Given what we now appreciate about the reality of Disruption, How do we go about assigning Terminal Value to a business? That was essential poser to us.

Essentially the higher the Multiple we assign, the larger the time period we assume the business will be alive, so cash flows for so many years can be essentially discounted back to present. And then, how sure are we about going about that process of assigning that Value?

If it is Roti, Kapda, aur Makan - okay there is some basis to do so going by previous uninterrupted centuries of history and the strength of the brand/franchise. But if it is anything else - ? How do we make sure we do not err grossly? Do we even know how to assign value to say a Pharma business?

There are some businesses which have some regulatory-based entry barriers like Pharma and Agri-Chemicals that may make these sectors less prone to catastrophic disruption - falling of a cliff - so to say. So you may have a slightly longer time-frame to observe and course-correct. However even these could face disruption in unimaginable/imaginable ways

In emerging businesses, we may be safer therefore - only if the assigned multiple is lower. Then you are spared having to discount cash flows over a large number of years, without any predictability history so to say.

This is a very important project, we want to work on for next 6 months and form informed views on.

Hence this may remain a locked thread, till such time we have created a coherent but complete discussion flow. We do not want folks to clutter up this thread and/or get unduly influenced, either way

Please bear with us. We will keep populating with compiled Notes, and our original investigations/insights

Why have we put it up prematurely then?

Starting Food for thought for everyone, and a constant reminder for us to prioritise.

We have been given important leads.

we will look for both confirming as well as disconfirming evidence. We are taking this seriously to re-examine holistically our investment preferences, and thus portfolios. That does not mean the Jury is Out!

This is NO DOUBT a very important Input, at this stage of our Investment Learning Process.

We should investigate the subject, and bring this into our Conscious-Decision-Making process, which wasn’t in mine (I will be the first to confess).

At the same time, each of us needs to learn to treat not everything as a Hand-Me-Downs. We need to learn to question and work out things based on what resonates with our own Investment Style, Temperament, and individual experience/Learning so far.

The way I see it, “Terminal Value”, the way Vinay Parikh advocated its use, has its CONTEXT, too

While almost everyone had that “Wow! Eureka” Moment at different times during the 4 days (especially those present in after-dinner conversations late past midnight), I am sure everyone will be lying, if they have rushed to clean up their Portfolios

There is a very big Context difference. Assigning TERMINAL VALUE, is possible for a MATURED business, and of course every mature investor - in a matured business - should live by that Tenet.

It is NOT POSSIBLE for VP Kind of early-stage-growth businesses to assign a Terminal Value, for sure - where we are like Early Adopters (sometimes much before they have crossed the Chasm). But does that mean that it is NOT POSSIBLE to Allocate good capital (bet hard enough) to businesses in a life-cycle-stage where they are yet to cross the chasm, or have just crossed the chasm, where they are yet to reach Early Maturity Stage like a BFL has now, e.g.

If nothing, we all should have the Intellectual Honesty to aver I think - that there is a VP way to that madness too. Somehow we have cracked some part of that code . It can’t be just pure luck, that we have had such exemplary picks in so many industries, many of whom have continued to outperform.

I think the “magic” lay in not just having a “FEEL” and slogging to establish hard facts that lead up to that FEEL with lots and lots of confirming evidence, seeing them walk the talk, re-affirming the FAITH, and re-investing based on new-evidence, every 6 months, every year, every 2 years.

It would be too naive, to dismiss things with - you don’t NEED to assign a Terminal Value when you find a decent-looking business - 30% grower, with 30% RoCE, going CHEAP, say 6x PE.

Rather, the way I see it - the most important part of investing in Early-Adopter kind of companies (apart from getting as good a feel as we can on Management Quality, and Business Quality) - is to KNOW WHAT TO LOOK FOR, 6 months down the line, a year down the line, 2 years down the line.

If we tried to understand the Business as well as we could - we would have a “Moving Forward Hypothesis” (for want of a better word) of this early-adopter business 2 years down the line. I could not articulate it at all initially, jsut focused on understanding as much as we could - put as much FACTS ON THE TABLE - as we could

By 2012, I was getting my early hands around BQ and MQ and would argue endlessly with my friends on superiority of an Astral over a Mayur, And an Ajanta over an Astral, A PI over an Ajanta, and a Shilpa over an Ajanta, example. No one would be convinced - because I had not again learnt to put all things on the Table - In my Mind - while arguing postives/superatives and negatives of Business A versus Business B.

But that is getting ahead of the Narrative.

What I did have always worked out though in my mind, was the clarity about the NEXT LEVEL for these businesses. For a Mayur, it would be when they could get in a BMW, Mercedes in its Order Book - that would have meant it has crossed the Chasm definitively for me. for a PI Industries, it meant Commercial Success fro one of its 13 R&D stage innovator molecules; for PI it also meant when the Innovator: Generic agro chemical sales would reverse? For Shilpa, it was when would it breakthrough in Japanese/Chinese Markets?

Not saying I had a very clear picture everywhere, but my largest allocations/de-allocations in businesses would be on what I could clearly hypothesise as a very plausible picture happening in 2-3 years. So when there was no progress on that Mayur - whole of 2014 and 2015, I had no option but to sell off. But where there was definitive progress, it meant I would allocate more.

Having said all that :), I greatly value the “Terminal Value” Conjunct when taken concurrently with the “Disruption” Conjunct. Together, they have illustrated in very “potent” terms, that I must sanitise my Portfolio, urgently. (My “Chamko” moment, if you will).

If the business is unlikely to last the 10 years profitably, WTF am I doing assigning high-valuations. So it’s important for me to be ALIVE to the fact that in my disruption-ignorance, I might have been completely off-the-mark in thinking about the longevity of my business.

Whether we agree to the efficacy of DCF as a Valuation tool is beside the point, no one can disagree with the main principle behind that the Higher the Sustainable Valuations I assign a Business, the longer I am assuming this business will last, and therefore projecting future earnings back to today. But is there a reverse way using the EPA method that essentially does the same thing as DCF, but is a more tangible way of looking at Future Value Creation (2-3-5 years down the line, in line with current visibility of the business)?

After getting enough hints from VP conference , i have been just thinking about levered businesses and calculating terminal value for them . Big NO to the levered businesses from two guru’s shocked me and started to think more and more . They hinted us to focus more on culture and stay away from companies whose managements talks market shares and fond of growth . I got a sense that in product companies or other businesses , performance wouldn’t get into cliff all of sudden , where as in finance business you will never know until that happens .

Should we consider the businesses which have blow up chances even remotely ? Can we envisage the probabilities ? If you are not sure then how should we calculate terminal value ( at least in our mind ) ? Say if we have 5 year horizon things should be pretty fine for another five years right ?

If we invert our doubts and start to think from customer perspective , then i’m getting lot of doubts . In case of repco , we are celebrating tier 2&3 opportunity , self employed segment , prudent underwriting skills so on . If i think of how story can go wrong i am getting lot of new thoughts . In micro finance sector incentives ( I would dare to say lures ) are driving the loan book growth and end of the that is bad credit . How and when the things will stuck ? In Bajaj finance case say if consumer durables companies are not making money and stop to pay such incentives ( 24 Percent IRR ) , what would be the situation ? Say shriram with 28 percent capital adequacy growing at 10-15 percent . why can’t they shore up the loan book growth at 25-30 percent ?

So the point is while evaluating self reinforcing business models , we should also consider these aspects . Prudence , risk mitigation measures , counter cyclical approach , chances of blowing up , Customer repayment capacity .What are the unique traits in the company and management that prevents these kinds of mishaps .

I would like to post one failure pattern here . I’m not sure whether this case study i apt in this thread .

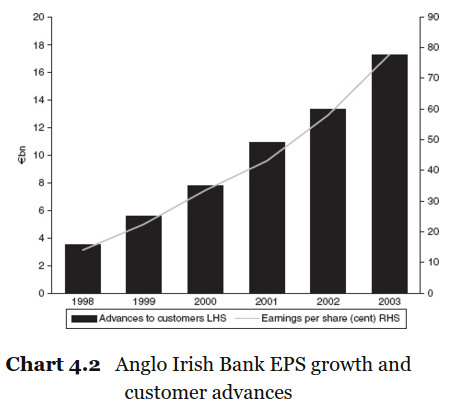

Anglo Irish bank :

Business model : To lend businesses on secured (property ) basis in Ireland and UK without branch network .The competitive advantage is the speed at which they approve loans , customer orientation , Flexibility and speed of execution .Given the branch less execution strategy their cost to income was very low . They relied on word of mouth and no brokers .Their provision coverage ratio was more than regulatory requirements . Average provisions were 210 percent of npa’s against 80 percent of Europe average . Usually loan to asset value is 70 percent . For example if i were to purchase a property at €10 million by signing Ten Year Leasing Agreement ( IMP criteria) with say Mcdonalds should be no problem for paying interest . But when i have to payback principal amount after ten years i have to be financially solvent or atleast property market should not fall more than 65 percent to match remaining loan ( 35-40 percent ) . Same time between 1998 to 2008 property prices were skyrocketing hence this didn’t seems to be risk . Their Loan book grew by 35-40 percent in that period and market cap went up by more than 25 times . It was trading at 4-5 BV with 30%+ ROE.All the investor’s , fund manager’s were very happy by filling in 25% growth in BV . Market cap went up by several times .

Some interesting points Branch less business generation means lower overheads , Low cost to income . same time deprived of raising low cost deposits and solely dependent on banks and other sources . In declining interest rates scenario both bank and customers thrived through lower costs + resultant increased property prices .

Higher ticket size : As their targeted segments were businesses average loan size was €4-5 M .They didn’t have focus on residential segment ( More stable )

Dependent on property lease agreement : Though rents are secured over loan periods their hypothesis was clients will repay as property prices will grow or at least should stay at same levels .

Management had huge stock options and diluted their holding along the stock rally . Management was incentivised for short term goals vs longer sustainability .

What happened later ?

Cheap capital flowed in Irish real estate which pushed assets prices to the sky . People chased the returns . In 2008 when lot of financial institutions went bust , all of sudden capital dried up hence property prices collapsed by 80 percent . Which was more than the Irish Bank assumption of 60 percent .They had to write off more than half of the loan book and subsequently nationalised .

Completely agree with you. In fact after working in Financial sector for mroe than decade, my conclusion is the chances of mine in lending business are much higher than less leverage business. While Prof Baxi was saying 25% for leverage, I would not be satisfied with that ROE for bank.

In my thought process, We have two companies.

Company A: ROE 25%, Growth 15% (Free cashflow), Debt Equity ratio: 0-.25

Company B: ROE 25%, Growth 15% (No free cash flow as lending would require always new capital being infused. I would question how to value Banking company when we know for sure negative free cashflow all through out their operationa), Debt equity: 8: 1

My way of looking at things ROE/Leverage. If the company not contributing significant ROE by leverage, why should one take risk? In my limited study, I have still to get answer on this question and would appreciate if someone can provide insight to same.

Also, is there anyway to value a company which by basic business model can never have free cashflow? I know only method being dividend discounting (which got extended to free cashflow)? How does one value lending business particularly in context of terminal value?

Had a discussion around ‘The terminal value of a growing business’ with Donald during his Hyderabad trip and now I think I have some handle on this issue. There is a possibility that we may say ‘Oh I knew all of this’ (and that happens to all of us more often than not now a days) but I think it is more about perspective and how you look at things and as Donald said somewhere it is all there in the Copeland valuation tome. Some of the explanation below is my understanding of the subject after some more thought on it post our discussion.

Now terminal value of a business which is dying is easy to calculate since the underlying assumption is that there will not be significant asset creation from hereon. But the growth firms (the VP ones) like a PI/Alembic/Shilpa keeps investing in newer assets every year and at the same time keeps generating much higher return on capital from these. If we all remember the BQ Sheet and the company grading (why some companies were slotted higher as A++ or A+) the following three things were relevant:

a) ROCE

b) Ability to deploy incremental capital

c) Risks

Ignoring risk assessment for the time being the two things that can create a multibagger (we all like them) is of course a) & b). Combine the two and ignoring all math what we get is EVA (Economic Value Added).

How do I assess the terminal value of a growing business?

Put the current value of assets (not the book value) in terms of what capital they can generate, assess the future EVA that can be added from future asset creation by the company (of course subjective) and the capital invested in Assets (the book value)

In other words:

Firm Value = Capital Invested in Assets in Place + PV of EVA from Assets in Place + Sum of PV of EVA from new projects

Very clearly for most firms that we are invested in we need to have handle on the plans for next 5 years in terms of capital allocation and at the same time a clear visibility of next 2 years in terms of capital generation to have any decent idea of putting it all together (5yrs and 2yrs are my parameters).

By the way those who read Copeland can easily understand the difference between EVA and DCF. There isn’t much (any?).

Everyone interested in learning to thinking more clearly on Valuation (especially early-stage growing businesses), is encouraged to a RE-READ of this must-have Valuation Tome.

Don’t dismiss it as a DCF book, like I did the first-time. Mr D had gently nudged me (don’t read it in a hurry) read it at a leisurely pace - important to first understand the essential way Future Value is created, every year incrementally. That this can be measured objectively, each year. That if you truly attempt to understand the business, you will have to have a certain view/visibility on the value being added in the immediate future. Then you will also need to get your fingers around the Intangibles!! Start thinking like the Owner of the entire business; put yourself in the shoes of the Owner, how will he Value this business?? How will a 100% buyer of an emerging growing business, VALUE the business???

This 2014 back-to-basics paper by Michael J Mauboussin and Dan Callahan, opened my eyes to the centrality of EPA (EVA) in Future Value creation, and how it can be pretty tangibly measured - as I went back to the Copeland Tome, and did not have to look any further, ever.

The authors maintained thus The sloppy use of multiples is almost everywhere you look. In our opinion, some analysts justify their recommendations with apples-to-oranges comparisons of businesses with different economics, suggest companies should trade at the same multiples as the past without a solid economic justification to do so, and compare price-to-earnings multiples with growth rates without any mention of the underlying economic returns. Price-Earnings multiples are widespread in use, yet remarkably poorly understood.

Hope you find this paper, as useful as I did couple of years back - to try and make sense of how to Allocate Capital to an early-stage growing business in my hands - and realise that we need to consider Incremental Returns on Capital first, and Growth second. Growth only creates Value, if the investments generate a return in excess of the Cost of Capital.

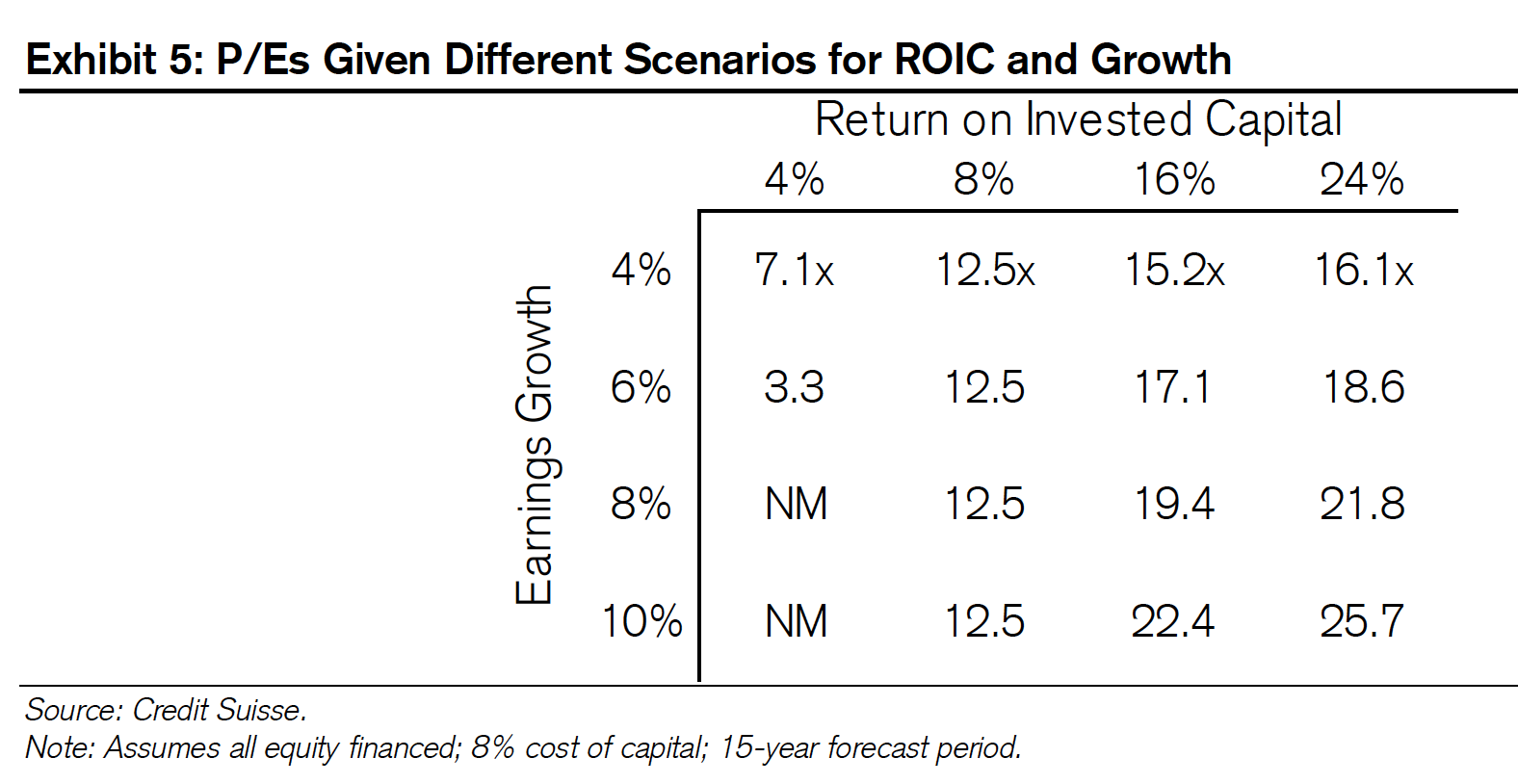

Most relevant excerpts from the Article There are three fundamental concepts that you can take away from the exhibit. First, a company earning its cost of capital will trade at the commodity price-earnings multiple, 12.5 times in this case, irrespective of growth. You can imagine these companies as being on an economic treadmill: You can speed up or slow down the treadmill of growth and it makes no difference, the companies are not going anywhere. Value neutral companies must first figure out how to increase ROIIC before they worry about growth.

Second, if a company is generating returns in excess of the cost of capital, growth is good. Indeed, all things being equal, faster growth translates directly into a higher price-earnings multiple. For instance, the warranted price-earnings multiple for a company with a 24 percent ROIIC and 4 percent growth is 16.1 times, whereas a company with the same ROIIC but a more rapid growth rate of 10 percent is worth 25.7 times. The value of high ROIIC companies is extremely sensitive to changes in perceived rates of growth.

Finally, companies that earn below the cost of capital on their incremental investments destroy shareholder value. We can see this clearly in cases when companies overpay for acquisitions and hence transfer wealth to the selling company. Acquisitions are a good example because the acquiring company grows, and in many cases the deal is accretive to earnings per share. That many deals grow the business and earnings yet destroy value is a stark reminder that an acceptable return on incremental investment is paramount.

Academic research shows that the stocks of those companies that grow their assets the most rapidly, a proxy for substantial investment, tend to generate lower returns for shareholders. In theory, companies can rank their investment opportunities in relative attractiveness. The idea is that those companies that invest the most deplete the value creating investment opportunities and dip into investments that are value neutral or value destroying.

The final component of future value creation is how long a company can find attractive investment opportunities. M&M referred to this as simply “T,” but it is also known as “value growth duration,” “competitive advantage period,” and “fade.” This period is closely related to sustainable competitive advantage. Some companies are able to find attractive investment opportunities over a long time by virtue of the industry in which they compete, the strategies they select, the capital allocation choices they make, and some luck.

When thinking about our VP Kind of early-stage-growth businesses about to cross the chasm, I had found the following even more relevant:

The period of attractive investment opportunities has attracted considerable research attention. There are a few things we can say to summarise the work. First, the market tends to impound value creation for many years in the future. It is common for the market to reflect a half dozen years or more of value-creating investment opportunities in the price of a stock. This empirical reality counters the notion that the market is strictly short-term oriented.

_Second, the anticipated period of value creating investment opportunities is different for various industries. For instance, research by Brett Olsen, a professor of finance, suggests that the market-implied competitive advantage period averaged about 8 years from 1976-2007, with a span of roughly 5 years for very competitive industries to 15 years for industries that are more stable.

This range of market-implied competitive advantage periods is tied closely to the reversion to the mean of returns on invested capital. That reversion occurs is incontrovertible, but we also know that the rate of reversion to the mean varies by industry, which explains the range that we see in years of anticipated value creation. This says that industries with rapid reversion to the mean justifiably deserve lower price-earnings multiples, as the second term of the equation will be worth less, all things equal, than that of an industry with a slow rate of reversion to the mean. Slow fade sectors include consumer staples and health care, and fast fade sectors include information technology and energy.

And finally, the real eye-opening part for me, when I had to think of our VP style early-stage=growth businesses with high Incremental RoICs and my (subjective) evaluation of their sustainable competitive advantage periods, versus the more stable matured businesses - and again, I did not have to look back, ever again!

In practice, most analysts have only a vague idea of what expectations a particular price-earnings multiple captures. Exhibit 6 shows three companies that all justifiably trade at a 15.0 times price-earnings multiple. In each case, the steady-state multiple is 12.5 times and the other 2.5 points come from future value creation. This example holds constant factors such as leverage and the period the company can find attractive investment opportunities, which further complicates the task of understanding expectations.

In the top row is a company with high growth in earnings (12 percent) but generating only a modest positive spread (0.8 percentage points) to its cost of capital. The bottom row is projected to grow slowly (3 percent) but with a very large positive return spread (15 percentage points). The company in the middle has a growth rate (6 percent) and a return spread (3 percentage points) that splits the anticipated results of the other companies. So a 15.0 price-earnings multiple can imply very different levels of corporate performance, a fact that the simplicity of the multiple obscures.

The challenge is that very rarely the entrepreneur himself knows how the business will look like 2/3 years down the line.

Let me quote from an recent article in Outlook Business, Jul 22, Secret Diary of an entrepreneur issue:

“I look back sometimes and marvel at what we have achieved - I never had a business plan, just went with the flow and took the next steps. Whenever something looked like an opportunity, we jumped in. It is all about circumstances; it’s a function of being at the right place at the right and doing the right things. I feel lucky…” VG Siddhartha, Founder, Cafe Coffee Day.

PROBLEM WITH TERMINAL VALUE 1 - It cannot be predictably determined.

Let’s go back to first principles.

As a practical matter, the forecasting task is often divided into two sub-components—detailed forecasts over a finite number of years and a forecast of “terminal value,” which represents a summary forecast of performance beyond the period of detailed forecasts.

What is terminal value? The terminal value (continuing value or horizon value) of a security is the present value at a future point in time of all future cash flows when we expect stable growth rate forever.

When I am investing, even in so called stable businesses like, say a, Colgate, can I be sure that people will brush their teeth 50 or 100 years down the line and also using Colgate? I am not sure. They may or may not. I don’t have any visibility that far ahead, forget “forever”.

PROBLEM WITH TERMINAL VALUE 2 - Terminal value is an approximation, so is PE

Had read Mauboussin’s article on PE earlier. He tries to explain that PE is an approximation and should not be used as the primary method of valuation. He does not delve into the details of DCF or any other discounting mechanism of valuation.

Let me quote Graham & Dodd’s Security Analysis (when in doubt, I always go back to the bible):

Find out what the stock is earning. (This usually means the earnings per share as shown in the last report.)

Multiply these per-share earnings by some suitable “coefficient of quality” which will reflect:

a. The dividend rate and record.

b. The standing of the company—its size, reputation, financial position, and prospects.

c. The type of business (e.g., a cigarette manufacturer will sell at a higher multiple of earnings than a cigar company).

d. The temper of the general market. (Bull-market multipliers are larger than those used in bear markets.)

The foregoing may be summarized in the following formula:

Price = current earnings per share x quality coefficient.

The result of this procedure is that in most cases the “earnings per share” have attained a weight in determining value that is equivalent to the weight of all the other factors taken together. The truth of this is evident if it be remembered that the “quality coefficient” is itself largely determined by the earnings trend, which in turn is taken from the stated earnings over a period.

At the end of the day, it needs to be understood that there is NO definitive valuation mechanism that is available and each have multiple assumptions built in.

Terminal value as a concept is good to help think through the longevity of a business, but has limited practical applications beyond that.

What a spirited Defence

Ab toh Guru logon ko bulana padega !!

Let us forget DCF calculations, and come back to the First Principles.

One cannot be arguing that we buy businesses without a view on longevity of the business.

If one accedes that we like to buy businesses primarily with a view on the Longevity of the business (except for the VP Opportunistic Portfolio, which is another nice discussion) - then you have to concede that Size of Opportunity, Long Runway with Sustainable Competitive Advantage, et al enter into our minds while we allot in our minds what we think would be a stable, sustainable PE for this business.

Any which way we argue therefore, however intelligently one may quote Graham & Dodd, or Buffet and Munger, we have to come back to agreeing to the real sustainable Buffet quote “Sustainable” or “Intrinsic Value” of the Business. (Buffet never needed big spreadsheets or complicated DCF Analysis to Intrinsic Value of the Business - If there is Value, it should just scream at you, he says).

If the business is an early stage maturing Business like BFL, and the business keeps getting stronger each year, the Intrinsic Value/Sustainable Value should keep on increasing each year. And we should be happy to buy up. If it is a matured business like 'Colgate" may be the sustainable Value/Intrinsic Value stays at similar levels or eventually declines with time.

If the business is early-stage emerging business (yet to cross the chasm), then obviously it is much harder to put your finger on what kind of sustainable stable valuations you can accord this business, but surely there are ways and means around this typical valuation issue - not all emerging early stage businesses are equal, there are those with clear domination of niches, those where the distance with peers keep increasing with time, and hence chances of success increase with time - an ART form, for sure, but not an unsurmountable a problem - if we can keep exploring more and more indirect pointers to sustainable cash flows in the future

That should be the Quest. That’s the way, I have learnt to think about this.

. It can’t be just pure luck, that we have had such exemplary picks in so many industries, many of whom have continued to outperform.

. It can’t be just pure luck, that we have had such exemplary picks in so many industries, many of whom have continued to outperform.