The article talks about an ongoing research by few Americans on developing new ways to grow and harvest shrimps…mainly creating the ability to setup a shrimp farm at any place rather than just coastal areas. This could be an interesting development once their process develops and reaches economic viability.

At any given point, in every industry there are several key developments going on and along side the business is carried on in that industry using the traditional methods/process. So, we don’t have to be scared of such developments or research unless they come to a mature stage. Yes, it is good to be aware of such insights…but in my humble opinion one shouldn’t be scared about shrimp processing industry going for a toss in India due to this research. There will be a lot more which one needs to factor in…like even if this technology evolves…then will it be viable on cost front? If yes, then will it be cheaper to process shrimps using this technology in an Indian city rather than New York…so on and so forth.

The research if successful may be positive as shrimp farming will not be restricted to coastal areas and that would increase production as well as consumption of shrimp when it could be readily available anywhere. The impact on shrimp feed demand will be positive.

Lots of news around India’s sea food exports to China facing major issues due to ongoing India China conflict and shipping container problems. What kind of impact will it have on Avanti Feeds? China being the biggest sea food market for Indian firms.

I know they do. I want to know specifically for Avanti what this may mean. My link already covers that Chinese markets are big for Indian shrimp exports.

Avanti Feeds’ consolidated net profit jumped 46.47% to Rs 86.20 crore on 0.78% decline in revenue from operations at Rs 915.43 crore in Q3 December 2020 over Q3 December 2019.

Do we know when is the concall scheduled for? Normally its a day or two after the results but this time its been almost a week without any notification.

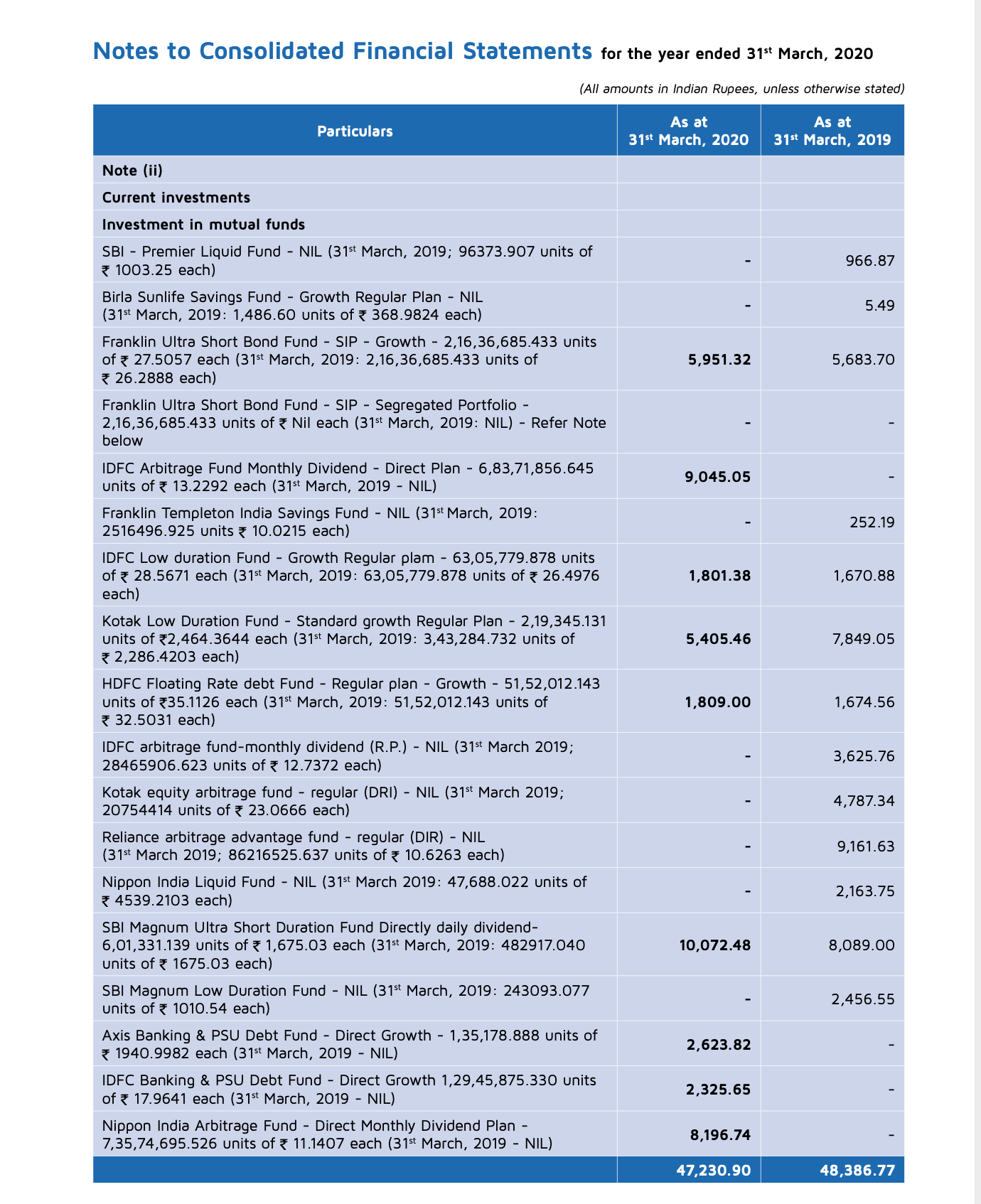

Hi, does anyone knows where to find cash available with the company? I was hearing to the concall and there was a point made about large amount of cash available with the company and suggesting buy back. I tried to find cash available on screener. But I couldn’t find it. So any pointer will be helpful.

Aquaculture industry- Expected to improve. Main season started on a good note in Jan.

Global production was 3.5mn ton in 2020 vs 4 mn ton in 2019, decrease of 10%. Forecast for 2021 is 3.8mn ton, growth of 8%.

In India 2020 production was 6-6.5 L MT vs 8 L MT in 2019, decrease of 19%. 2021 forecast is growth of 10-15% to reach 7-7.5MT. Feed consumption 9.55L in 2020 vs 12L in 2019, drop of 20%. 2021 is expected to grow 10-15% and touch 10.5L MT. Avanti did 4.55 L MT in 2020 and expected to touch 5-5.1 L MT. Expected to maintain 46-48%. Seeding is going on actively. We keep monitoring seed offtake and also feed distributors finance part of the farmers. Avanti hatchery seed offtake is quite good. Our staff is going around in the market.

Avanti shrimp processing was 12192MT in 2020, expecting 12500 MT in 2021. Value added products and new markets.

Import duty on import of shrimp feed and fish feed increased from 5% to 15%. Long awaited decision. Feed imports were 10-15% of the market. In 2020, 1 L- 1.15L MT was imported out of 9.5 LMT from China and Vietnam at lower prices as they were getting export benefit. With this increase, imports will stop

PLI scheme details to come but it should be helpful for players like us.

10900cr to ministry of food processing over 5 years.

MEIS withdrawn has significant impact. Alternative RODTEP will come

AP govt passed act to control quality etc. Compliance will need some efforts.

RM- fish meal and soya meal was stable for some time but now increasing. Soya 42.17 in Q1, 40.84 in Q2, 43 in Q3. Wheat reduced slightly

Entering into fish feeds and other feeds (pet foods) and bringing in new species of fish. There is lot of interest in high valued, high protein fish like grupper(?), seabas. Plans were impacted due COVID. Looking for organic and inorganic growth.

Freight rates have gone up significantly due to shortage of containers and space in shipping lines. Trying to negotiate and pass on to consumer.

My notes- Interest in Avanti seems to be fading but it seems that things are about to change for them. Finally things should start coming back to normal. They did 4.57L MT in 2020. With 10-15% growth in feed along with capturing some market of import substitution, I think they can touch 5.25L MT. This can be a big jump in profits. However, we need to see two things 1) the impact of MEIS withdrawal 2) Soya is rising again

It is reassuring that things can only get better from here on. However, is there any weight in the belief that this industry and stock will never get a huge valuation due to it being prone to disastrous situation when there is disease outbreak?

And if so why would one hold on to a stock of such company if there may not be a huge rerating?

Disc: I am still learning, do not understand a lot yet so please ignore any naivety in my questions

Economies around the globe are absorbing the ripple effects of the disruption on the seas. Higher costs for transporting US grain and soybeans across the Pacific threaten to increase food prices in Asia.

The co.s share price is constantly trending downwards since last 3 months. The major risks - raw material prices, Freight issues, regulatory tarrif seem to be adequately priced in currently.

Are thr any other risks that long-term investors\other valuepickrs are aware of that’s being factored in? Or is it just markets being a voting machine in short-term?

I think the key concern for the market is growth. We have seen enough of raw material price, cyclone etc in last many years, and company gets out well after short term blip. But now the concern has moved to fast growth vs slow growth vs no growth . Market will value depending on how management deploys cash and the overall shrimp market growth . Known risks generally get discounted well in advance.

Disclosure- invested for 5+ years from lower levels