A variety of factors, but IMHO primarily low base. Also, it was easy to grow in Gujarat where Atul is a well known brand. But not so outside. Please read this:

Anyone planning to attend the AGM scheduled for 30th September ?

Rajkot made e-rickshaw approved by UK: Another milestone for the ‘Chhakda’ maker Atul Auto.

https://t.co/IR6Js9N1ar

If anyone is attending the AGM, request you to investigate about the following questions:

-

What is the distribution network of the company? What are the plans on expanding it? (Am I the only one who couldn’t find the dealer / distribution network numbers of the company in AR FY19?)

-

Bajaj Auto’s 3W margins are 20% (Source: Q2FY19 Conf Call). But Atul’s EBITDA margins are only of the order of 13%. What is the cause for this difference?

-

How is the transition towards BS VI going on? Are you facing any hurdles which are difficult to handle?

-

What is the contribution of diesel vehicles in total sales? Is it easy to convert diesel engines to BS VI?

Thanks!

Discl: Invested from higher levels.

1 Like

Hi,

Can someone please explain this

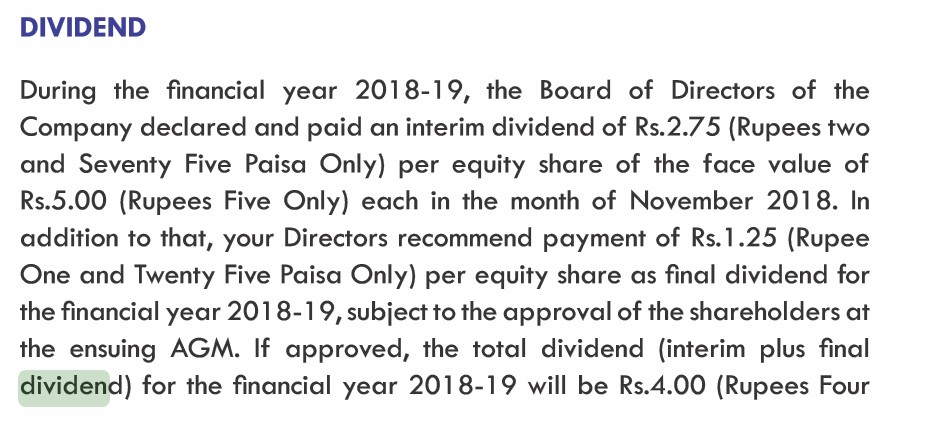

Total dividend for year 4Rs per share

No of shares = 21943200

So total dividend outgo should have been 4*21943200 = 8.77Cr

But in cashflow it is mentioned as 11.52Cr pre tax

Final dividend of Rs.1.25 per share will be paid in FY19-20 and will not appear in Cash Flow Statement. What appears in the Cash Flow Statement is interim dividend of Rs.2.75 per share and final dividend of Rs.2.50 per share belonging to FY17-18 paid in FY18-19. So the calculation is as under:

| Particulars (Rs. Crores) | Dividend | Total outflow |

|---|---|---|

| Final dividend for FY17-18 paid in FY18-19 @ Rs.2.50 per share | 5.48 | |

| Dividend Distribution Tax | 1.12 | 6.60 |

| Interim Dividend for FY18-19 @ Rs.2.75 per share | 6.03 | |

| Dividend Distribution Tax | 1.24 | 7.28 |

| Total | 13.88 |

4 Likes

If anybody attended the AGM, would be great if you could upload the notes.

Thanks

I want to know the current condition of this company

Valuation wise its looks good.

Any idea regarding its future growth.

Currently debt free and many mutual funds are invested.

Can any one throw some light on the future of this company

1 Like

The stock is trading at a PE of 5.3 right now with no debt.Production capacities has expanded from 60,000 vehicles to 1,20,000 vehicles.The company seems to be doing well in terms of expansion.

Anyone else is following the stock?

1 Like

Production is there how about the demand and sales. I have been tracking but scared to take a position.

Hi,

Yes I have similar worry.they do have some kind of exports to Europe and we all know what is the situation now in Europe.This Covid 19 has really thrown life and business out of gear.

Disclosure invested in Atul auto

Thanks,

Deb

Looks like demand has fallen off the cliff. The current quarter results are going to look bad:

Why have the sales fallen so badly?There was no lockdown in feb.Can someone explain?

1. As Atul Auto is not a market leader, is its growth sustainable?

In Passenger 3 wheeler segment Bajaj Auto is market leader and it is very difficult to gain market share from Bajaj Auto.

In Cargo segment Piaggio Vehicles Pvt ltd is market leader whose Parent company is Italian Piaggio group(Piaggio & C SpA).

Piaggio Vehicles Pvt Ltd is in good financial shape, due to healthy profit margins, low gearing of around 0.5times, & it has own engine manufacturing facility.( Annual revenue around 3500cr & NPM of around 250cr)

Financial condition of Parent Piaggio & C SpA is not very good and also Parent company is having diversified product portfolio, so not particularly focused on any single segment(though more focused on 2 wheeler segment worldwide).

As parent is not in a very good shape,as a good boy Piaagio Vehicles pvt ltd sends parent a huge dividend every year

Credit rating agencies are downgrading parent since long time.

here are some of highlights of parent Piaggio & C SpA

- OPM on consolidated basis is 6% & NPM is 3%

- D/E is more than 1

- Company has around 28% revenues from India market

Some highlights on Piaggio Vehicles Pvt ltd.(Indian subsidiary)

- Ape Fy18 2,04,700 & Fy19 2,06,700 sales volume

- Overall Three wheeler Market share increased from 23.3% to 23.9%

- Cargo segment market share decreased from 44.9% to 41.8%( I think Atul is eating it)

- Passenger segment increased from 18.7% to 20%

- First to become BS VI on three wheeler segment

- The updated cargo range features a larger cabin, while the passenger version has been fitted with new doors designed for even greater passenger safety.

- alternative fuel models are equipped with one of the most advanced transmission systems in the sector, and feature an ultra hi-tech 3-valve, 230 cc engine

- Reduced employees from 2026 FY18 to 1749 Fy19

- OPM in India business is 15% & PAT of 8-9% (Atul Auto has higher operating efficiency as OPM 13% & NPM 8%)

Overall Piaggio India business is gaining market share in Passenger 3 wheeler segment but at the same time not able to defend market share in Cargo segment.

130 years old Italian man is now dependent on his son’s ( Indian & asian subsidiaries) to support him in the old age, otherwise he will collapse(COVID 19 will further deteriorate balance sheet), still I felt looking at the Annual report of father company it seems to be more focused on European business and consider Indian business as a cash cow.

So clearly along with a market growth Atul Auto has potential to increase market share in Cargo business, and it is also growing exports.

2. Why Atul Auto can increase market share, whats special in it?

- Atul Auto is focused singularly in only one product segment ( 3 Wheelers)

- It is not doing business simply by copying product designs from market leaders

- They know how to position product

- Customized product development as per customers requirement.

- As they can become market leaders in one state, they can also use same strategy in other states.

- Balance sheet is in very good shape, internal accruals are good.

This is how they positioned their vehicle in the market as against competition (Atul Shakti vs Piaggio Ape),

Kept BHP less

Kept torque less

Reduced width and increased length

Increased height and Payload capacity

Mileage is around the same

Keeping BHP & torque less gave them advantage of giving same mileage for significantly higher payloads than Ape, Reduced width give driver freedom to enter crowded lanes in typical small width road Indian cities. Also less torque & pickup speed means less accidents in crowded parts. Increased height means more boxes/material can be stacked.

As you can see in image, driver door is missing and it has more height giving comfort to driver where he has to visit retailer’s shops every now and then to deliver material. (Very much suitable for FMCG dealers)

they are not making just another three wheeler, they are creating value & comfort for end user.

This product may be produced keeping in mind requirement of FMCG dealers/distributors. I Think this is an edge company have(Product Positioning).

Price of the product is around same as Piaggio Ape, so good thing is they are able to sell and increase market share without competing in Price alone.

another advantage is as company claims, Atul rickshaws as low operating maintenance cost, this is another edge.

As Piaggio Vehicles Pvt ltd has to feed its poor parent, they tend to loose in case of price war.

Atul Auto Negatives :

- No in-house engine manufacturing

- AR15 says Ahmadabad green field expansion project will compete soon, investor’s must have considered their soon as 12-18 months, but project is not yet operational.(Project may be delayed considering reduction in growth in FY16 & 17, till date they have not reached full capacity of Rajkot plant)

Conclusion : I think they were able to grow fast in the past & they will continue to do so in the future ( but not immediate future ![]() ).

).

Growth will come from -

- Market itself is growing

- Exports

- Snatching market share from others in Cargo segment.

This is my understanding & I may be wrong,

suggestions welcome.

Disclosure : Invested

Pardon me for bad English.

12 Likes

The trade payables and receivables are red flags before investing. Trade receivables has increased from 47 Cr to 104 Cr in last 3 years. Trade payables has gone up to 63 Cr. With Atul auto being debt free, this increase in payables is not digestible as they can payoff. Also the collection of receivables is suffering and ttl Rx is now 2 times of npm. Why is the company not able to collect it’s receivables? There is not much explanation in AR of this. Also in last AR co. Said that they have taken insurance against credit risk. seems to me that they are going to write-off a big part of Rx in coming years and may do so gradually.

4 Likes

My observations from the last 10 years of annual reports are below:

- The FY10-16 growth was on back of launch of rear engine based 3-wheelers which got a lot of success.

- One of the key shortcomings was a petrol/CNG based vehicle in their arsenal. The management guided for a launch of petrol/CNG vehicle in FY15 annual report and launched the same in FY16

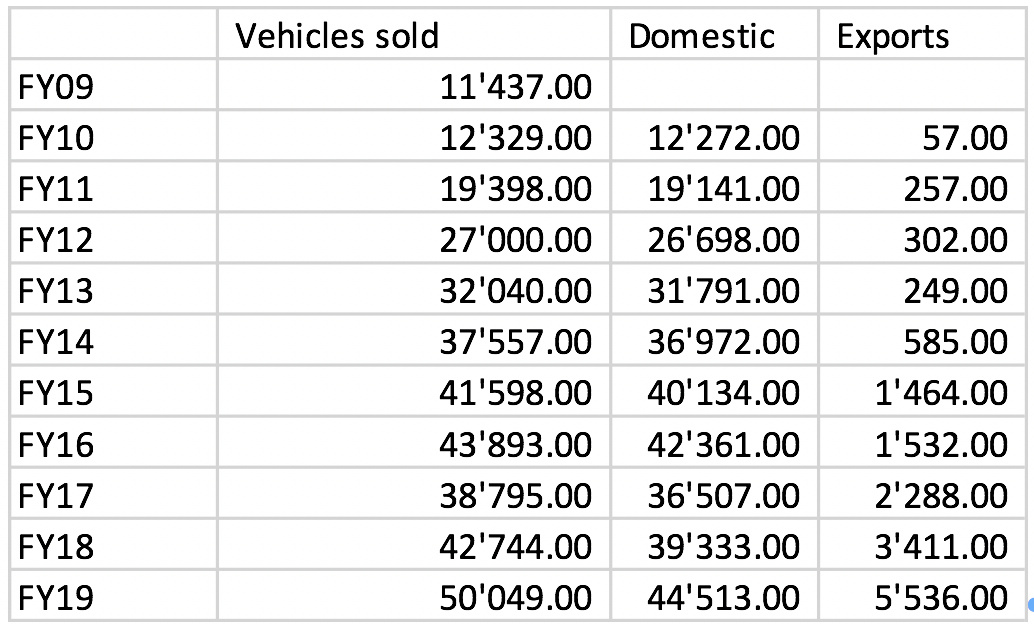

- From FY16, domestic demand has plateaued. However, their export growth is admirable (albeit at a smaller base): See chart below:

- Sale of their domestic 3-wheeler crossed the previous FY16 peak in FY19 (business is cyclical, its okay that growth is not linear)

- The Ahmedabad CAPEX to increase vehicle capacity from 60’000 to 120’000 was first proposed in FY15. However, the work has finally started in FY20 as they sold close to 50’000 vehicles in FY19 (reaching optimum capacity utilization).

- Their 3-wheeler electric rikshaw has faced stiff competition from Chinese imports (sales: 141, 922, 610 in FY17, FY18, FY19).

Key red flags:

- Increased investment and corporate guarantees given to its associate (30% holding) Khusbu Auto Finance Ltd.

- FY17: Provided 50 cr. of corporate guarantee + invested 6.82 cr.

- FY18: Provided 150 cr. of corporate guarantee + Invested 5.4 cr. + Invested 5 lacs to get into housing finance business through Sanand Home Finance which is yet to get license from NHB (this is stupid capital allocation!). Why venture into housing finance?

- Increased receivables means that they need to give easier credit terms (which is okay as long as there is no large credit loss)

In my opinion, market took the valuation of a cyclical business to an extreme (at peak it was valued at 40 times earnings and >10 times book which is absurd!). Now, its again back to close to its book value (which in my opinion is again absurd!). For a business generating ROE > 25%, P/B > 1. Please let me know if I missed something ![]()

Disclosure: not invested

8 Likes