While reading through the excellent forum on Terminal Value and also the automobile disruption/automation disruption

Some other good reading below

It struck me that we can generalize this to a wider segment and bring together points lost in company specific threads. We can try and identify business models which will CEASE to exit. For example

*When was the last time you purchased a greeting card or gift instead of sending the person a Whatsapp/Email/Gift Voucher Wish? What does this bode for Archies Limited with 5yr sales CAGR 0.7% and profit degrowth? While it is trying to pivot into Indian ethnic stores etc, the jury is open

*When you want a service provider, have you used Urbanclap/Housejoy or referred Just Dial? Why do analysts not believe in its growth.

*How many of us have used a discount broker like Zerodha rather than full service broker like ICICI/HDFC/Kotak? What does this portend for the business models of listed brokerage firms like Motilal Oswal if they do not diversify in future

*There is talk of robots replacing back office functions and automation/IT era replacing low skilled jobs. What does this portend for low skilled/commoditized providers such as *Teamlease

*The recently launched UPI allows inexpensive P2P payments at just 25paise/txn. What does this portend for the business models of PAYTM’s listed holding company One97

*AirBnB and OYO are disrupting the leisure travel segment with ‘on demand’ housing at many segments. Many other websites also offer alternative experiences(like Travel Triangle). What does this bode for the timeshare industry such as Mahindra Holidays & Country Club. Will it disrupt them with people becoming less willing to lockin high amounts and be tied to a vacation instead of ‘On Demand’

*Abroad, people are ‘cutting the cord’ and downgrading their cable plans to instead watch internet. While the Indian scenario is presently different with broadband being expensive and streaming being costly being non zero rated, things could change if Jio like plans allow realistic use of Netflix/Jio Movies. While content providers will escape while earning from the new ‘pipe’, what could happen to broadcasters/DTH players like Dish TV Do note unlike cable broadband players who can bundle broadband and cable, this option is not open to pure play DTH players

Please note I am not referring to industries hit by demographic trends/electronic trends like writing instruments(Linc/Camlin) which may see slow growth but whose necessity is not under question/doubt. Comments welcome and hopefully we can build on this topic. If there are examples from other threads, please LINK to the comment on that thread so that stuff is not reproduced. Also, please let us refer a listed Indian company in our answer so that this becomes more immediately actionable intelligence.

I would also like to give attention to Battery Players like Amaraja and Exide who could be hit when the full blown concept of Electric Cars is introduced which btw is already at a quite advanced level going by what we read about Tesla and its innovations

From as much i understand all the current Batteries are all Chemical Based batteries whereas Electric cars will have batteries which are chip / circuit based which is economical and would have higher capacity to boost power

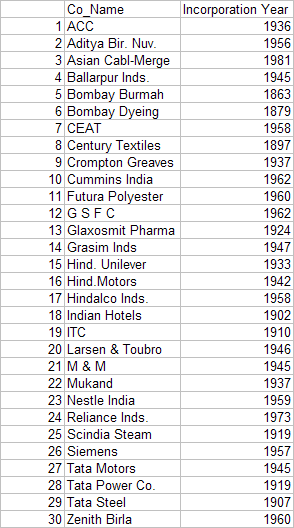

It’s like saying “tell me where I am going to die so I will never go there”. I don’t think such a list is possible. On the other hand, all dominant businesses that exists today were tiny just a generation ago (about 30 years). so extrapolating that, we can say many of what exists today will become insignificant in 30 years. Just look at composition of Sensex when it was created in 1978.

Looking at pace of innovation and integration of Indian economy with global economy, I think in another 35-40 years, Sensex will be made up companies that are not even born. I think Darwin’s theory of evolution also applies to stock market. It’s the survival of the flexible who adapt and demise of the dinosaurs.

I feel Jio is hyped too much. Do you think they will be able to match up with a full strength security solution ? Will a power user ever use a AV from Reliance? It is not their expertise.

All intermediaries like stock brokers, insurance agents (bancassurance) are set for disruption.

Banking as an industry can also be very severely disrupted by Blockchain technology (peer-to-peer transactions). Now whether it will impact any of the listed players or they will themselves evolve into users of such technologies, remains to be seen.

Energy industry is another which is changing. Both in Upstream & Downstream. Move from Oil & Gas to Renewables is a major theme that is getting pushed due to cost and climate change. Impacted companies - HPCL, BPCL,IOC, Cairn, ONGC, Suzlon…

If banks adopt blockchain tech, it won’t make a difference to the consumers, isn’t it? It certainly makes for a buzzword but don’t see it changing or disrupting the way we bank anytime soon. Am I missing something?

The energy sector is a good example, but corporations with vested interests and an energy deficient country like India will certainly have a place for alternatives along with the conventional sources of energy.

All sectors except catering to Roti ,kapda ,and Makaan are vulnerable for disruption Because all other things which have arisen too satisfy mankind rising aspirations are in the disruption curve always.

Expertise does not matter in security software. They can license the engines and technologies of a renowned security provider and distribute it as their own. This is a very common practice. Many softwares like Emsisoft, Bullguard, F-Secure have licensed Bitdefender engine in their products. They do have some of their own technology though! Jio Security for Android licenses the paid version of Norton and provides it for free for their prime members.

Another company which I think will need to rethink their business strategy is Linc Pens and Kokuyo Camlin. I saw that Linc is continuously upgrading their strategy by launching innovative products like Linc Touch which is a Pen on one side & a Stylus on the other side.

As somone working in the writing instruments business, I do not see this concept getting adopted. Their stylus is merely a round rubber at the end, something like mechanical pencil+eraser combo. I am sure smart Indians have figured out the jugaad like those who critiqued Juicero(a subscription based juice squeezer which collapsed when people showed it could be done by hand) of just using any object!

Intermediaries have a significant role to play to ensure trust in payments.For micropayments, stuff like UPI or wallets works, but otherwise, you need someone who owns the platform and can ensure trust. Take Ebay as an example even though they pride themselves as C2C, they have embedded PayPal to add a trust layer and adjudicate disputes. What happens in case of quality defects, quantity disputes, allegations of fraud, hacking etc? It is at those times where the MDR(Merchant Discount Rate) pays for itself. Personally, for a high value purchase, I would much prefer credit cards to allow me that added layer of protection/claim against merchant, which a bank account payment or wallet payment(Just try PAYTM customer care once, you won’r try it again) wont provide.