https://www.bqprime.com/business/aster-dm-considers-hiving-off-gulf-india-health-care-units

This has been in discussion with quite some time, I preferred demerger over slump sale as Indian unit is still not there

https://www.bqprime.com/business/aster-dm-considers-hiving-off-gulf-india-health-care-units

This has been in discussion with quite some time, I preferred demerger over slump sale as Indian unit is still not there

The stock tanked 9% last Thursday. Any idea why it lost so much? The quarterly results were not THAT bad. I did a Google search but could not find any news other than the results.

Certainly I missed something.

I feel it’s just technical correction after recent spike in price… Results were also slightly below expectations.

Was reading the last con call and the management still keeps eluding about restructuring plan, mentioning that everything is in pipeline, hiring bankers, etc.

What I am concerned about is at what price / valuation would they be willing to sell the GCC business? How will the proceeds be distributed among shareholders? Or is this going to be retained by the company? Also, what is the need to sell GCC business? That was their cash cow. Can anyone clarify on this plz?

The market is not discounting this uncertainty. I am surprised by that.

Disc: Invested and planning exit strategy based on restructuring plan.

Aster Q2 Results

Poor results, esp compared to NH. In the Q1 call management had said the lean period of Q1 would be reversed in Q2 in GCC business, but does not seem to have happened. India business is doing ok, but on a much smaller base.

From the Inv PPT, looks like the decline is attributed to the drop in vaccination revenue, which had a hefty 50 % margin. Would be interesting to hear from management in the inv call. Also the long pending restructuring of the GCC business.

Regional Breakup

Segment Breakup

GCC - H1 performance is poor. Since Q1 is lean period due to holidays, with expats going to their home countries, I took the H1 and compared, and the results are very poor.

Inv PPT: https://www.asterdmhealthcare.com/fileadmin/user_upload/Investor_Presentation_Q2_FY_23_to_upload.pdf

Disc: Invested and holding.

Aster Conf call notes

Dr Moopen

Alisha Moopen

Investor Questions

Aster DM Q3 concall updates -

Revenues 3192 vs 2650 cr, up 20 pc

EBITDA at 449 vs 397 cr, up 13 pc, margins at 14 vs 15 pc

NP - 160 vs 168 cr due higher interest and depreciation costs

Aster India business growth at 25 pc with revenues at 771 cr, EBITDA at 115 cr, up 13 pc

India business PAT at 30 cr vs 27 cr YoY

GCC revenues grew 19 pc 2420 cr

GCC EBITDA at 334 cr, up 13 pc

Current capacity -

30 hospitals, 15 each in GCC and India

Beds - 5536, GCC- 1441, India - 4095

Clinics - 113 in GCC, 12 in India

Pharmacies - 257 in GCC, 239 in India

India Hospitals distribution -

Kerala -6

AP- 4

Karnataka- 3

Maharashtra - 01

Telangana- 01

GCC Hospitals split -

UAE -09

Oman -04

Qatar -01

Saudi -01

Revenue split-

Region wise - GCC-70 pc, India -30 pc

Channel wise - Hospitals - 61pc, Pharmacies -17 pc, Clinics - 22 pc

Hospitals pipeline-

India-

04 in Kerala under construction with bed capacity at 750

03 in Karnataka under construction total bed capacity at 875

02 in AP are in pre operational stage with bed capacity at 200

GCC-

01 Hospital each in Doha, Dubai,Saudi. Total - 245 beds

Some highlights -

COMPANY ACTIVELY LOOKING TO SELL GCC BUSINESS

HAS APPOINTED MERCHANT BANKERS FOR THE MERCHANT BANKERS FOR THE SAME

HAS STARTED RECEIVING GOOD INVESTOR INTEREST FOR THE SAME

BINDING BIDS LIKELY TO BE RECEIVED BY Q1 FY 24

Current number of Pharmacies in India at 240.

Looking to add 120-150 pharmacies in India every year

Most of India hospital expansion to be via operate and manage model vs owning model. So the margins may be a little lower, but ROCE would be very high.

Aim to add 500 beds/year for next 4-5 yrs under this Operate and Manage model

Aiming to sell own labeled medicines in the Pharmacy business to boost profitability

Aim to spend 250-300 cr per year for India expansion. Aim to keep Debt/EBITDA ratio under 2

Currently, the AP,Telangana mkts underperforming for the company. Aim to go back to 15 pc EBITDA from these mkts by next FY and grow from there

GCC pharmacy sales were very strong in GCC due same store growth and greater share of private label medicines

MyAster app in GCC and home deliveries in GCC also boosted pharmacies profitability

India occupancies-overall at 68 pc

Kerala-80 pc

Karnataka-60 pc

AP, Telangana-50 pc (had stopped treating govt scheme patients. Restarting now)

India can go upto a peak occupancies of 85 pc

AP, Telangana EBITDA margins currently at 8-9 pc. Likely to go upto 15 odd pc in a steady and progressive manner

Disc: planning to take up a tracking position

From time and again I’ve asked one question… why are they selling GCC business? It was and is cash cow.

My Opinion

Aster Healthcare started from GCC and all through times they are vocal about GCC getting low valuation multiples (also present in this thread).

Developments in UAE: Abudhabi which is the capital of UAE is pushing all the companies in their country to list on ADGM (Abudhabi global markets).

If Indian markets give a very cheap valuation to the company, why not buy the shares(62% of GCC) of Aster in “slump sale” (according to the CFO) and list it in ADGM where a real valuation is given to Aster GCC.

I think this is the primary reason for the slump sale. To complete this they will engage with some PE firms to buy out their stake and list it separately in time in ADGM.

Aster selling GCC stake to PE firms

Aster GCC single handedly could get interest at low rates(6-7%) and build the whole India business from scratch starting from Kerala, today they have close to 15 centers and all Multi-speciality and not clinics. I think the primary motivation to ‘slump sell’ is the lack of valuation given in Indian Markets and attractive offerings that can be got in ADGM.

To give you a perspective

Apollo Assets according to their books is 13000 crores and their valuation is 61588 crores.

Apollo is into (Hospitals, Clinics and Pharmacy). Apollo is audited by Deloitte and Haskins

and

Aster is into the same and if you visit Dubai or Abudhabi, you will find their pharmacies every nook and corner just like Apollo and they have Clinics and Hospitals as well which are proportionate to the population in UAE, Deloitte and Haskins audits Aster DM Healthcare books.

The only exception is Apollo realises most of its money on the go and Aster gets it a little late because all its money including from Pharmacies is from insurance.

Important part is what is the fair value of the company or GCC business. For me, it is rational to have a valuation which is similar to Apollo

When i went through the thread i found that few management changes happened abruptly. These things happen, generally a venture capitalist or any family owned business starts operations in a country they will try to have their men(family/primary stakeholder employees) in Finance, in board where they can have over sight on the operations. If they see fraud they are immediately terminated. I think so management terminations happened that way.

But for the readers perspective(who might not have a good understanding of doing business in GCC) lets assume prospects are mediocre and get into valuations.

Numbers could vary a little because i some mental math to add last 4 quarters based on their investor presentations(1,2)

Indian Operations (last 4 Quarters)

Operating Profit is at 407 Crores

Apollo is valued at 80PE and 30 times operating profit.

Fortis/Rain bow at 20/22 times operating profit

lets assume Aster is equivalent to Fortis so the valuation would be

20 * 407 == 8000 crores

GCC operations (last 4 Quarters)

Operating Profit is at 1116 Crores

Operating Margin is ~14%

If i value them with companies like US or less than them at 12 times operating profit(40% less than Indian business valuation)

12 *1116 = ~13400 crores

UAE base Burjeel which healthcare/hospital player is smaller in size compared to Aster and at their peak of revenue/ebitda which is last year, went for an IPO in ADGM at 14.5 time EBIDTA . Links(Bloomberg link,CNBC link,IPO Prospectus link)

(Healthcare companies in US).

United Health group 13.5 times operating Profit 10-11% opm 22PE

Elevance health 10.5 times operating Profit 7-8% opm No PE)

Based on these assumptions if i value them it would be

operating profit based

8000 +13400 = 21400 crores which is 75% above current market capitalization.

To bring this to perspective a mediocre valuation would mean a share price of 240 *1.75 = Rs.420

Other Notes:

I don’t want to value by PE because the GCC operations posted -40% profit for last 9 months.

Aster has a total Assets of 13600 crores which is same as its market capitalization and Apollo has an assets of 13900 crores.

Let me know your thoughts, if i missed anything or didn’t consider anything.

Disclosure: ~8% of PF @240

I read little bit about aster as I knew it when I was in UAE for some time. My take on the company is it is known as common name running OPD clinics - I never found them to be in the hospital like Burjil or other GCC grown hospital. They wanted to utilize the brand value they created in UAE by running hospital chain in India. This is Claver move by the Aster as people age above 60 move back to home country after work and look for better service back in the home country for them and family.

Is company really undervalued?

I agree with your point that management thinks it is undervalued and looking to bring in privet investor to its GCC business.

My one cent on why Apollo stand better against Aster

With story “NMC Hospital” still fresh I would take GCC number more carefully. Indian business they have grown in Kerala which they took full advantage of brand value from GCC and rest of the expansion will be time tested.

Aster as a Pan India player still long way to go to be compared to Apollo. My take is it is not undervalued.

Thank you for the review @Girish_Kolari

Below are the three things you are questioning in my rationale.

Aster Hospitals & Clinics have (45% + 35%) contribution to EBITDA last 4 quarters.

Aster has 81% from hospital+clinics, so its not apple to apple comparison.

However if assign weightage to each like the below table and also account all the unallocated and elimination numbers i would get a GCC Valuation of ~12500

| (in Crores) | ||||

|---|---|---|---|---|

| EBITDA | GCC Hosptials | GCC Clinics | GCC Pharmacy | (Unallocated & adjusted |

| Q42022 | 156 | 115 | 67 | -52 |

| 9MQ32023 | 417 | 340 | 178 | -217 |

| Total | 573 | 455 | 245 | -269 |

| Burjeels overall | 14.5 times EBITDA 70% Hospital | |||

| Valuation multiple | 16 | 11 | 8 | 12.67 |

| Valuation Totals | 9168 | 5005 | 1960 | -3409.1 |

| GCC Business by EBITDA | 12723.9 |

Apollo has almost all of this hospitals assets in Land where as Aster doesn’t they comparatively are asset light. (Ref.

indianhealthcare-3-3-22-pl.pdf (2.0 MB)

)

PE firms will always a full forensic audit of their numbers, if Aster has been over stating numbers or being unethical they wouldn’t go to PE business. It is reasonable to say numbers are safe.

Frankly i think this is a special situation where you can leverage difference in valuations, Asters management is seeing for a temporary gains(Cigarette butt stock). Like you said there are many more things to look at if some one wants to hold it for long. My objectives is the special situation.

Let me know if you have any more questions.

Promoters acquired 4% from Olympus Capital Asia investment @230 Rs.

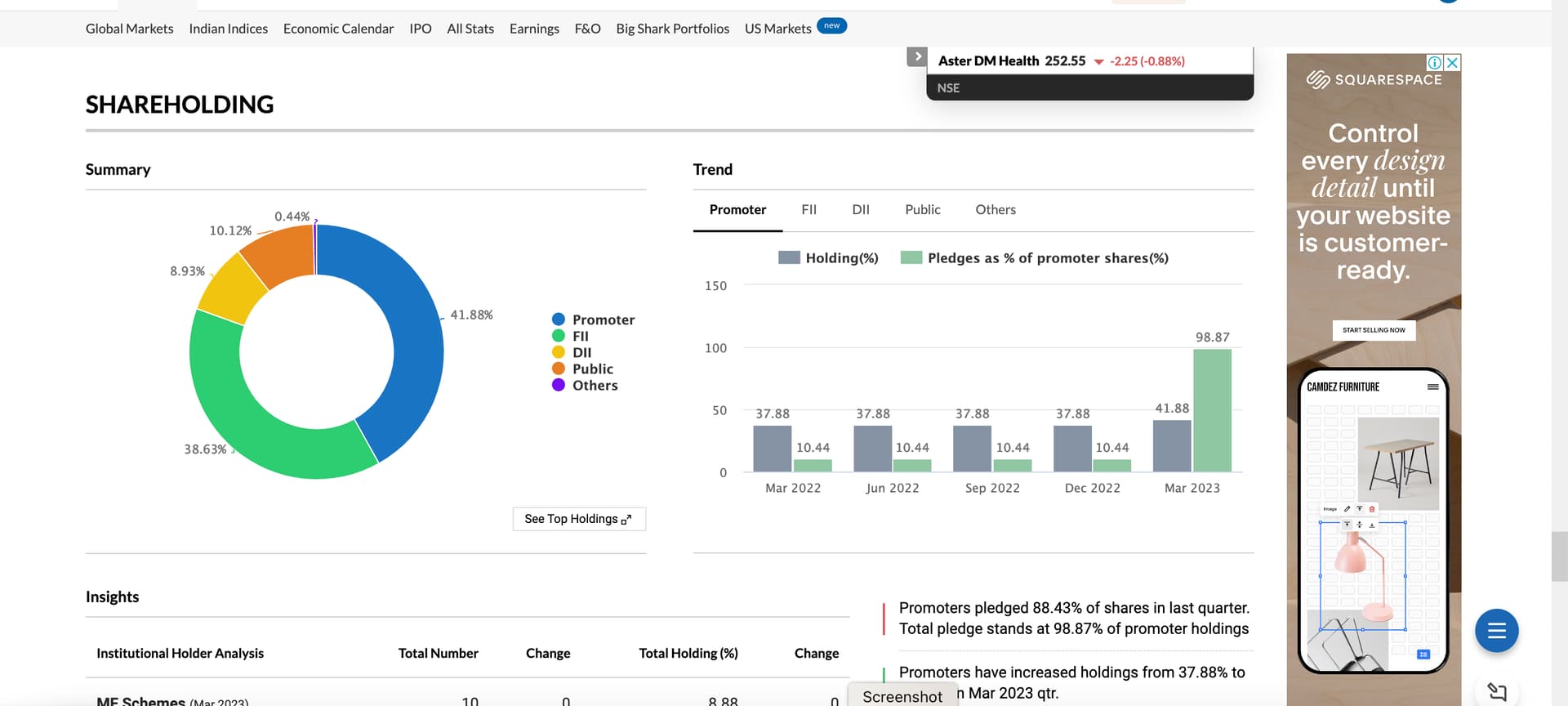

Anyone has any idea why promoters pledged 99% of the holdings in March 2023 - info from moneycontrol

Dear @vamsi21 thank you for your perspective.

My thoughts:

- On sale of GCC business:

If there is a slump sale of GCC business and then listing on ADGM by new investors/PE then it would be loss to current shareholders as the value they get from sale would be very very less than it’s intrinsic value. The PEs being a ruthless negotiators will give very less value because the only money they are going to make is from delta of buy and sell valuations.

I am not sure what benefit promoters themselves will get out of this sale. No promoter will sell their business because the stock price is not valued by market! Less valuation of stock price is not going to individually affect them unlike rest of us retail investors (unless they are selling their stake)

Why doesn’t the promoters themselves list the GCC subsidiary on ADGM? Can an Indian listed company list it’s subsidiary on foreign stock exchange?

This whole thing is negative for existing investors and the share price should decrease but the stock price keeps increasing. So I am not able to understand why market is ignoring this sale of business.

- Investment thesis:

I live in Riyadh and am very much aware about the healthcare business in GCC. In fact there is Aster Sanad hospital near my residence and I have seen the sheer patients crowd there.

I would prefer to invest in a hospital which has insurance patients (GCC) rather than cash (India). As an insured patient myself, I have never bothered to what and how much I am being charged (pricing power for hospitals). I will not get into the business practices adopted by hospitals for insured patients.

Just look at the healthcare - insurance nexus at America which has made healthcare unaffordable to non insured patients there. Unfortunately/fortunately (depending on which side of table you are) same is being now replicated to other countries.

Promoter pledged shares to raise the money and used the amount to buy 4% shares in the compnay , Chairman said, they will release the pledge in a year. Please check the concall tranacript Q4/2023 for more details

If the promoters sell the GCC business on slump sell basis then at what valuation it would be? Are there any SEBI regulations dealing with determination of such sale price?

How can minority shareholders protect their interests?

#4QWithCNBCTV18 | Aster DM board shall review the proposals for the sale of the co’s biz in the Gulf Co-operation Council region. Binding bids from potential buyers are likely to be received by the end of Q1 pic.twitter.com/aYYeUU7GNG

— CNBC-TV18 (@CNBCTV18Live) May 26, 2023

Hi Everyone,

Need clarity on this:

Promoter acquired a 4% stake from a PE investor at 75 Million Dollars recently. Does it mean they acquired at a higher value than market value or is my calculation wrong?

Requesting people from this thread to comment on this.

Thanks in advance.

Any reason for spurt in price and volume today? Is some thing happening related to sale of GCC Business? Members please share your views.

Most probably some mutual fund buying…Recently HDFC launched its healthcare & pharma fund, so maybe they picked up some stake in it.

Has aster DM gone for Q2 FY 24 earning call? Pl share the link if held.