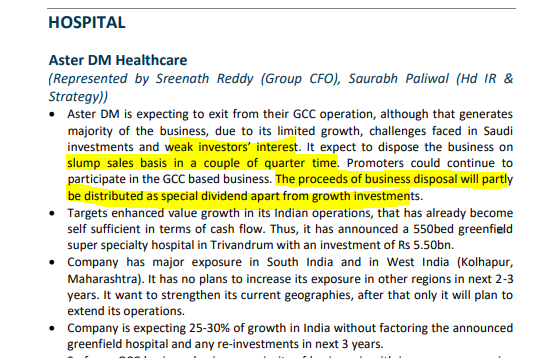

Hi,

I am opening the thread on Aster DM healthcare to seek discussion from the experienced investors.

The company was started by Dr Azad Moopen in Dubai with a small clinic and has now expanded to complete healthcare system in 7 countries.

The company is one of the largest player in health care in GCC (Gulf country) and now expanding base in India. It has also have small presence in Cayman islands.

Infrawise breakup

27 Hospitals (14 in india)

115 Clinics (98% of it in Gulf)

223 Pharmacies (All in Gulf)

81% of the revenue is from Gulf and 19% from India.

PAT breakup

238 crore (Gulf)

-91 crore (India)

All of the profit is from Gulf and currently the company is in net loss from Indian operation.

Note that per patient profit is very high in Gulf countries.

Why to get interested in the company ?

(a) The loss in India is due to expansion phase. After the expansion, the operating leverage may kick in and profit will be realized.

(b) Strong regional presence in South India and the company is working to leverage the foothold to expand clinics and pharmacies.

(c) Growth Prospects

New hospitals and clinics are in development phase both in India and Gulf.

Location : Gulf

→ Partnership with Roche Middle East, the world leader in biotechnology, as a strategic partner

→ Aster Hospital in Sharjah and the Aster Hospital in Oman would be completed in 2022.

Location : India

→ Three new hospitals in development stage

→ Plan to open new pharmacies and diagnostic centers in areas of strong foothold

Location: Cayman Island

→ One hospital is already in operation.

→ Agreement with Cayman Islands Government to build Aster Cayman Medcity, a 150-bed Multispecialty Hospital over the next three years

(d) Management Innovative Attitude

→ Focus is on using latest tech (like machine learning , blockchain) to improve service quality.

→ Focus on asset light model like teleconsultation, homecare and diagnostics.

I think once the capex is over, the stock will rerate to better P/E.

Valuation Metric

Currently the company is available at Mar. Cap to Sales of 1.2, which is considered attractive observing its peer groups valued at mcap/sales of more than 5.

Currently, the stock is available at P/E of 27, where all its peer groups have been valued at P/E of 40.

The low valuation can be due to high debt ( D/E = 1.2), but the company has been reducing debt for the past 2 years (can’t say about the future though )

Sales

One can observe the increase in sales on YOY basis. One can only expect the sales to grow in future considering the expansion of new hospitals and clinics.

Interest Coverage

The company has comfortable interest paying capacity as opposed to operating revenue.

One can say that company can easily survive the difficult environment.

Operating Cash Flow

The company has been generating positive cash from the operations.

Promoter Shareholding

The promoter owns 37.88% of the share. 10% of share is pledged.

Account receivable / Sales

![]()

AR / Sales data is also looking Ok for the company

Negatives

(a) The company owns lots of subsidiary due to that analysis becomes difficult.

(b) the company is expanding into hospitals, pharmacies in different areas. The risk of fund mismanagement is there.

(c) Being interested in low PE stocks, the PE of 27 makes me fearful (need valuepickr experts to comment on the case)

(d) promoter shareholding of 38% is also a concern.