This scheme is dependant on state govt as well as the beneficiaries. States are starved of funds. Beneficiaries with free cash flow will be able to benefit. Avanti will definitely benefit if state govt also support. See the attachments.

3 Likes

All seems to look good for Avanti feed- the results, the govt’s infusion of cash, but the stock prices seem to quote a different story ! wonder why?!

Also the delivery percentage has been low compared to past month and relative strength index has been in negative zone this week.

Q1FY21 results concall brief - posting it a bit delayed, almost a month after concall.

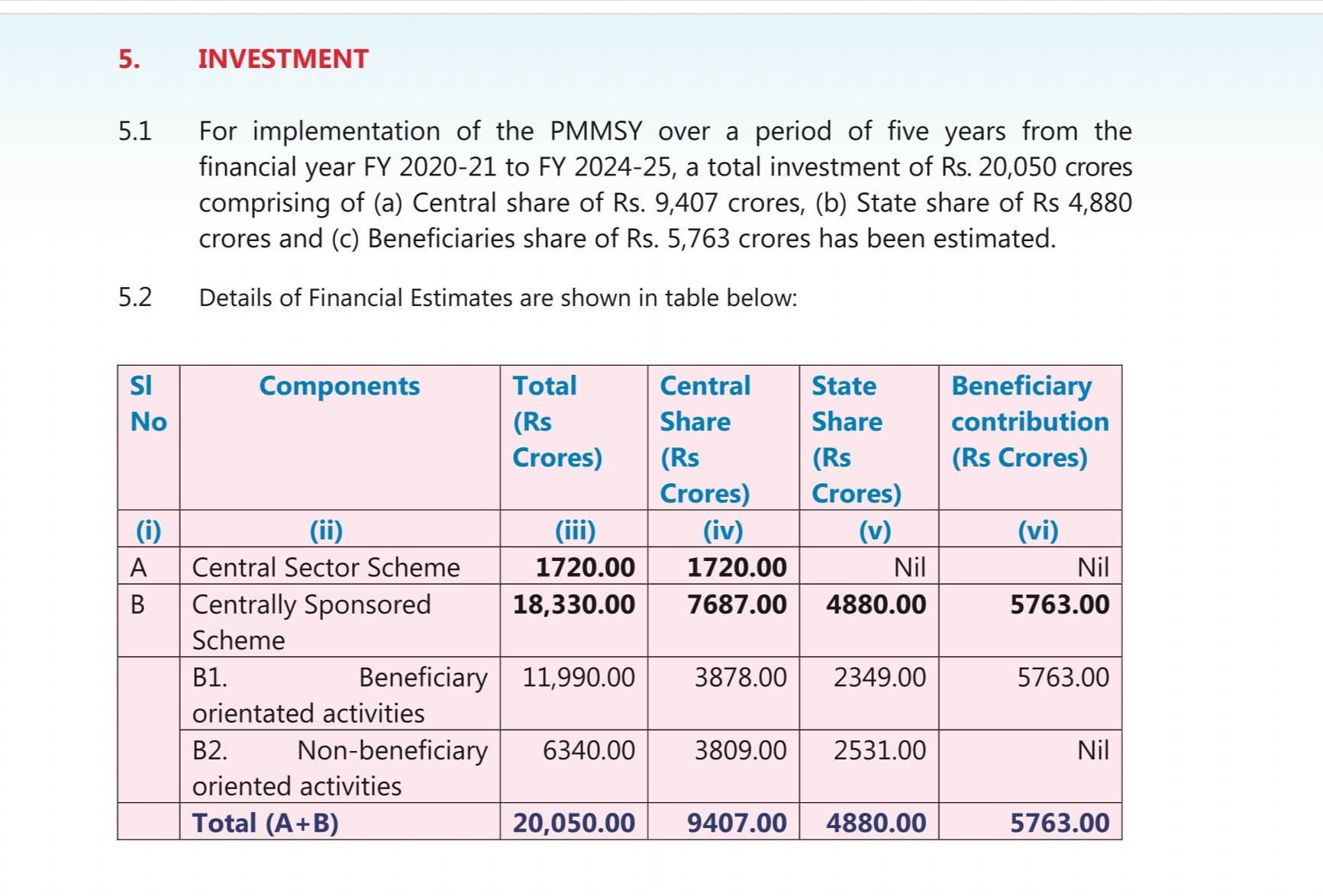

Attendees - C Ramchadra Rao, A. Venkata Sanjeev, Alluri Srinivas, Ms. Santhi Latha - GM Fin. and Accounts, Ms Lakshmi Sharma - company secretray

- Hatchery division is ready to start now. Statutory clearances awaited and expect to start commercial operations from this year-end.

- Government is working on export incentives - expect tax breaks which will compensate for withdrawal of incentives earlier. It will help farmers. Export incentive accounted in Q1 was 8 Cr. and tax breaks of 4.6 Cr.

- Government was seeking information on taxes paid etc. (my comment - this looks good. While the government is trying to achieve fishery export targets, good part is government is eager to hear about issues and address that. It will help to sort out issues like GST on raw fishmeal etc. along with other issues)

- 1 lakh crore export target for fishery products by Indian Govt. (need to work check Shrimp % and shrimp food% as part of Shrimp price in that)

- The government is working on developing infrastructure facilities as part of post covid package. It will help farmers in long term. Also working capital needs of farmers might get addresses to increase shrimp culture.

- no salary cuts for employees, all dues paid, 100% bonus paid, all incentives due were paid as like any normal year. This shall give more confidence in the company and loyalty for employees

- China Market - demands more of commodity-like products and Avanti is focussing more on value-added products. Current issues and tax conflicts will take some time and in 5 to 10 years period it will be good market.

- Foreacst - conservative estimate is to maintain last year results in this year.

- growth prospects - shrimp consumption is expected to go up. Company increased market share year on year despite many feed manufacturers etc. Overall - value added products, more capacity utilization and addition of capacity are avenues for growth

- inorganic growth using cash reserves - not inclined much for inorganic growth bcs of grey areas in inorganic growth. Company is evaluating opportunities available but not found anything really interesting in last 2-3 years. The company will keep on doing due diligence on opportunities available.

- US exports - other countries have taken more share - its due to India getting badly affected by Covid and manpower shortage in the manpower-intensive industry. India will regain its position in few quarters

- Blue revolution - 46-47K current exports of fish and fish related products. Want to double to 1 Lakh Cr by 2025. Area of shrimp culture can go up. Infrastructure development and running costs funds along with post-harvest infra is expected to improve.

- Shrimp processing US revenue share - currently its 75 to 80 for shrimp processing revenue. Other markets are not giving that much value like US

- buyback - there is no proposal of buyback as of now. Safe investments company is looking into with 6 to 7% returns on cash balance

My comments -

Overall PMMSY looks good for Avanti Feeds and we can expect doubling revenue from shrimp feed segement in 5 years on min. side. Upside to this possible due to increasing shrimp culture and further improvements in market share.

Overall growth for Avanti will be further supported by Shrimp processing business and newly coming up hatchery business (need to see size of this opportunity).

Decreasing ROE may remain ongoing concern for next 2-3 years but considering management quality and company position we can expect moderate returns on this investment for next 4 to 5 years.

11 Likes

This article series from global aquaculture summarizes really well the global shrimp industry, how and why it grew in India, how COVID impacted Ecuadorian shrimp prices and why Ecuador started gaining market share in US. The key takeaway for me is India is starting to make its own vannamei broodstock (backward integration in a way).

10 Likes

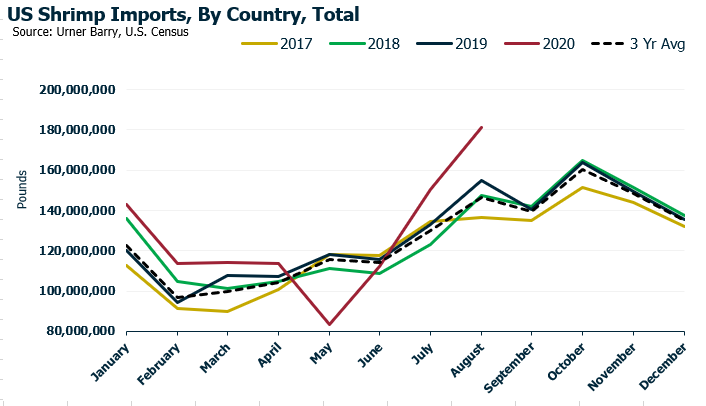

US August Shrimp Imports Set All-Time Record

Came across this update today. Surprising to see the recovery given that everyone (including me) were concerned about the consumption given closure of restaurants etc worldwide.

17 Likes

Just did some digging around. Apparently…

-

One of the most comprehensive surveys of U.S. diet from 2007-2016, the National Health and Nutrition Examination Survey, researchers finally have accurate numbers on seafood consumption in the United States (pre-pandemic). They found that by weight, 63% of seafood is consumed at home, with the majority coming from retail and a smaller proportion from takeout.

-

The demand for sea-food was always there even during the Pandemic

Fresh and frozen seafood sales continue surging in the United States, as Americans continue to eat more meals at home during the COVID-19 pandemic. And, as a result of increasing demand for grocery purchases, supermarkets and grocery delivery services continue to expand. Overall fresh seafood sales jumped 41.6 percent for the week of 12 July, according to Information Resources Inc., while frozen seafood sales climbed 41.9 percent.

Sources: https://sustainablefisheries-uw.org/seafood-consumption-statistics/

https://www.seafoodnews.com/Story/1175473/Seafood-Fastest-Growing-Supermarket-Category-During-Last-Week-of-May

https://www.seafoodsource.com/news/premium/foodservice-retail/retailers-expand-as-seafood-sales-continue-booming

The demand for sea-food may have also been driven due to

-

Meat plants being shut down https://www.theday.com/article/20200621/BIZ02/200629901

-

Scarce supply of fresh-water fish

https://www.foxbusiness.com/industrials/frozen-fare-fishing-industry-coronavirus

8 Likes

This is wonderful news,but let me play devil’s advocate here.The high imports of August might be due to 2 reasons:

1)The importers want to avoid delays or uncertainities of shipments due to another lockdown in India,and want to ensure supply for their holiday season.

2)Because the prices currently are at the lowest levels in many years,they want to take advantage of that and increase inventory.

But in either case its only a short term impact and the secular trend of increasing shrimp consumption globally looks to continue especially considering rising Chinese percapita consumption of shrimp.

US import data of September and October will show if my point 1 is valid or not,since usually that is the time when US imports are high

4 Likes

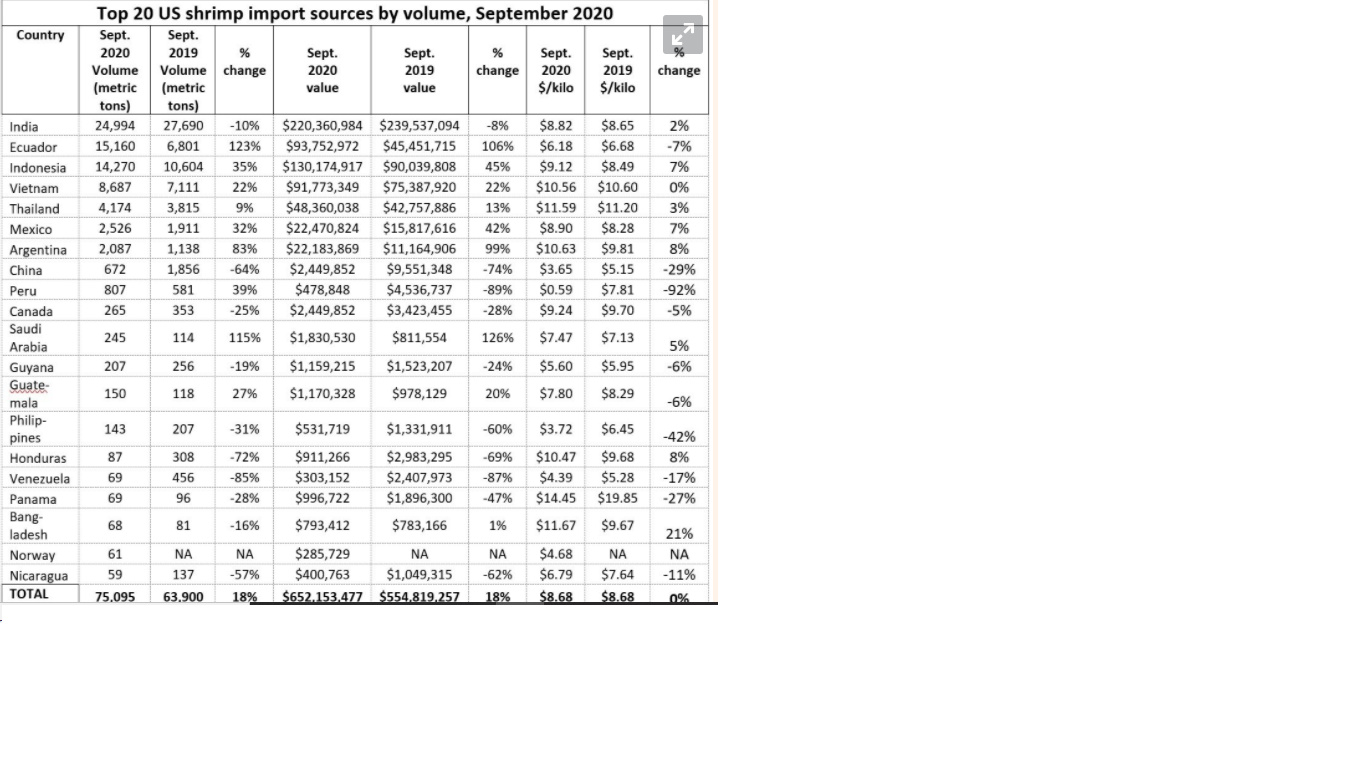

US Sept2020 Shrimp Import is encouraging.18% jump in volume of total import. India Volume down 10% YoY. Price Realization per KG is encouraging up 2%.

2 Likes

India Shrimp price is stable mostly. May be effect of 10% less farming this year also better US and China demand. Also Ecuador shrimp harvest at record level .despite better demand from China and US ,farmgate price in Ecuador going down quickly.

avanti feeds is the kind of company which can deliver growth even if the market de-grows a little. it is the kind of company which can improve its market share inpsite of having 50 % Market share. It is similar to Apl Apollo in quality- both can improve its market share in a shrinking environment , both have around 50% Market share, both companies are like a branded player in a commodity sector

Sometime i have learned with Avanti over the years is that we dont have too worry too much even if the market de grows. Avanti can still surpise us postively with the results.

11 Likes

Strong Q2 results by Avanti in the current environment. Despite degrowth in US import volumes over the last few months & flood situation in AP, company maintained higher operating profits ( as compared to qoq, yoy). Cash levels are swelling ( almost doubled compared to March levels). Op profit from processed shrimp almost doubled compared to H1FY 20. Higher volumes in feed segment is encouraging and implies business activity is slowly picking up. Raw material prices continue to remain softer and aiding the margins partly. Finally, hatchery division starting shortly. Hope it becomes a growth engine in future. Will wait to hear managements commentary on industry trends and their future growth plans ( esp with large cash on their books)

9 Likes

Hi can anyone provide more insight into the hatchery business?

As per last concall 2 days ago, they said ‘400million capacity in phase 1 out of which 15% utilisation has started resulting in 7CR turnover’.

I am unsure if this means 7CR is the expected turnover from 15% for the entire year or what if any of the projected revenues from the Shrimp Hatchery?

Management has already mentioned that hatchery is a small thing and will not be significant for revenues. However, it will provide another place to add value to the farmer who will benefit from quality seed

Q2FY21 concall- 24/11/2020

-

470cr generated in H1. Too large sum, request for buyback from BNP Paribas MF and another caller. “We are very cautious- should be secure and give good returns. Issue is in front of the board”

-

Indonesia JV: Thai union project where we have small investment

-

Fish feed? Can PLI scheme help? Time is not right to take a final decision. We have everything in terms of technology. Due to COVID, the situation is not good. PLI doesnt appear to be very lucrative. More details have to come on production, infrastructure. There are so many industries in the scheme. We have to see how govt frames it, nothing is clear as of now.

-

-

25-30% fall is anticipated globally. India 20-25% reduction in FY21. White spot disease on and off. Farm gate encouraging. Last year production was was 8 lakh tons, 6-6.5lakh tons production expected. Farmers have undertaken stocking. Harvest will be in January. Expecting same level of sales. Adding new farmers, geographies. Market share to be 46-48%.

-

We are getting farmers to shift from competitors to Avanti.

-

We maintained our revenues in H1 when industry is expected to be down 20-25%. How is this possible? Feed quality, performance, constant support to farmers. Profitability depends on RM and productivity, where we have been able to maintain the performance. For processing- we are focusing on value added products for right customer and right market. Q2 many new contract shipments started for US. Increasing CU. Maintaining quality and our relations with customers. Less prone to fluctuations because we are able to get regular orders from these customers.

-

There is a lot of potential for the industry which is not realised due to these temporary issue. We hope that in 2021 there would be a complete change in the performance and we expect to see good growth.

-

-

Govt support expected to revive the sector

-

Govt has capped MEIS to 2 cr for Sept to Dec. It will be discontinued from Jan. New plan RODTP details have not come. Q2FY21 MEIS was 10 cr, duty drawback was 6cr. Last year total MEIS+duty drawback was 21cr. Q3 will be 2cr?

-

PLI scheme for food processing includes fisheries. Competition saying there is potential for fish culture in Punjab and Haryana due to water bodies. We have to see the roll out of scheme for farmers, sply in Andhra, Bengal, Gujrat that are already doing good fish culture.

-

-

Feed

-

RM prices is major variable: Overall RM cost will remain more or less same as last year 1) fish feed stable, good catches and currently at rs 89 down from 91rs. expect it to be below 90. 2) Soya crop was good so expected price drop but US crop failure, GMO seed is not available so demand for Indian crop has gone up. Demand for non-GMO is also pushing prices. Soya was expected to be 41 but is at 43-45rs. 3) Wheat flour is stable.

-

Selling price- Dont see any change up or down.

-

Is there a stress in competitors? Stress in sense that competition giving credit to dealers and farmers. There could be issue in recovering the money and it becomes a vicious cycle for next crop. Other players reduced prices, gave credit but Avanti does not forsee challenge from competition in any factor- pricing, quality etc. Complete control of situation

-

Next season outlook? Last season was an early harvest. Farmers are looking for good season of first crop, starting Feb-March. Farmgate prices are good.

-

-

Processing:

-

Margin outlook? 16% margin is one of the highest. Can this sustain or any impact due to MEIS? It may not be 16% but it will be good margins.

-

RM and export prices. Recently, RM has been going up faster than export price and there is little shortage, but crop will come in Jan and RM will drop. Dynamic demand and supply situation.

-

Market size for value add products and Avanti’s share? India is still commodity supplier which does large volumes to US, EU, China. Vietnam and Thailand are much advanced products which are not introduced in India. We want to introduce these and export from India. Avanti share is small, low double digits.

-

Volumes- 13400 tons last year. H1 volume is down 10% but realizations have gone up. For full year FY21 we expect slightly lower volumes but we will do more of value add.

-

Capacity Expansion- nothing coming up, but we want to increase CU. Processing is labour intensive and COVID had caused some labour shortage. Now the labout issue is sorted.

-

-

US - Thanksgiving and new year demand? Orders already shipped? Cases going up again. Cant predict.

-

Ecuador exporting more to US. Is India losing market share? They are shipping more than before but qty is low. Main reason is dumping in US due to ban of certain Ecuador factories in China. Ecuador is supplying low value add shrimp. Ecuador shrimp prices are at all time low, so we need to see how it evolves. Ecuador shrimp is more suited for China so when China starts again, they will supply to China instead of US.

-

China- Q2 we didnt export much because we exported in Q1. Look at H1 data. Overall, China is importing lower qty of shrimp, driven by policy of Chinese govt.

-

Is channel inventory at lows and best WC days are behind us? We keep RM inventory for 1-2 months depending on season of fish meal. We dont see much changes in either units.Our realizations are prompt and we pay promptly. We have comfortable funds situation so not going for bank borrowings.

-

Hatchery started 400mn seed per annum. 50% CU in first crop, revenue 7cr. (Now after the last post by @samm2211, I am not sure whether they said 50 or 15. Personally I am not bothered about this part much…very small in overall scheme of things)

20 Likes

Interesting story on the Ken on Indonesian startup efishery and their automated feeders. Wonder if such a solution will be required by Indian fish farms. Maybe the management could explore

5 Likes

Good article highlighting the farmer pro policies adopted by the company during distress/panic times - https://www.businesstoday.in/magazine/indias-best-ceos/the-caretaker/story/425912.html which leads to trust and long term business leadership

18 Likes

4 Likes

HI Team

Just founded the below Link and does not sound good for avanti.

3 Likes

Can you explain how this does not sound good for Avanti?

1 Like

Hi Team

The shift in technology and the possible customer shift(from Indian Farmers to this Company) . It is just a thought cant access the impact.

Regards

Shashank