Majesco Limited

About the Company:

Business:

Majesco (formerly MajescoMastek) is a provider of Insurance Technology Software, Information Technology Services and consulting to insurance carriers worldwide across lines of business – Property & Casualty (General Insurance), Life, Annuity, Health, Pensions, And Group & Worksite Benefits Insurance.

Timeline:

1992: Founded as MajescoMastek, a U.S. Subsidiary of Global technology solutions provider, Mastek.

2005: Acquired Entegram LLC, a Connecticut based software company.

2007: Acquired Vector Insurance Services, a technology solutions provider and third party administrator. (L&A)

2008: System Task Group (STG), an IP based enterprise solution provider, was acquired. (P&C)

2010: SEG Software, Canada based policy administration systems provider was acquired.

2015: Acquired Agile Technologies, a consulting firm.

2015: Demerger from Mastek.

2015: Listing on NYSE.

2015: Merger with Cover-All Technologies.

Overview:

Majesco, as an Insurance technology solutions provider, has thrived its way to be in top 3 companies in core systems, data, distribution, digital and cloud offerings, where in cloud based services it enjoys monopolistic position. With the successful integration of Agile and Cover All, the company has ended fiscal year 2016 achieving its goal of market penetration with strengthened brand, new clients and order book growth.

Opportunities:

* The Insurance Technology market is a large and growing market with over 11,000 insurers globally and with large number of US insurer still using dated platforms, the market is huge.

- With around $25 billion of addressable market in new hardware and software, maintenance and support and external service and staffing, P&C and L&A offers significant opportunity.

- 58% of the insurers IT budget is increasing with 80% of IT budget apportioned to core, data and digital.

- In US, more than 25% of insurers are replacing core systems, more than 25% planning major enhancements and more than 25% are going for total replacement and enhancement. (Source: www.novartica.com)

- Acquisitions has helped boost revenue through cross selling. No competitor has an all-round solution comprising consulting service, core software suite, digital assets and data service under single roof.

- With the Insurance business environment radically shifting and around 48% of the Insurers increasing their investment in cloud services, Majesco is already in a unique positon to serve with its core software, digital and data extensions and scalable cloud platform.

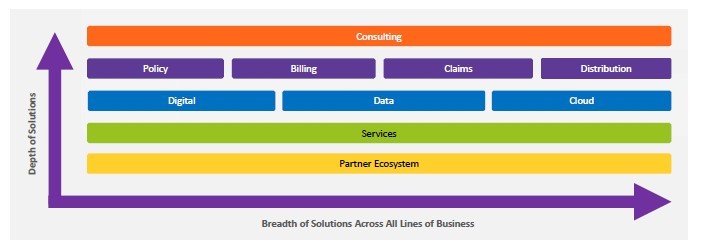

Majesco value Chain:

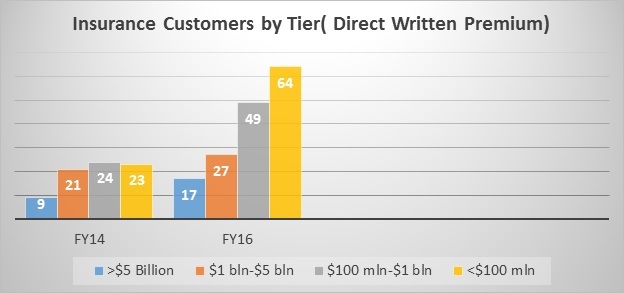

Client Profile:

Risk & Concerns:

-

Client Concentration: Revenue contribution from top 5 and top 10 clients has reduced however the % share of revenue from Top Clients is still a concern

-

High R&D/S&M : R&D expenditure remains the key driver for margin expansion. As of now, rise in R&D and S&M spends remain a key risk to value and sustainable earnings is the necessary trigger.

Investment Rationale:

Majesco, the spin-off of Mastek Ltd. has registered its presence in cloud based P&C and L&A insurance industry platform offers tremendous demand for modern core systems. Very few or no competitor offer support for both group and individual business. Insurance industry being a $4.6 trillion market, is only second after media and entertainment to face major disruption.

Majesco has its presence in 6 countries with 2500+ staffs and has done successful acquisitions in last 10 years with an investment of $100 million. The company with over 164 clients globally has registered growth of 23% CAGR in last 2 years and expects to reach revenue of $200-225 million in next two years.

• Order book of $158 million in FY16

• Ended FY16 with 12 months backlog of $73.1 million, up by 46%

• Revenue up from $79.3 million in FY15 to $113.3 million in FY16

• Rise in Gross margin from 38.5% to 44.5%

• Increased spending on R&D and S&M, 29.5% of the revenue

• Revenue from new account up from 9.8% of the total revenue in FY15 to 14.0% in FY16

• Revenue guidance of $200-225 million by FY18 with EBITDA at 12-14%

At CMP of Rs. 566, Majesco is trading at EV/Sales of 2.08 its FY16 revenue and 1.18 and 1.05 its FY17E and FY18E respectively, which is steeply undervalued compared to its global peers Guidewire Software and Sapiens(less profitable company) trading at 9.19x and 2.67x respectively. Majesco is positioned to gain market share with increasing scalability and higher revenue growth and profitability due to huge cross selling opportunity in P&C and L&C cloud business.

Disclosure: Not Invested.