Hello,

What do you think about their CNG vehicles. I think they might be a key factor under bs-vi regime as smaller diesel engines may become unviable and CNG availability improves.

Thanks

Hello,

What do you think about their CNG vehicles. I think they might be a key factor under bs-vi regime as smaller diesel engines may become unviable and CNG availability improves.

Thanks

Mahindra and Mahindra to shift focus to electric 3-wheelers Mahindra and Mahindra to shift focus to electric 3-wheelers | Mint

Article quotes internal sales targets of 10000 electric 3 wheelers a month ![]()

![]()

I believe mahindra (and others) focussing on electric three wheelers might actually benefit atul auto if they get out of electric three wheelers and focus on CNG since they anyways don’t have enough resources for r&d on electric. I am sceptical about success of electric three wheelers in India(they seem to be empty or at max carrying 2 passengers and are slower than diesel or gas based vehicles).

Also, focus seems to be the strong point of small companies and those small companies that lose focus have an even higher rate of failure.

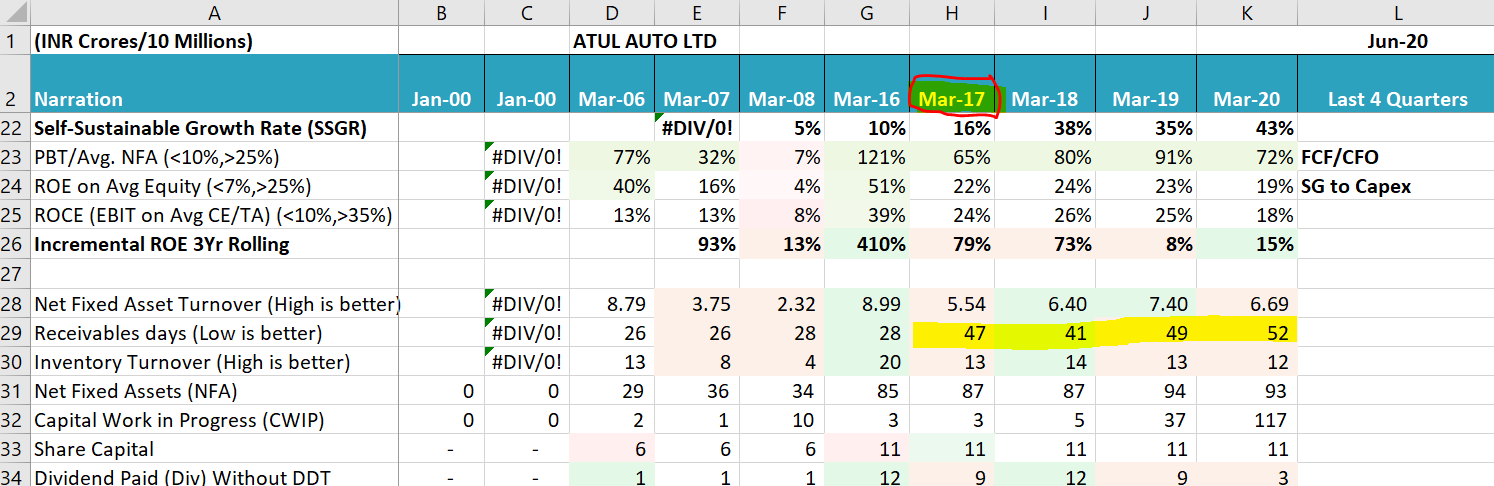

Atul definitely has the full vehicle suite. However, they are having problems in terms of market share which they are losing to Bajaj (specially in the cargo segment where their market share went upto 20% in FY16 and is now down to 15%). In the passengers segment, they have quite a low market share anyway (~3%) and are unable to dent Bajaj’s dominance. That’s probably why they are focusing more on exports right now.

The domestic 3-wheeler industry is close to 6 lacs vehicle, 10’000/month translates to 1.2 lacs (20% market share). Mahindra currently has 2-3% market share and they are not a new entrant. I will say odds are not in their favor (but who knows what can happen!).

In essence, Atul is losing market share which is probably discounted in the current price.

Nirmal Bang (interview)

does anyone know BS6 selling prices of Atul Auto & competitors?

Thanks for the information. Very helpful

This is grt deep dive analysis.

The beauty of this company, they believe in growth through internal accurals and it is consistent business

CNBC interview (link):

This is interesting development :

My only concern is companies abilities to deliver outside their home state.

Disc : Invested in my core portfolio.

CNBC interview (link):

When an Independent director is hired by Atul Auto :

Though the profile of Vijay Goel looks grt, am not sure, if the recent spurt in prices is of this reason. If that is the case, then looks promising.

Disc : Invested in core portfolio.

Hi Investors ,

does any one has link to conference call held on sept 15th 2020…

incase some has chance to attend it , can you share your thoughts

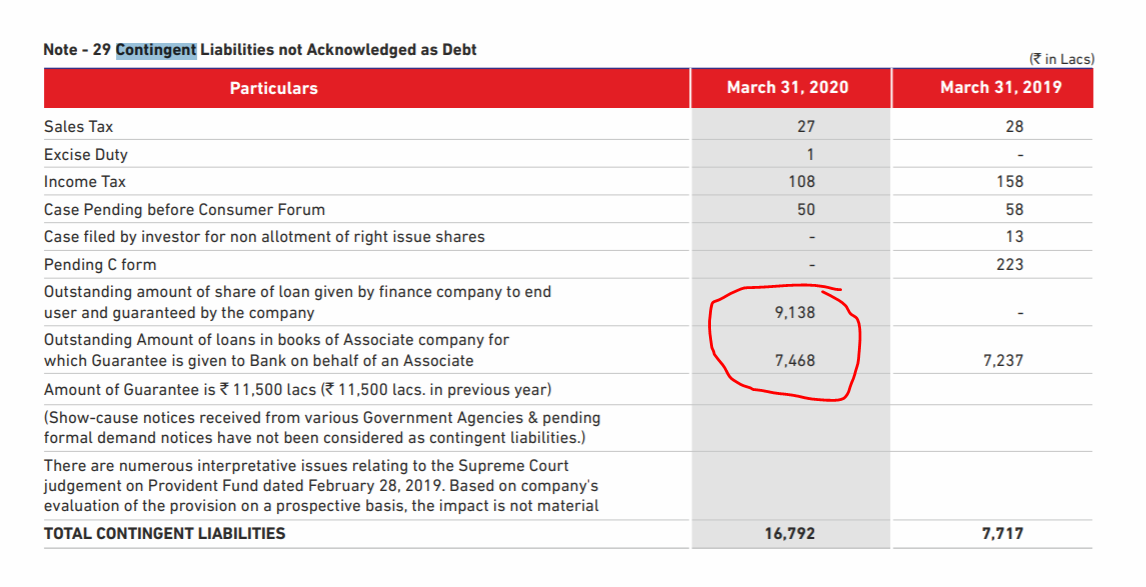

Company now acquired the rest 70% of stake in Khusbu auto finance (@44.57cr. valuing them at 63.67cr.) making them a wholly owned subsidiary. Cost is equivalent to the book value of Khusbu, I have no idea about the quality of their underwriting.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/22d9376f-12ad-4edd-b9f1-fedbb0b16e79.pdf

I am not sure about there Underwriting … but i don’t see much of difference if it is associate with 30% stake or completely owned company because the complete AUM is backed by corporate guarantee extended by Atul Auto Ltd.

with such a risk on there books … not sure why they are sharing the profits with dr vijay kedia of kedia securities

Underwriting :: as per the report gross NPA’s stands at 11.73% on Mar 2020 vs 7.08% on Mar 2019

How the acquisition could impact the debt

Sep 2021 Debt on consolidated level → 15cr + 44.57cr + the complete debt of Khushbu Auto Finance Limited

this would mean more stress on the financial which is already impacted by COVID-19

Regards,

Rama

Increase in receivables and investment in Khushbu Auto Finance Limited happened almost at the same time … just wondering if Receivables has something to do with this Auto Finance company , I did not get(/might have missed ) any receivable details of Khushbu Auto Finance Limited in AR …

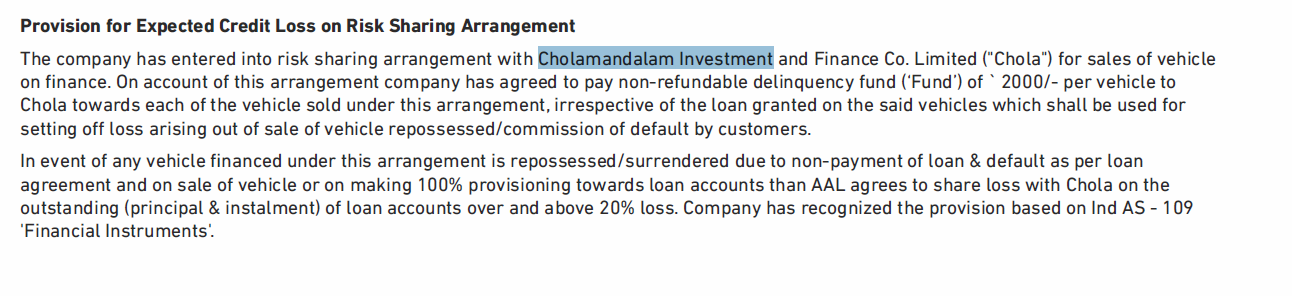

Corporate Guarantee to cholamandalam investment company …9,138

Yes the Sales and topline has grown well but with much risk on the books for the company …

with Above I fell the growth of the sales does has considerable amount of company Push base rather then market Pull base

*** Note this are just my personal view’s based on my reading , this can be wrong ****

Credit is heart of sales for vehicle market as without credit even second hand vehicle market will collapse,

we need to find out what kind of arrangements other auto companies have with NBFC’s.

Is Atul Auto sharing more risk with NBFC’s compared to others?

Need to find out

Is acquisition of KAFL in favor of business of AAL and in the best interest of investors?

I think 60-70% of customers cant do without credit, so credit is must for this business.

AAL already owns 30% shares and acquiring remaining 70% shares at 44.5cr.

It is acquiring in depressed market conditions for NBFC’s & particularly KAFL’s customers are affected more, as in lockdowns they had almost zero cash flow, so I expect them to acquire at significant discount to fair value, as NPA’s are definitely going to be very high in coming quarters.

Need expert opinion on acquiring valuations of 44.5cr for 70%

Will 3 Wheeler business grow?

I think it will.

Reasons,

a) India’s GDP is bound to bounce back to 6-7-8% growth level

b) Rural to Urban population shift theme playing out, cities will get bigger and more populated, so last mile connectivity for material & passenger traffic will increase.

Will AAL’s business grow?

Time frame is uncertain but I think it will,

a) It’s making good quality of vehicles

b) Market leader in Gujarat and it just has to apply same strategy to other states. Hugh growth runway

c) Prime competitor in cargo segment is Piaggio which has to feed financially weak Italian parent, so Piaggio cant stand to win in price war.

d) Good export potential

e) Growing market size

f) Presence in all fuel types

g) Focused management

Why so low price to such high RoCE, strong Balance sheet, good growing business?

Business is depressed, credit risk is there, acquisition risk is there, and definitely there is uncertainty.

Market hates all these

When will the sun shine again?

We don’t know,

3 wheelers segment is one of the most impacted segment in last 6 months due to COVID & Lockdowns,

I guess bad NPA’s cycle is playing out since last 2-3 years and it may be at its peak at the moment, so whatever bad had to happen has happened now.

once the uncertainty is over and GDP starts growing again at heathy pace we can expect a good business, and great share price.

Discl.: Invested and may be biased ( Some famous western investor has said " Keep your eyes wide open when choosing a girl for marriage and half close after marriage)

An intrsting thing I got on my LinkedIn page.

Though I could not get the link to the page. So took a screen shot.

Though am not sure how this product would add in the revenue / margin part of Atul Auto.

But in totality looks like a +ve step.

Disc : Invested.

The passenger 3 wheeler sales has not yet normalized.Even that is reflecting on the monthly sales figure.

seems like colleges and schools being shut is the drag for it. Going forward things should improve. Stock has not run up more from march lows compared to other auto stocks.

Thanks,

Deb

During FY20, overall automobile industry faced challenges due to various factors such as increased insurance costs,curtailed lending by the NBFC segment, weak festival demand, weak consumer sentiments, migration to BS-VI norms and the spread of Covid-19 in the country by end of the year.

Auto industry usually pushes more vehicles in the market in the last month of every financial year. However, due to nationwide lockdown from

March 24, 2020, company could not do so this time— both domestically and globally. Hence, overall sales volume declined by 12% during FY20 to 44,082 units. Also, export volume declined by 39% during FY20 over FY19. Due to

imposition of nationwide lockdown, company had shut its manufacturing facilities from March 24, 2020 till May 2020 due to which company could sell only 1,477 units during Q1FY21 as against 10,514 units in Q1FY20. Hence, TOI of the

company for Q1FY21 moderated by 82% on Y-o-Y basis to 26.87 crore and it also incurred cash losses during the quarter.

Subsequently, there has been some growth in sales volume, however, the same are still on the lower side.