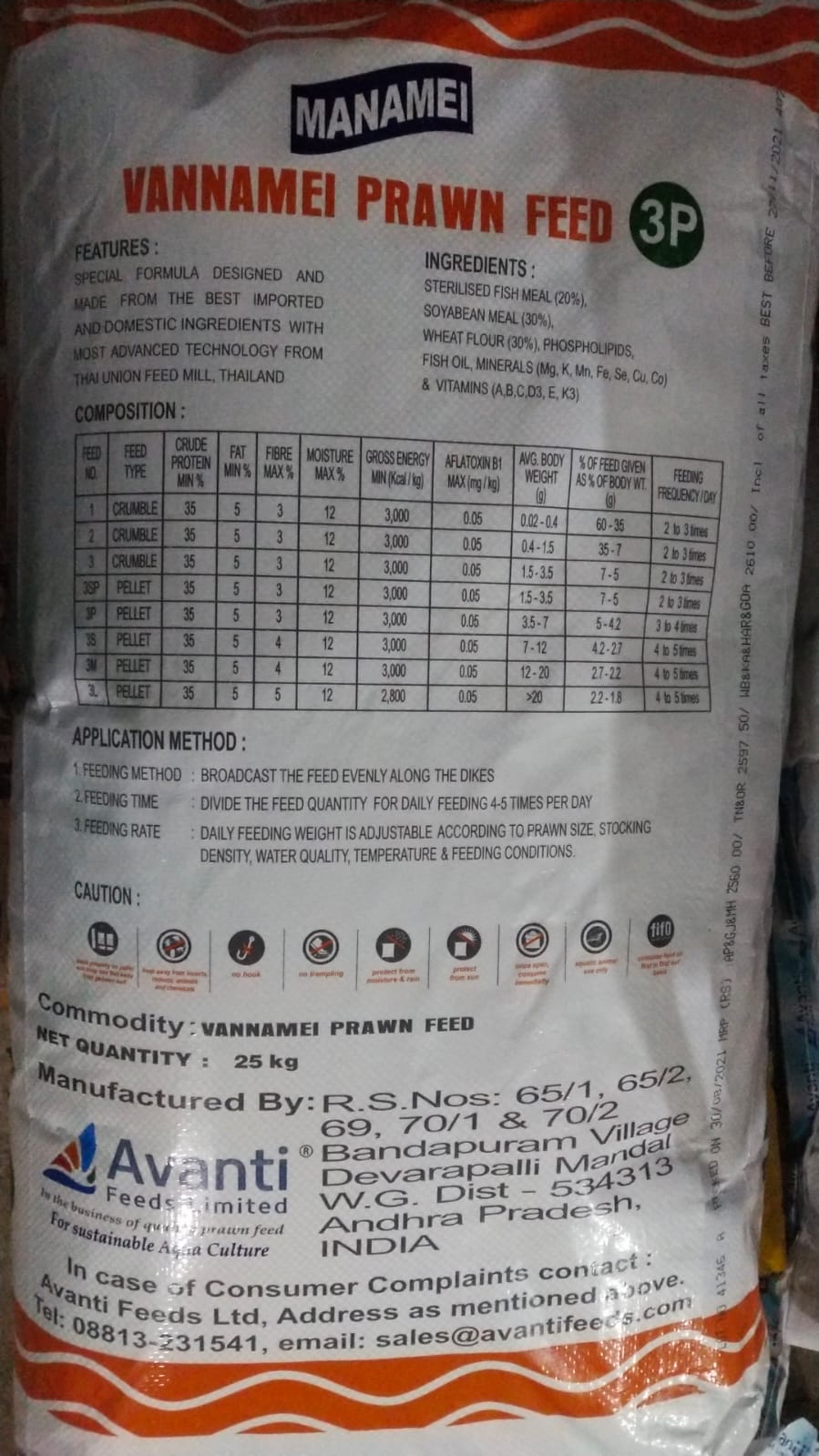

Fishmeal up 95/kg vs 91/kg in Q4FY21, now at 115rs/kg. This happened because there was a ban on importing soyameal. Some industries started using fishmeal instead of soyameal. From 1st Aug, the ban has been lifted on catching.

Soya meal at 46rs in Q4 shot up to 65rs and went to 105rs. Now at 95 after import ban was lifted. Govt allowed 15 L tons imports of GM soyabean meal. This requires some approvals from multiple bodies- GEAC, forest, environment etc. Import policy has to be modified. We have placed order to import soyameal from Vietnam. Landed cost will be 65-70rs. Expected this shipment in Sept. More suppliers will come up after the policy stand is cleared. Fresh crop in mid Sept so expecting price to soften.

Feed price hike of Rs 2.15 in April, Rs 3/kg in May, Rs 4.25 in August. This will have effect in Q2, Q3. Once RM prices stabilize post Sept, things will look better. We cant increase prices as we wish, we do it only when its is absolutely necessary.

Shrimp culture is expected to be good 9.55L Tons 2020, 2021 expected to grow 10-15% to 11L tons. Feed consumption was 4.55L tons in 2020, expecting 5.25 in 2021 increase of 15%.

Avanti Feed market share expected 48-50%.

Volume growth momentum should continue in coming Qs. Last year culture was down due to COVID. This year climatic conditions and sentiment (due to farmgate prices) is positive. This time area has gone up, lot of conversion has happened.

Processing Business

De-growth of 7.41% due to non-availability of containers (Freight rates went up 300%) and slowdown in exports of cooked shrimp due to more quality checks.

PBT dropped due withdrawal of MEIS, increase in marketing expese. Gross income includes 5% export incentive and 3% duty drawback- withdrawn. RoDTEP announced effective from 1st Jan 21. 2.5% of FOB subject to a cap of 16rs/kg. So effective benefit will only be 2%. This 3% will have impact on the result of the company. This 3% will be eventually adjusted between farmers, processors and buyers

RodTEP will accrue 3.88cr in Jan-Mar and 4.65cr in Apr-June. July 1.96cr. Total 10.53cr till now since Jan21. Govt saying that this will be credited automatically on exporting. This will get credited in Q2 or Q3

First Product recall -4.1cr impact charged off. This was 25% of the consignment. Second Recall expanded to 50.12cr imported in US. Need to see how much is returned. Expecting write off of 15-20% by Q3FY22.

Impact due to recall- We have engaged senior food safety consultants incl ex-FDA compliance officers in assisting us to built a robust, advanced food safety system in the world. Engaged people from Canada food safety association, USFDA, Indian counterparts. During the discussion, the first thing that came is that the major food processors incl Thyson foods who had a recall of 9mn pounds of chicken, Kellogs …the US inspections have increased substantially. USFDA/regulatory authority work with the facility to ensure that the food safety system is upgraded. We are presenting to them the most robust system incl testing equipment, doing testing with same equipment used by USFDA. It will not impact volume in long run. We are in constant communication with customers. Things are going in the right direction. As the system shows its result, any impact will be mitigated.

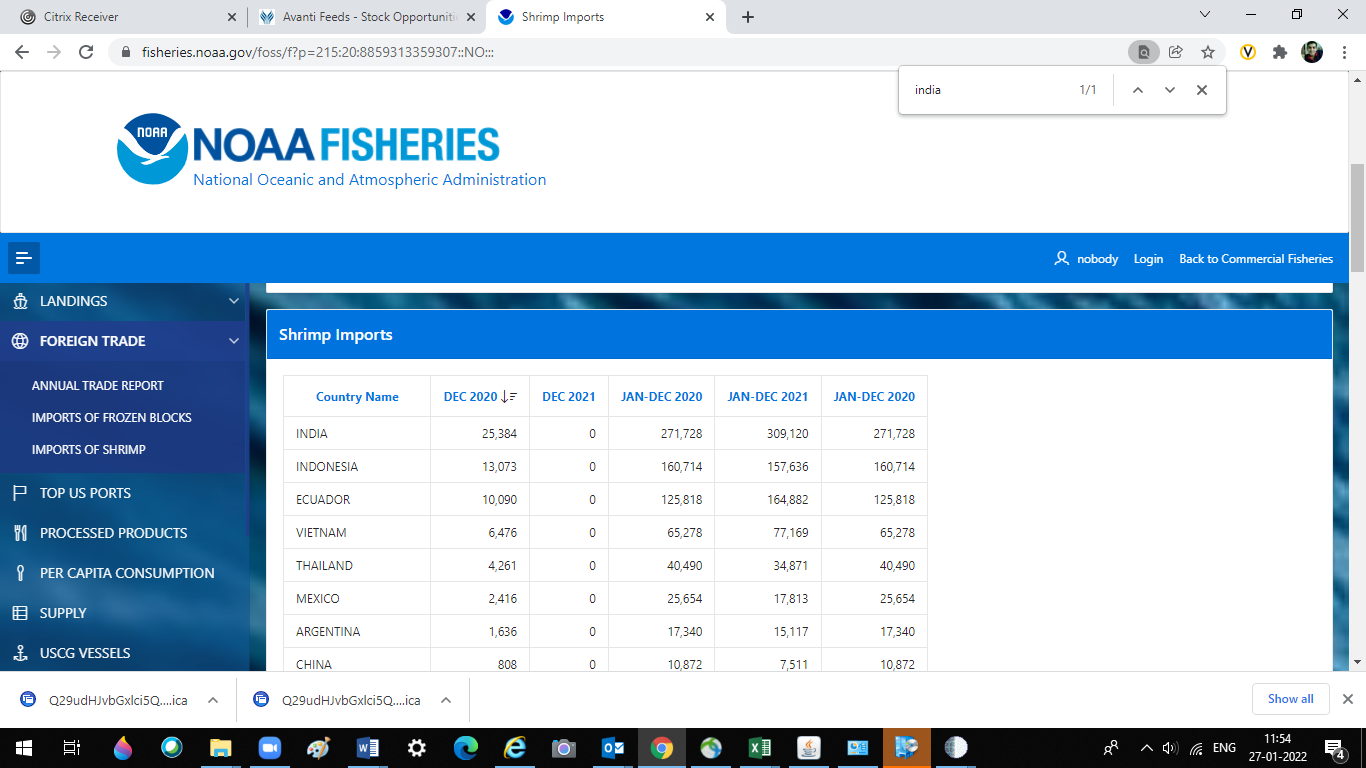

Shrimp exports from india in 2020=5.75 L MT, 2021e= 6.5L MT, growth of 10-15%. Avanti 2020= 12,192 MT, 2021 expecting 12700 MT, flat

Earmarked Capex plans of 100cr

Feed- Wanted to increase capacity by 1 L tons and also planning fish feed capacity. Getting quotations, will come out with plan details by end of this year

Processing- Capex spend towards testing equipments etc. After CU increases to 80-90%, then we will decide on capacity increase. Some plans to modernize the plants

Farmgate shrimp prices are rising, probably due to holiday season import demand from USA.

Some suggest dichotomy in price movement of larger vs smaller sizes, due to excess availability of smaller sizes as farmers are harvesting sooner, being reluctant to take risk of diseases.

With the holiday season demand, if USFDA concerns are well addressed, demand side looks robust. However, raw material price volatility is a serious concern and can have significant impact on margins.

As import of GM soya meal is allowed now, it will be interesting to see further developments in this regard. If in future, cultivation of GM soybean is deemed acceptable, raw material price volatility would reduce a bit.

Interesting to read this article and learn that Mr. Rao started as a finance manager and cs in a small group company and rose through the ranks to become a Jt MD! What an extra-ordinary success story both for the person and the co!

Pet feed and Fish feed looks promising to me . With the reopening of the economy and restaurants , the shrimp demand should be back to normal. Hopefully this will translate to topline and bottom line growth and thus growth in stock price

Expansion by setting up a new plant for manufacture of Shrimp Feed at Bandapuram, Andhra Pradesh with capacity of 1,75,000 MT per annum, at an estimated CAPEX of 125 Crores. Expected to be completed and commissioned by June '22

Growth on the feed side but margins had a sever impact. It barely broke even. Looks like the price hike didnt help them. Hopefully, next quarter will be better as soya has corrected sharply.

Processing seems to have normalized

Would have a view on the Outlook for the demand, especially on capacity expansion? Any thoughts from the management on why they r preferring a capacity expansion

Revenue grew to 960 cr an up 7.2% due to increase in sale price. volume declined marginally by 2.9% YoY to 1.27 lakh MT

RM increased by 14.7/kg, while 3 price hikes of 2, 3.15, 4.25rs/kg left unabsorbed price of 7.59rs. Full impact will be seen in Q3. ( later mentioned that “farmer has seen 7-7.5rs price increase while our cost went up by 16rs, the difference is borne by company”) However, RM price have come down

Fish meal 105/kg in Q2 vs 95/kg in Q1, now at 95rs

Soya meal was 65rs/kg in Q1, 110/kg in Q2, govt intervened to allow imports, 12L tons imported. Hit a low of 48-50 and current price 60rs, we have never seen such high volatility. Its a bumper crop this year. Large fluctuations at commodity exchanges. “NCDEX coming in the way”. We have 1200 tons soya inventory with us.

Other inputs have also increased.

To farmer, feed price has gone up but farm gate price has also gone up.

Soya crop this year is a bumper crop. Prices should come down. Fish meal should also come down. IF they dont, we will have to increase prices.

First crop has been good and second crop (Jan-Feb) also looks promising. Feed consumption expected to grow 10-15%. 202=4.55L MT, 2021expected 5.25L MT, increase of 15%. Market share expected at 48-50%.

Industry 10.5L-11Lton in 2021, 9.5L ton in 2020

Gained market share (conversion from other feeds) and area under cultivation is going up. Expansion from 6L to 7.75L MT at capex of 125cr. Commercial production from June 22. Capacity Utilization was 120-130% in Q1 (Peak season March-June), currently 85%. Since we are not able to supply to the peak season requirement, we are expanding.

Disease related early harvesting? There were 3-4 mild cyclones so farmers were afraid of the damage so they harvested early.

Thai Union Feed Mill has been listed and they mentioned Avanti as a partner. The royalty was being paid to them from the beginning and it will continue on same terms. Avanti is collaborating with Thai Union on fish feed. Thai Union is leader globally in Sea bass, culture is just starting up in India. Currently feed is imported from Australia and Vietnam. Many are using traditional raw fish feed. Avanti will encourage Sea Bass culture in India. Sea Bass is a premium variety. Tilapia culture is going up in India. Fish processing is not on cards

Processing

Volume up 12.2% YoY. Sales up 14.7%.

decrease in margins: Freight rates increased resulting, Reduction in export incentives MEIS. MEIS received 14.14cr has been accounted for

RODTEP effective from 1/1/2021-co eligible for 13.58cr so far. Will be accounted for when received.

Recall of products- June and Aug21. Destroyed in US.We have to compensate customers, reimbursement of medical expenses to people who got sick. This cost has to be met by co. 21.25cr in H1 has been charged as exceptional item. Further returns are not expected. We have done multiple food safety audits. Strengthened testing, increased number of microbiologists in factory. Thoroughly looking at our systems. Explained these measures to our customers. Dont see a long term impact to brand image and customer base

Exports from India in 2020 was 5.7LMT, expecting 6.5L MT in 2021. Avanti Shrimp export 12192MT in 2020, 12700MT in 2021.

PLI scheme-Made application and under process. 82cr capex plan is submitted.

Cash pile up??? We are using funds for expansion Feed 125cr, fish feed under planning, processing PLI 82cr. RM is Seasonal and needs to be bought in bulk. Working capital will increase with capex.

I have been holding on to the stock hoping they would start fish feed some day. Finally after a lot of talk, company is starting with it. Personally in my tier-2 South Indian City, I see a huge increase in fish consumption compared to 5-7 years ago. If company can replicate what they did with shrimp feed, will be a huge opportunity.

Sebi decided to ban trading in soyabean futures for a year. This was mentioned by the management in the recent concall with respect to fluctuations in soyabean prices driven by speculative trading.