Is there any visibility on a con call

Did the management disclose this event to the shareholders? If not, isn’t it mandatory to do so?

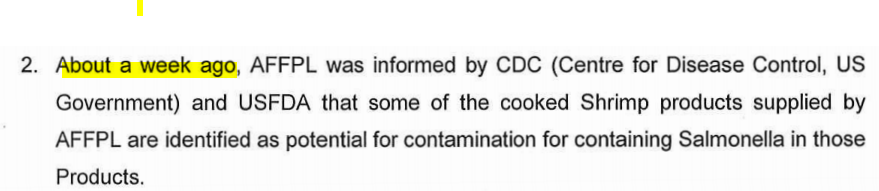

Here you go - https://www.bseindia.com/xml-data/corpfiling/AttachLive/807ec5eb-ccb7-4727-9e1c-ffe6d33cfcca.pdf

2 Likes

USFDA, CDC ask Avanti Feeds arm to recall shrimp products: USFDA, CDC ask Avanti Feeds arm to recall shrimp products - The Hindu BusinessLine

1 Like

No…It does not explain considering latest latest filing to the exchange (relevant snapshot shown below).

Results of Q4FY21 also came around the same time and I hypothesize that it was too late to accommodate the impact of this event

On the overall impact, company’s reasoning is as below:

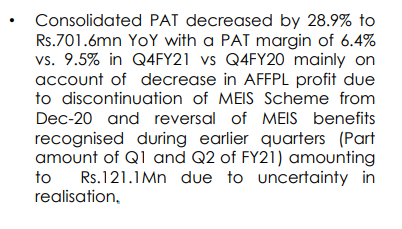

Still curious to know the reason for loss in the processing division for Q4FY21 although market seems to have respected the reasons given in the filing.

Disc: Not invested.

3 Likes

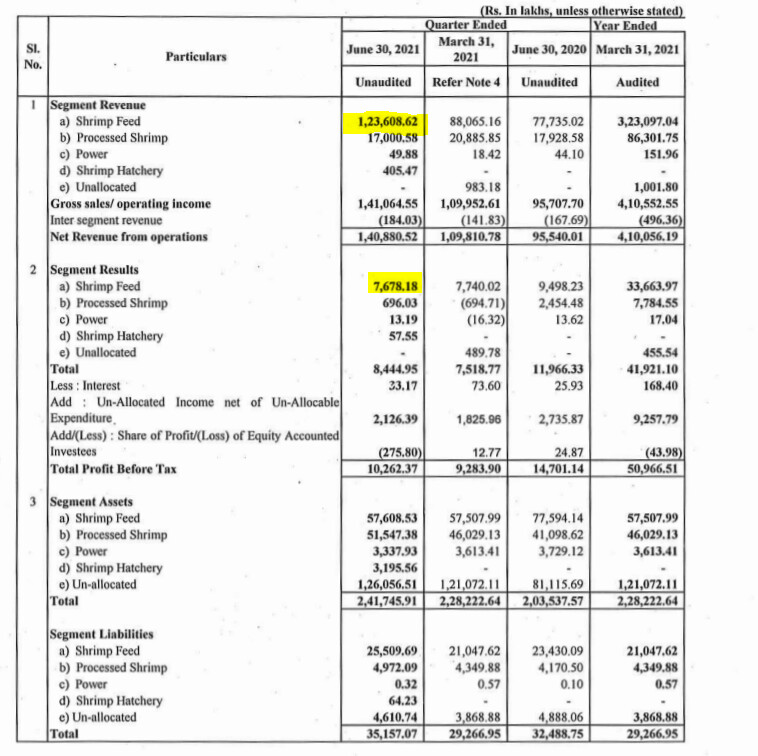

Presentation out. So MEIS discontinuation and reversal of MEIS for Q1, Q2 amounting to 12cr. There is also an increase in RM price and other expenses.

Few highlights from the presentation

-

Sales volume(MT) in Q4FY21 increased in shrimp feeds segment by 14% YoY due to increase in culture and in Processed shrimp segment decreased by 18%

Shrimp Feed Consumption in India during FY 20-21 also reduced which was around 10 lakh MT as compared to 11.50 lakh MT in FY19-20. However during FY21-22 due to increase in Global demand and stable farm gate prices, shrimp culture is expected to come back to the levels of pre pandemic period. -

Shrimp Feed sales during the year 2020-21 is 4.74 lakhs MT as compared to 4.85 lakhs MT during FY20. Company sales reduced marginally by 2% as compared to overall market reduction by 16.5%, mainly due to lockdown and non stocking by farmers due to non availability of seed during Q1FY21.

Company has not only kept its farmer base intact, it is also added new farmers and new areas to its sales network during FY21. -

Export sales during FY21 is 11,518MT as compared to 13,397MT in FY20, a decrease of 1,879MT (14%), where as overall market reduced by 20 to 25% mainly due to continued lockdowns, closure of malls & restaurant etc

5 Likes

Q4FY21 concall notes

(reorganized)

-

USFDA advised Avanti frozen foods to recall, based on reported 6 cases of contamination. Most of the shipment would have been consumed. Since the volume of the product associated with this incident is insignificant, company does not expect any impact on company’s reputation. Company has adequate insurance, engaging consultants to strengthen company systems and procedures to avoid such incidents. In past 25 years we never had such issue. Customers know this and they are cooperating. The first notification was in Feb. After that we slowed down and were double checking with external labs. We had reduced our volumes. Our order book is full but Going little slow on exports in Q1 because we want to have double check on our quality control so that things don’t happen again. Root cause analysis investigation has been conducted. Cant disclose it because the case is not closed yet. We are treating this as a one-off. Salmonella occurs from transmission from humans also due to personal hygiene.

-

Outlook- Shrimp culture started in Jan-Feb with good weather, farmgate prices, good quality seed. These conditions are good for farmers. First crop is very good compared to 2020 and also compared to 2019. Last year seed availability was an issue. Broodstock has to come from Hawaii/Florida and the flights could not come due to COVID. So many farmers could not operate. Second crop also looks good but will depend on monsoon and climate. Good shrimp culture is expected to continue in H2 of 2021. New farmers have come and expansion has happened in Orissa and West Bengal. Demand for shrimps is expected to be good from Thanksgiving, Easter, Christmas, new year etc.

-

Govt allocated 10900cr over next 4 years to Ministry of food Processing industry in 2020. They announced PLI scheme on incremental exports of seafood products over next 6 years starting 2021-22. PLI envisages an incentive of 6% for normal products and 10% for value added products. Condition- min investment of 75cr in first 2 years and achievement of min 5% CAGR on sales for 6 years. Avanti has made an application and awaiting response. RODTEP will be applicable from Jan21 but details are yet to be announced, waiting for announcement due next week.

- Our current capacity itself is underutilized so will PLI be useful? We can do 5% CAGR for 6 years, which is basic requirement. We planned that in the first 2 years we will focus on utilizing the existing capacities and then are working on new expansion plans with new products and new markets. We will accelerate after 2 years and meet the average 5% CAGR requirement of PLI.

-

Feed business

-

Shrimp feed consumption went down 20% to 9.55 LT in 2020 from 12LT in 2019 due to COVID. Expecting growth of 10-15% to 11LT in 2021. Avanti did 4.55LT in 2020 and expected to grow 15% to 5.25 LT. Will maintain market share of 48-50%.

-

Increase in RM affected margins. Soyameal price went up to 47rs vs 43 Q4FY20, fish meal touched 93rs vs 90 rs in Q4FY20. Current price of Soyameal is 77rs, fish meal is 93. Exorbitant prices. Price hike in Jan20 of 3.8rs /kg which could absorb some increase. Price hike of 5rs per kg in 2 tranches between April-June 2021. This takes care of some RM increase but fishmeal and soya meal are increasing unabatedly. Frequent price increase cant be taken because of govt. Company is hoping that soyameal prices will stabilise after fresh crop comes in October. Fishmeal prices can stabilise after fish catching ban is lifted from west coast in early August. One of the increase in soya prices is exports- because American and Brazil crop failed.

-

Marketing expense has gone up. All competitors sorted to huge discount to increase their sales. Also imported feed was available at a cheaper price as imported feed had concessional duty of 5% against normal duty of 25%. This duty was then increased to 16% in the budget. Avanti spent 1 time incentive of 17.5cr to issue coupons to farmers to retain all farmers and add new farmers to maintain our growth rate.

-

-

Processing

-

Shrimp exports are expected to grow 10-15% in 2021. Avanti did 12192MT in 2020, and expecting 12700MT in 2021.

-

De-growth of 20.15%. MEIS is a major reason. Gross revenue includes 5% MEIS and 3% duty drawback on FOB value of exports. Govt restricted MEIS to 2cr from Sept-Dec, and then completely withdrew from Jan21. During H1, 12.11 cr was taken as MEIS on accrual basis. There is uncertainty on getting this from Govt so company reversed this in Q4. As and when it is received, we will account for this. So post this reversal, we have not factored any benefit in FY21

-

Volume drop was mainly due to container shortage. Container prices have shot up from 3300 in Jan to now 7100 per container. Q4 volumes also decreased due to container shortage. RM cost also went up

-

There were also few other issues- USFDA issue was first notified in Feb, Lower footfall of workers due to COVID

-

Containers in highs seas are taken as stock in transit at cost value. If the opening and closing transit is the same, it does not affect the top line.If closing stock is higher, revenue and profits come down to that extent and is reflected in next quarter. Numbers are accounted for on reaching customer. Such containers were 114cr vs 90cr in FY20. Profit will be booked in Q1.

-

-

Capital allocation- Generated 300cr FCF in FY21. Management considering 1) Increase capacity of shrimp feed 2) Fish feed 3) PLI related capex. Question of buyback has been considered couple of times but still we considered that we will need funds for capex in the long term. Issue is kept open but in present condition we are confident that we will be able to invest in the business. Some projects could not be implemented due to COVID, we will look at these when time is right.

Again an unconvincing reply from management on buyback.

19 Likes

2 Likes

| Country Name | May-20 | May-21 | JAN-MAY 2020 | JAN-MAY 2021 | JAN-DEC 2020 |

|---|---|---|---|---|---|

| ARGENTINA | 1,211 | 1,351 | 5,703 | 6,601 | 17,340 |

| CHINA | 1,069 | 845 | 4,621 | 3,011 | 10,871 |

| ECUADOR | 5,773 | 16,849 | 37,706 | 67,722 | 125,818 |

| INDIA | 8,600 | 31,972 | 99,722 | 117,634 | 271,831 |

| INDONESIA | 13,006 | 17,235 | 63,166 | 75,280 | 160,744 |

| THAILAND | 2,654 | 2,878 | 12,122 | 12,827 | 40,510 |

| VIETNAM | 3,316 | 6,151 | 16,387 | 23,917 | 65,459 |

| Report Total: | 37,814 | 80,327 | 257,601 | 326,074 | 746,010 |

Data for Shrimp imports into US. Source

India is showing some traction. Good growth in Jan-May numbers

7 Likes

Not a mature industry yet?

Two interesting points in the article:

1: “Shrimp was the big winner in the US market: what we’ve seen in the pandemic is that consumers have moved towards food they are familiar with – they buy what they know to cook at home. There were huge leaps in retail sales during 2020: frozen raw shrimp, a $2 billion industry, went up by an incredible 47 percent, frozen cooked shrimp by 25 percent. We haven’t seen this kind of growth rate in a mature category in a very, very long time,” he adds.

2: “India is targeting the US in a big way, but without a lot of product innovation and marketing it’s difficult to sell more shrimp to the US without losing out on price, so that’s basically a big problem for that industry and in 2020 they dropped in both volume and value – they’re back to 2017 volumes but quite a bit down in value. It was a tough year for India – they really had problems with lockdowns. There were problems in March and April, in the summer and in December, when they suffered because they could not export enough product and there was a delay in the season,” he notes.

“On the price side it was a bit of a roller-coaster because supply was so volatile, but the prices were not as low as in Ecuador. And they’re starting the year quite well now thanks to their strong position in US retail – India is the dominant producer of US shrimp retail products and US retail has been going very well. During lockdown, however, when the shrimp peeling stations were out of action, they had to pivot towards the Chinese market with their unprocessed shrimp,” Nikolik adds.

Can anyone point us to the historical volumnes and $Value of exports for last decade?

Disc:Invested

5 Likes

you can check here Aquaculture Sector | Tijori Finance

1 Like

1,000 shrimp containers stuck in Chinese ports, half of them from Andhra Pradesh

“We have already approached the Ministry of Commerce and talks are on at diplomatic level with China to resolve the issue,” Indra Kumar said. Shrimp exports from Andhra are now having their fingers crossed and praying for a positive outcome.

Virus traces?

China suspects coronavirus traces on the outer packaging

Rs 1,200 crore: value of the shrimp 50 companies have been suspended by China

China is second largest importer of shrimp from India after the USA

46.44% of shrimp exports to China

4 Likes

The management’s salary is too high in my opinion. The managing director (Indra Kumar) and their CFO received 19.4 and 13.7 crores in salary respectively in FY21.

I know it’s a family run business and the promoter being the management here is entitled to share in profits. But this much seems unfair to me and especially when it was not a good year for this industry and their business which remained flat.

Is it a cause for concern?

1 Like

I think the management is being too conservative here. A pertinent question was asked regarding capital allocation that even after provisioning for capex of 75 crores in each of next two years (PLI scheme), the cash they are generating to the tune of 250-350 crores should be enough to take care of it. Capex wouldn’t be of more than 200 crores for sure.

They already have more than 1000 crores of cash on books. What will they do with this? Even the dividends aren’t attractive. Buybacks would create immense value at this stage. They could easily consider buyback worth 400-500 crores, but they are simply not interested in returning money to shareholders!

1 Like

Q1 2022 report

Excellent volume growth in feed business but severe margin contraction due to RM increase.

Feed Margin at 6.2% vs 12.2% yoy and 8.8% qoq. Hopefully the margins will bottom out here.

3 Likes

Hopefully yes. Soya prices have already reduced significantly in past few days. Amazing growth overall.

2 Likes

Fantastic growth in feed business. Hopefully the processing volumes too show a good growth.

Very good results! Good to see the growth finally kicking in. The last Concall was very positive, while several industry people were very concerned and many were expecting loss in feed segment. I think co has surprised positively

Disc: invested in family accounts

13 Likes

Q1FY22 Presentation link

Concall on 21st Aug at 4pm

Some imp points

Feed Business

-

The company is expected to maintain its market share of 48% to 50% in FY22

-

Shrimp Feed sales during the Q1FY22 is 1.74 lakhs MT as compared to 1.13 lakhs MT during Q1FY21. Company sales increased by 54.5% due to increase in farming area and conversion of farmers from other feeds during Q1FY22 compared to panic harvesting and delay in farming during Q1FY21.

Processing

-

Global market are gradually picking up and recovering from COVID-19 and increasing in demand from retail sector is expected to come back to pre COVID-19 levels as travel is allowed and malls, restaurants & public eating places have reopened. Production & exports of shrimp in 2021 is estimated at around Rs.6.50 Lakhs Mts a growth of about 10-15% over previous year.

-

Export sales during Q1FY22 is 2,451MT as compared to 2,611 MT in Q1FY21, a decrease of 160MT (6.1%), due to non availability of containers and slow down in exports by implementing more quality checks in view of USFDA recall

6 Likes