I believe recent downward pressure is also due to import duties on shrimp from US government. This will hamper the frozen foods finished product which was key growth driver for the company…

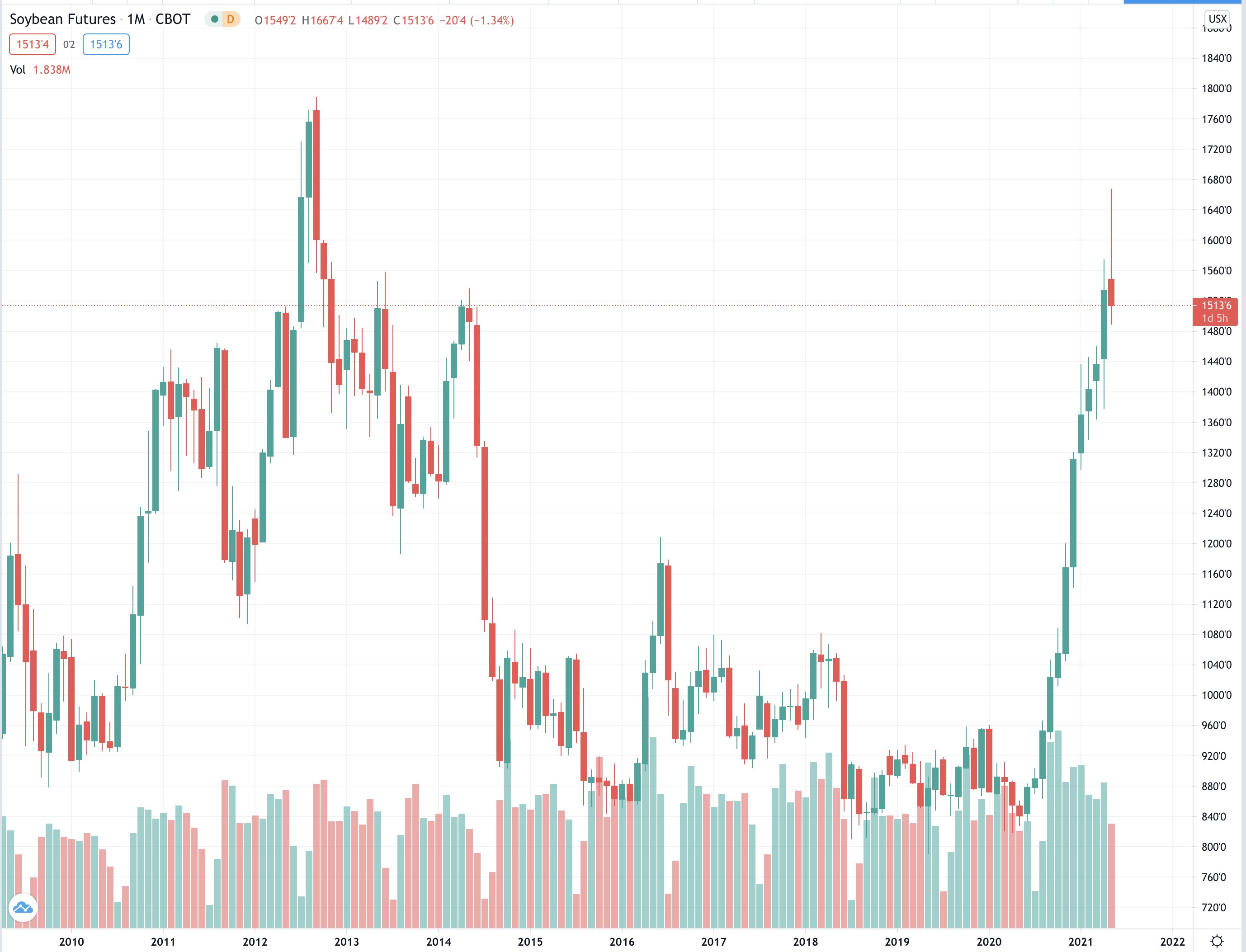

Current challenges are due to increase in soya prices (raw material) and import duty in US. Used the low prices to double down the position.

In the past, the company has come out stronger from such events

3 Likes

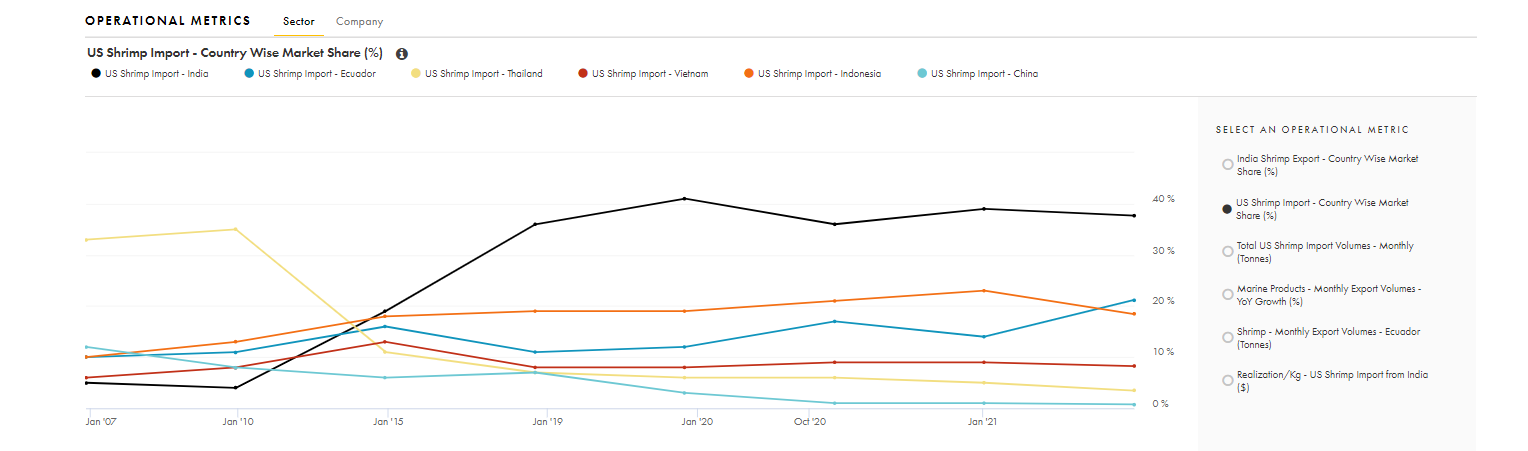

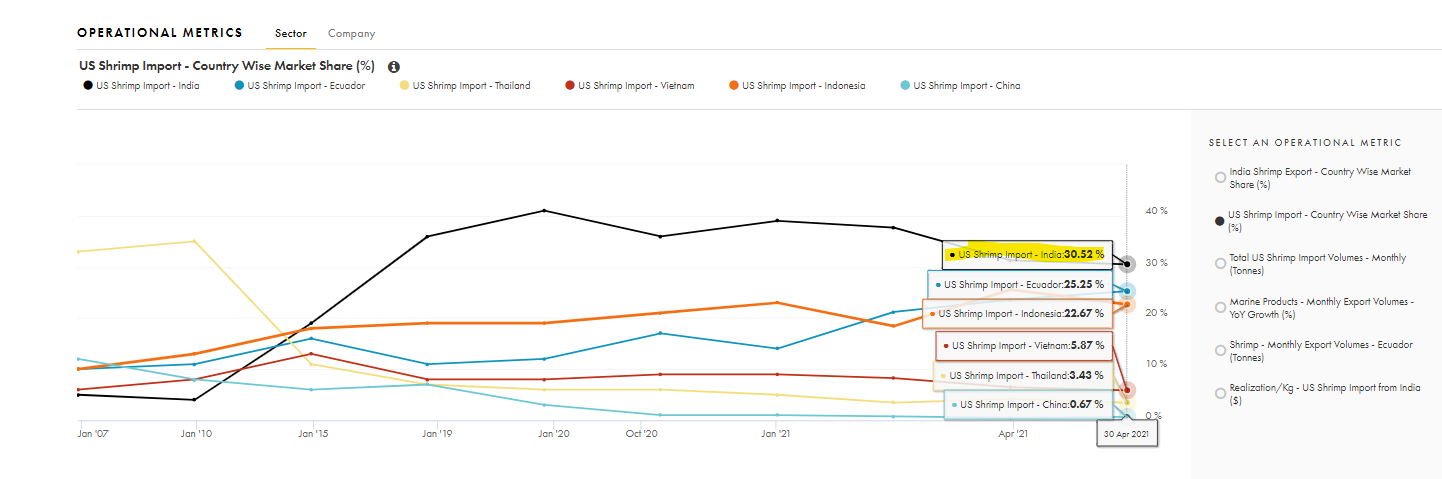

Indian companies continue to lose marketshare in US shrimp imports. Hopefully after spike in march there will be some reversal

3 Likes

I made the following note for a recap of the story.

The big picture-

- Feed business: Avanti has a strong brand and ~48% market share in an industry that has struggled over last 2-3 years. Shrimp production and feed consumption was down 20% in 2020. The industry was hit with bouts of diseases, cyclones and low shrimp prices. FY19 saw a dip, and even CY2020 (part of FY21) has seen a dip. There is a potential for industry to come back on growth path going forward. Feed business has some traits of FMCG (negative/very low working capital), but has somewhat limited pricing power. Growth in this segment will come mostly from industry growth now. The large cash on books can not be used meaningfully in the domestic feed production because Avanti can itself setup a new plant fast at low cost.

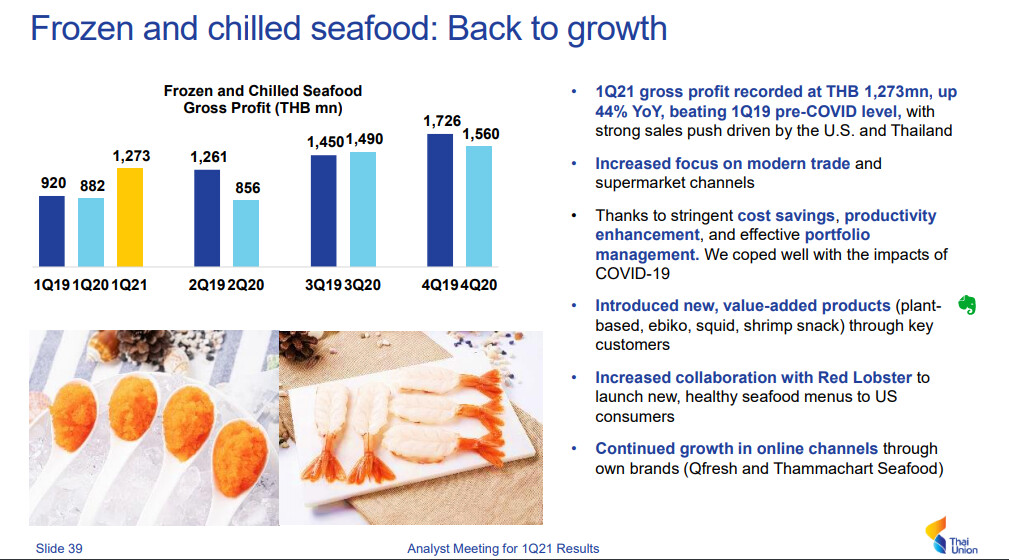

- Processing business: This is a labour intensive and high working capital business. Avanti has been trying to do more value added products that no one else does in India. They have done a good job at scaling up this business and there is a good room to grow here. The partnership with Thai Union can help them in distribution in the US market.

Near term monitorables

- Very sharp increase in Soyabean prices (attached Soyabean futures chart) will impact the margins. There was a price hike last year and they might need to take another increase, but farmer economics need to improve for this to be possible.

- Industry coming back to growth path: Management has guided 10-15% growth in CY2021 after a de-growth in CY2020.

- Opportunity to capture some of the 10-15% of feed market which was imported and now under duties

- Discontinuation of MEIS scheme has hit the processing industry. An alternative is in the works but no clarity yet. PLI scheme is a possibility.

- As the world opens up more after COVID, the shrimp consumption can go up.

- There is no clarity on utilization of cash. Management seems to have decided not to raise dividend payout and has not given any convincing answers on expansion into allied areas. My inference is that feed doesnt need capex. Processing may not need much capital to increase capacities either, and it will be in small steps. Unless management has plans for acquisitions, it doesnt make sense to hold so much cash. Moreover, the cash levels are increasing every quarter. Any clarity on cash would be a positive trigger.

12 Likes

Today waterbase declared their results and they have declared losses for the Q4. In their press release, they cited higher raw material prices impacted their margins and second wave also impacted their business ops.

Separately, Thai Union in their latest investor presentation cited that, their income from associate cos during Q4 was boosted by strong performance by Avanti!!

Will be interesting to see Avanti Q4 results and their business outlook

11 Likes

If you look at waterbase Q4 comparison yoy, they did not do good last year either and had reported a loss. The sales and COGS are more or less at same level yoy, though cost pressure seen qoq.

Commenting on the results, Mr. Ramakanth V. Akula, CEO said, “We are pleased to have reported an improved performance in the fourth quarter. There has been a meaningful improvement in topline compared to the immediately preceding quarter though activity levels are yet to revert to pre-pandemic levels. However, we have witnessed inflation in raw material costs, especially soya, which has resulted in pressure on margins.

Importantly, we continue to make progress on transformation of our revenue model. The proportion of cash sales continues to rise and we are committed to enhancing the quality of revenues. The initial benefits of this initiative are discernable from the improved balance sheet. Other encouraging developments during the quarter have been the addition to our dealer network and the resilience of the farmcare products business.

The two cyclones have impacted the farming activity on the east and west coasts, though the damage is yet to be assessed. Some of the key farming regions have been more severely impacted during the second wave of the pandemic in India, but we are confident that domestic shrimp production will eventually rebound from these disruptions. Activity levels are improving and farmer sentiment is buoyant in Andhra Pradesh even as global shrimp prices have held firm. Key global consumption centres like China, USA and Europe have made steady progress on their vaccination programs and are set to emerge from the pandemic. The reopening of these economies will unleash pent-up demand and significantly boost consumption raising the requirement for high quality farmed shrimp in the months and quarters ahead.”

1 Like

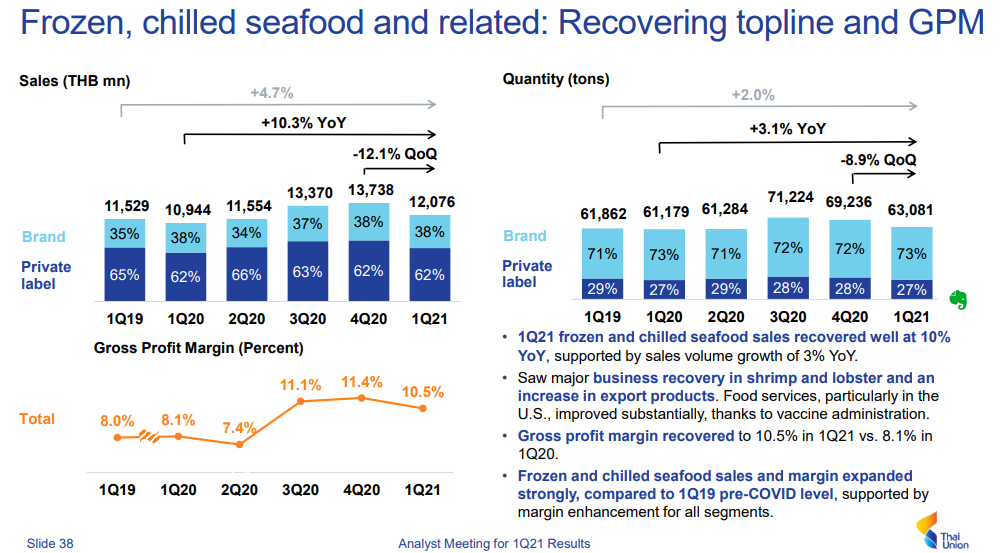

Thai Union Q1 2021 presentation mentions that shrimp business has done well and grown over Q1 2020. Good growth in US and Canada. Thai Union gets 45% revenues from US/Canada and 27% from EU. They have guided 3-5% growth for 2021.

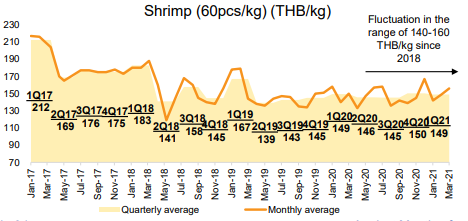

Shrimp price chart

7 Likes

2 Likes

Any information on who are these 6 companies? I searched many articles but none of them mentions the company names.

Avanti’s exports to China is very small.

Shrimp imports (MT) to US

2019: 698,358

2020: 746,010

So in a COVID year, imports have gone up by 6.8%.

Jan-April 2020: 219,791.

Jan-April 2021: 245,747. Growth of 11.8%

Imports in US from India for Jan-April have come down from 91,122 in 2020 to 85,662 in 2021, down 6%. Ecuador continued to gain share here.

Let see how Avanti performs in this quarter. Guidance was 10-15% growth for Indian Shrimp industry in 2021.

Source: Shrimp Imports

3 Likes

3 Likes

Results are out.

Final Dividend of Rs. 6.25, per Equity Share of Re. 1/-

2 Likes

2 observations from the latest results:

- ~7Cr. loss in the ‘Processed Shrimp’ segment for revenue of ~209 Cr.

- Under the current asset in B/S, a new category (almost Negligible ~2 Cr) is shown - Biological Assets other than Bearer Plants. Just wondering what it can be?

Any thoughts? Else, I will parse the Conf Call and AR as and when they are available.

1 Like

I did expect the feed margins to be under pressure due to high Soyabean prices (some relief due to some inventory they would have carried). However, the loss in processing was a negative surprise. They had done a 22cr profit in Q3 on a processing revenue of 239cr. Lets wait for the presentation and concall for the reasons. Cash flows continue to be good, net cash flow of 328.6cr vs 178.2cr last year. Cash on books almost 1250cr. Small increase in inventory levels.

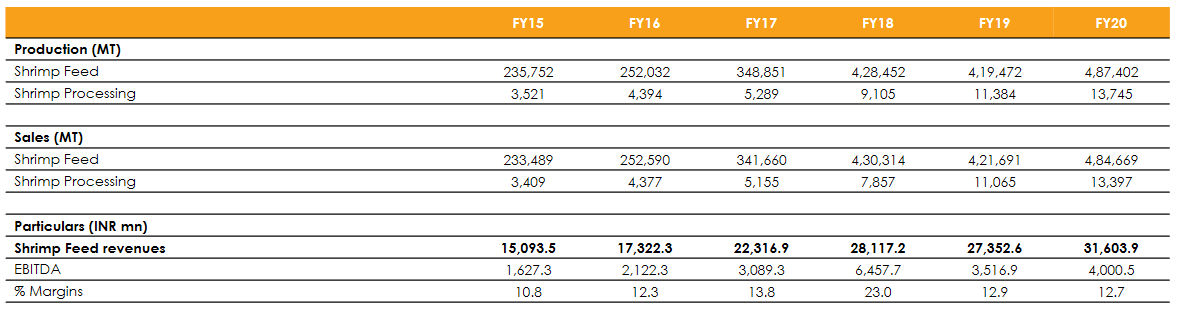

| Q4FY21 | Q4FY20 | Growth | FY21 | FY20 | Growth | |

|---|---|---|---|---|---|---|

| Feed business | ||||||

| Sales | 880.65 | 764.6 | 15.18% | 3231 | 3160.9 | 2.22% |

| PBT | 77.4 | 84.72 | -8.64% | 336.64 | 318 | 5.86% |

| Margin | 8.79% | 11.08% | 10.42% | 10.06% | ||

| Processing | ||||||

| Sales | 208.85 | 270.64 | -22.83% | 863 | 954.9 | -9.62% |

| PBT | -6.95 | 30.46 | 77.84 | 97.8 | -20.41% | |

| Margin | -3.33% | 11.25% | 9.02% | 10.24% |

5 Likes

Apex Frozen has declared a decent result. Revenue up 30% from 140 in Q4FY20 to 182cr in Q4FY21. Cost of materials is down from 127 to 112cr. In comparison, Avanti processing division has turned a loss.

1 Like

1 Like

That explains the reason for unexpected loss in processing division.

The recall is published on 25-Jun on FDA website but concerned with products (involving multiple brands-Censea/Hannaford/Open acres/Waterfront Bistro/Honest catch/COS/365/Meijer ) that were distributed from late December 2020 to late February 2021.

Let’s see how it spills over to current FY and what’s management’s point of view to the investor community.

2 Likes