Update on this

The GCC division to be sold to alpha GCC for EV of 13,540 Cr , Alpha GCC will have 35% ownership by promotors & rest by consortium of PE firms.

Concal scheduled at 11:30Am today : Webinar Registration - Zoom

Find more details in PPT

Update on this

The GCC division to be sold to alpha GCC for EV of 13,540 Cr , Alpha GCC will have 35% ownership by promotors & rest by consortium of PE firms.

Concal scheduled at 11:30Am today : Webinar Registration - Zoom

Find more details in PPT

Correct me if I’m wrong team….

All said and done if Aster GCC business gets sold - that basically means we lose our cash cow

Yes we’d receive cash in exchange, but the cash would not justify the current valuations.

Aster would have deploy this cash and then build up the same level of operations it had back in GCC and the chances of that to happen is very unlikely.

GCC business was very much a monopoly because of few hospitals and very high insurance penetration. In India you have significant competition with low insurance penetration.

Hence this deal is really unfavourable to retail investors.

Let me know what you think? Am I missing something?

Hi Rishabh

An alternate view for your consideration

1. Valuation post demerger (analysis done on a pre-tax basis for simplicity - please do your own post tax assessment of cash payment)

2. GCC Cash cow and outloook for future investments

3. Competitive dynamics

Hope this helps in your thoughts

Disc: Invested with a full position and likely to be biased. Am not a SEBI registered advisor and none of the above is investment advice - please do your own due diligence

* From an industry perspective, you could look at other similar companies (my review was EV/EBITDA is of the magnitude of 18-40). So on a relative basis looks fairly valued to undervalued (depending on what multiple you use). Once detailed historical financials for India business are available, should be possible to understand DCF basis

Narayana Hrudayalaya Ltd

EVEBITDA 21.5

Operational Beds - 6096

Founded - 2000 - 24 year ago.

Compared to Aster India

EVEBITDA – Valued more than NH post demerger

Operational Beds - 4080 (India - other than Kerala it is Asset light)

India operation started around 2014.

Key aspect is Aster yet to establish out side Kerala which enjoy its GCC brand recall.

My one cent is India business is unfavorable.

Interesting view Mr. Amrish - you are certainly more experienced than I am in the markets, and have clearly found a contrarian bet.

However, prima facie I would still stay away from Aster given my experiences when promoters sold the cash cow.

Dividend by Aster shall be in the range of Rs 110 to Rs 120/= per share

Shareholders approve separation of GCC business from India Business of ASTER.

Why did Aster DM fell by 20%, any reason?

It’s trading ex dividend

Any news on Q4 Results ?

There is news about morgan stanley buying Aster Stock and brokerages giving target of 418

Few of my takeaways from Q1 FY25 of Aster DM Healthcare

𝐂𝐨𝐫𝐩𝐨𝐫𝐚𝐭𝐞 𝐓𝐫𝐚𝐣𝐞𝐜𝐭𝐨𝐫𝐲:

Aster DM Healthcare’s business outlook appears promising, with the company reporting strong operational and financial performance in the latest quarter. The company’s focus on expanding its hospital network, especially in tier-2 and tier-3 cities, aligns with the growing demand for quality healthcare services in these regions. The management’s emphasis on maintaining sustainable margins and improving operational efficiency suggests a well-planned strategy for long-term growth.

𝐒𝐭𝐫𝐚𝐭𝐞𝐠𝐢𝐜 𝐁𝐥𝐮𝐞𝐩𝐫𝐢𝐧𝐭:

𝐌𝐚𝐫𝐤𝐞𝐭 𝐃𝐲𝐧𝐚𝐦𝐢𝐜𝐬:

𝐈𝐧𝐝𝐮𝐬𝐭𝐫𝐲 𝐓𝐚𝐢𝐥𝐰𝐢𝐧𝐝𝐬:

𝐈𝐧𝐝𝐮𝐬𝐭𝐫𝐲 𝐇𝐞𝐚𝐝𝐰𝐢𝐧𝐝𝐬:

𝐈𝐧𝐯𝐞𝐬𝐭𝐨𝐫/𝐀𝐧𝐚𝐥𝐲𝐬𝐭 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬:

Analysts raised concerns regarding the performance of the Andhra Pradesh and Telangana clusters, which have lower margins compared to the company’s other regions. The management acknowledged the challenges and provided a detailed plan to improve the performance of these clusters, including optimizing costs, leveraging government schemes, and building on the company’s existing presence in the region.

𝐂𝐨𝐦𝐩𝐞𝐭𝐢𝐭𝐢𝐯𝐞 𝐋𝐚𝐧𝐝𝐬𝐜𝐚𝐩𝐞:

Aster DM Healthcare operates in a highly competitive healthcare industry, with both regional and national players. However, the company’s strong focus on expanding its presence in tier-2 and tier-3 cities, where competition is relatively lower, as well as its emphasis on specialized and quaternary care services, provide it with a competitive advantage.

𝐅𝐮𝐭𝐮𝐫𝐞 𝐏𝐫𝐨𝐣𝐞𝐜𝐭𝐢𝐨𝐧𝐬:

The management has provided a positive outlook, targeting a consolidated EBITDA margin of 20-21% in the medium term and a hospital and clinic segment EBITDA margin of 23-24%. The company’s ability to achieve these targets will be crucial in determining its future performance.

𝐂𝐚𝐩𝐢𝐭𝐚𝐥 𝐃𝐞𝐩𝐥𝐨𝐲𝐦𝐞𝐧𝐭:

Aster DM Healthcare’s capital allocation strategy appears prudent, with the company planning to fund its expansion primarily through existing cash reserves and operating cash flows, without the immediate need for dilution. The management’s openness to exploring inorganic growth opportunities, subject to favorable valuations, is a positive sign.

𝐎𝐩𝐩𝐨𝐫𝐭𝐮𝐧𝐢𝐭𝐢𝐞𝐬 & 𝐑𝐢𝐬𝐤𝐬:

Key opportunities for Aster DM Healthcare include:

Potential risks include:

𝐂𝐨𝐧𝐬𝐮𝐦𝐞𝐫 𝐏𝐮𝐥𝐬𝐞:

The company’s focus on providing quality healthcare services, expanding its presence in underserved regions, and leveraging specialized and quaternary care capabilities suggests a positive customer perception.

Potential merger with Blackstone backed Care hospitals on the card…

[Aster DM in advanced talks with Blackstone to expand its hospital network - CNBC TV18]

https://www.medicalbuyer.co.in/aster-qcil-merger-blackstone-likely-to-hold-majority-stake/

Page 15 on concall:

I think the only thing we are quite keen on is building Aster India and like I mentioned in my opening remarks as well our Chairman’s vision has always been how do we become one of the top three. So just looking at the right opportunities in terms of mergers, acquisitions that are available that will help us facilitate. So we’re just being opportunistic on that, looking, keeping our eyes open. We could not really focus on any of this until the GCC segregation was

over. So I think since that has given us kind of a cleaner slate now, it just opens up for other combinations and opportunities to be explored. So hopefully we’ll have something more concrete to mention in the next couple of quarters.

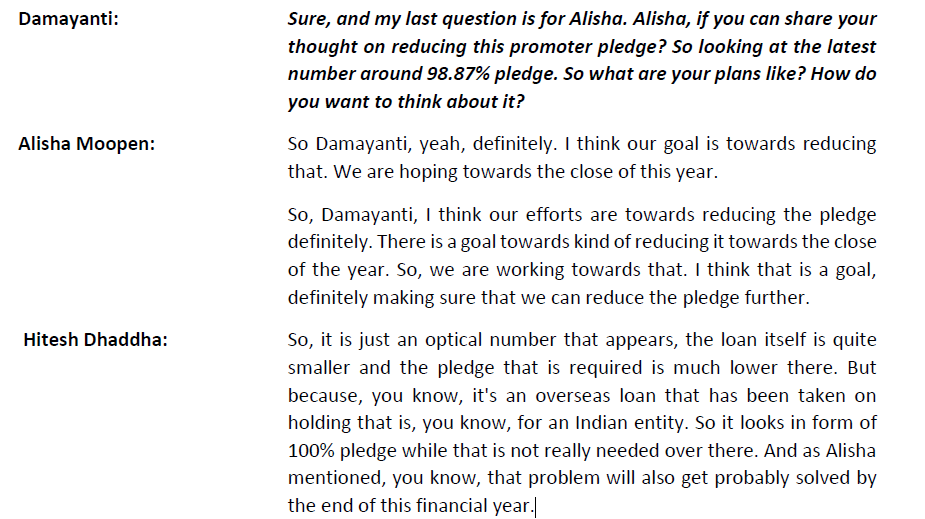

The company has pledged 98.9% of its holdings. A very high amount of pledging. Would be grateful if anyone tracking this company for long can explain.

this has happened now

what would be the consolidated PE of combined entity? Just wanted to understand what PE it is commanding after merger