As of now, the near term impact might be positive for indian processors as countries might source more due to stopping of procurement from those eucador companies. But things are too dynamic. Tomorrow one case emerges from India and we will be worrying the same for Indian companies. Broadly if the company delivers what they have mentioned in the call, i feel it be great.

3 Likes

Adding my notes from company concall as well, as it may add up few more points.

Forecast - shrimp demand in india less by 10-15% in current FY. But Avanti sales will not be affected much.

Extra cash on books

- company is evaluating various options but not close to any of them to finalize yet.

- Safety of capital is much more important than return of capital. Hence company is evaluating options keenly

- current investments in mutual funds etc for extra cash is generating returns like 7% post taxes

- Sounds like management is considering diversification into non-related business as well. Thats my guess from whats told and not something specifically told.

expansion in shrimp processing business -

- Margins are good and company is executing on lines of plan from 2017. US business is doing good

- capacity utilization for existing set up might have reached to 95% in couple of years in non-covid scenario. But due to covid their is uncertainty now

- Planning to add new capacity as needed but not given clear numbers

- Automation will be considered and is being evaluated by the company to deleverage labour intensity

China Vs US business -

- Chinese exports are more into commodity like products whereas US is more of value add products. No apple to apple comparison possible

- Not thinking of launching own brand in US in near future. Establishing brand with competition to existing brands in US is very tough process

- retail demand in US is making up for revenues in spite of loss of business for restaurants etc. Its more of a staple food now.

- Chinese exports can go on increasing but depends upon china’s import policies.

Covid impact on demand -

- India demand affected by 20% in first 6 months - Jan to Jun 2020. Overall impact for calendar year assumed to be -10% as pick up is expected from Jul to Dec.

- Avanti feeds business will not be impacted much though due to copamny increasing farmer base and existing relations with current farmers.

- US demand - no clear picture was given. But mentioned that as portien food its much sought after product and not getting much impacted. Restaurant closures and lock down uncertainties in certain states like California are the factors which stop from predicting future. But more or less demand remains unaffected much.

- on global demand side, global demand seen increasing on lines of expectation more or less and there is not much impact.

Hatcheries business -

- likely to start in couple of months time.

Farmer scenario -

- there was no stocking in summer by farmers due to Covid uncertainties. Situation coming to normal from Jun and see pick up in demand

- farmers are now confident and starting back harvesting season.

Extra inventory and RM prices -

- more inventory on books in last quarter is due to stocking of items like wheat. Normally wheat crop comes into Feb in market. Company stocks 2 to 3 month requirement in Feb which gets subsequently used in following 2 to 3 motnhs.

- Company’s mixture of raw fish, Soyabean etc are different and we procure different qualities and grades. hence RM prices dont exactly match as what is seen on websites.

Export Incentives -

- Earlier export incentive of 7% and duty rollback of 2% adding upto 9%. Now export incentive is 5% and duty rollback is 3% so adding up total of 8%. Company need to bear this.

Ecuador case in China of Virus detected on imported packets -

- No impact seen on US exports by company as their is very less posssibility of virus in forzen food

- Boxes remain in trasit for upto 14 days and hence less possibility of virus sustaining so much period

- China may take specific import decisions. But do not see impact much on company business

12 Likes

@mskoti86 , yes I agree with your message but this is case with all types of farming .

Looks like similar story for month of June. Shrimp imports in US from India dropped from 20,559 to 11821. All other countries Equador, Vietnam, Indonesia have gained at India’s expense. Hoping that this situation will change in month of July considering economy was unlocked by then.

https://www.st.nmfs.noaa.gov/apex/f?p=169:2:::NO:::

Although positive way to look at this is increase from 8600 to 11821 on month to month basis

7 Likes

Good to read the latest annual report - https://www.dropbox.com/s/x81vd8d7ag9wqct/Avanti%20Feeds%20AR%2020.pdf?dl=0

Clearly communicates the leadership that the company has achieved. One of the rare few case where the company has grown rapidly in a span of just 10 years and yet the company has generated loads of cash.

Future growth won’t be easy as they already have a high market share in feed segment which is already 70%+ of the total turnover. Probably the processing division will be the growth driver.

I hope they improve the dividend payout ratio to the likes of major FMCG cos.

Near term could well be subdued.

Ayush

Disc: Invested in family and client acs.

27 Likes

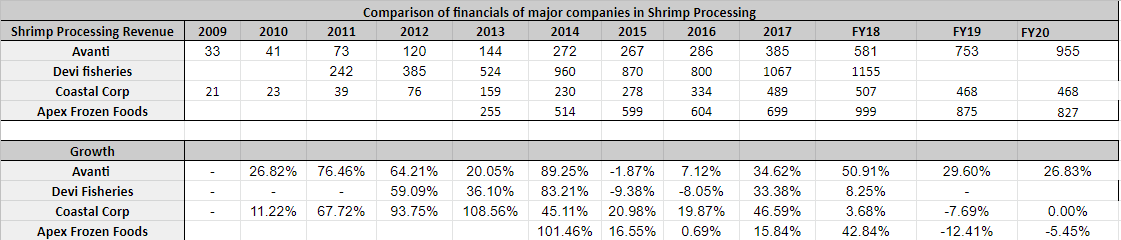

I was doing a comparative analysis of Shrimp processing business of Avanti vs peers and interestingly the company has grown at about 30%+ each for last 4 years and specially last 2 years when none of peers could grow much and the industry had headwinds in 2019 and 2020.

28 Likes

Everything looks good for the company except promoter holding. I wonder why promoter never thought of increasing his shareholding in such a growing profitable company, even when share price dropped earlier this year as well as last year. Or else Company can declare buyback and promoters can raise stake by not participating in the buyback. That would be much better use of money sitting idle in the books. Is it a reason that he is not interested in increasing dividend in-spite of huge reserves since he would get only 43.69% of it.

Maybe there are other reasons for not increasing the shareholding and not giving higher dividend but I am just trying to connect dots here. Its better to be skeptical than sorry…

Disclosure - in watchlist

3 Likes

Thai Union, their Thailand partner holds 22% if I remember correctly.

2 Likes

Due to competition from other players and downtrend in shrimp cultivation, both CP feeds and Avanti feeds are reducing Feed prices by Rs.3/kg. In earlier months of the year they increased price by Rs.5/kg

6 Likes

Hello.

What is the source of this information-

Do share the source. Following was shared in last concall

1 Like

Strong Q1 results by Avanti despite lockdown and slowdown of shrimp culture during April/May. Softening of raw material prices helped

5 Likes

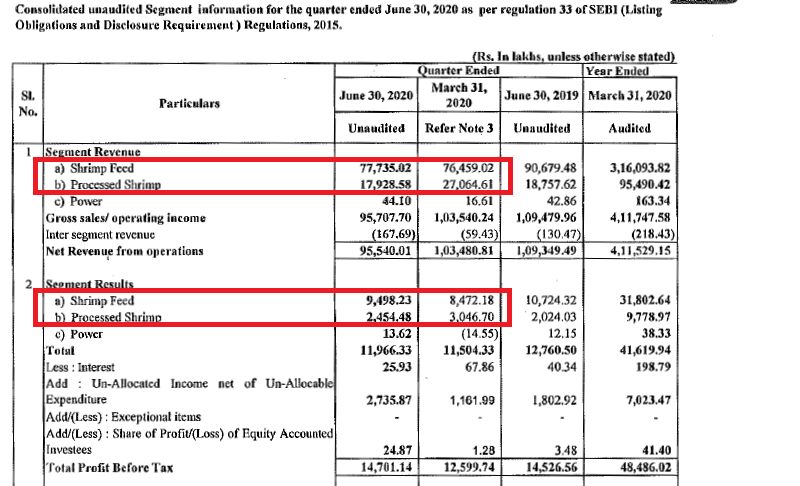

Some interesting nuggets from the segment data.

Despite large disruptions due to lockdown, lack of imported broodstock in April and May and consequent impact on farm activity, revenue from Feed business is surprisingly positive QoQ, up marginally by 1.67%. Sequential PBT figure does even better, up by whopping 12.1% QoQ! Margins have improved significantly, so the price hike done late last fiscal seems to be playing out positively (despite the minor rollback in price hike to help the farmers in these stressed times).

Similarly, they have done a stellar job with the Processed shrimp segment. Revenue falls off the covid cliff, from 270.6 Cr in Q4 FY20 to 179.28 Cr in Q1 FY21, down by whopping 33%. Now, despite this vertical drop in sales, pre-tax profit barely dropped by 19%, falling from 30.46 Cr in Q4 FY20 to 24.54 Cr in Q1 FY21. Once again they’ve manage to boost the margins significantly. And this despite significant softening in International shrimp prices from about $14/Kg in March to $12.55/Kg in May and $12.13 in June 2020.

As @ayushmit pointed out in his recent post, they are the only ones to grow the processed shrimp business at 30% for last few years, even when facing headwinds and with probability of reaching a market share saturation in feeds, processing segment has to be the new growth engine. If Q1 performance is any indication of their ability to deliver, it truly bodes well for the business.

Resolute performance in tough times indeed!

Disc: Invested for long term

18 Likes

Yes, results look good especially when we compare it with the performance of peers. Very rarely we will see a leader despite having large market share, continue to do better than others. And this becomes more valuable as the business is something which is like daily consumable for the farmer (think FMCG) and throws out cash.

Look forward to hearing to the management. There would surely be concerns around price reduction. But looking at past, it maybe ok and perhaps based on input cost reduction.

10 Likes

Isn’t Bottom line is boosted cos of tax rate at 22% as against 30% ?

1 Like

Shrimp imports in US from India are at 24,125 in July-20 compared to 25,309 in July-19. Almost similar. Really good progress compared to previous months although it was expected. Other countries like Equador, Indonesia and Thailand continued significant growth.

2 Likes

The govt of India has been focusing on fisheries and a lot of money is being made across the value chain. May not have an immediate effect but bodes well for medium to long term fortune of fisheries.

3 Likes

I think this is a great news for Avanti feeds!

1 Like