Purpose of this note

ASM Technologies is still a high conviction bet in my fairly concentrated portfolio. Prior to the elections, I intend to do a high-level scan of the semiconductor industry, as it stands, to determine whether I should keep holding onto ASM, or whether there are better ways to play the semiconductor game in the listed space. This list of companies below is not exhaustive, and if folks can find listed companies that can pose a serious challenge to ASM Technologies, please let me know.

ASM Technologies

ASM Technologies is an ER&D and design led manufacturing company operating in a variety of sectors, including the (now in vogue) semiconductor space. On its website it highlights the following:

“ASM has over 2000+ Person years of experience in serving reputed Semiconductor Equipment Manufacturing Companies. ASM has the expertise and understanding of design and development of System and Sub Systems of PVD, CVD, RTP, Etch, CMP and Inspection tools.”

To cut a long story short, ASM has the ability to create software and control systems for semiconductor capital equipment manufacturers. In addition, it also has process design, as well as equipment design expertise in this sub-domain. Courtesy of its JV with Hind High Vacuum, it also has the precision engineering capabilities to manufacture semiconductor industry equipment. This includes both entire systems and individual sub-systems.

The company held an EGM in March 2024, where they announced a potential acquisition in the semiconductor equipment manufacturing space, which would be done at the JV level. In addition, let us not forget the proposed ₹170 cr preferential allotment (₹38 cr equity shares, and ₹132 cr warrants), in which Mukul Mahavir Agrawal is playing a critical role (nearly ₹72 cr), and the promoters are also participating (primarily with warrants). Long story short, I am a fan, and I intend to find another company that can match ASM.

I am connecting dots into the future here, but initially, the company can work as a contract manufacturer of sorts for semiconductor equipment manufacturers. However, over time, I see a scenario where ASM can start manufacturing customized equipment of their own, which they can sell directly to semiconductor plant operators, while the larger equipment manufacturers focus on off-the-shelf models, but still take advantage of ASM for contract manufacturing work.

Finally, in a world where there are multiple players designing, optimizing and manufacturing chips, I want to focus on the entities designing/selling the equipment that’s required to make this all happen. In short, during a gold rush, I want to bet on the entity selling shovels, not an individual miner.

CG Power & Industrial Solutions

CG Power & Industrial Solutions is a global enterprise providing end-to-end solutions to utilities, industries and consumers for the management and application of efficient and sustainable electrical energy. It offers products, services and solutions in two main business segments, viz. Power Systems and Industrial Systems. The company’s stock price has increased considerably since it become a Murugappa Group company.

CG, a part of Tube Investments of India Limited and the Murugappa Group, Renesas Electronics Corporation (Japan) and Stars Microelectronics (Thailand) Public Co. Ltd., recently signed a joint venture agreement to build and operate an OSAT (Outsourced Semiconductor Assembly and Test) plant in Sanand, Gujarat. The ownership percentages will be 92.3%, 6.8%, and 0.9% respectively. The JV plans to invest 7600 cr over a five-year period, with a capacity that will ramp up to 15 million units per day.

While this is promising news, OSAT plants are not the same thing as semiconductor fabs, and serve a supporting role after integrated circuits (ICs) are manufactured/fabricated. Additionally, at this stage, I cannot comment on what the revenue contribution from this JV will look like, and given the massive run-up in CG Power’s share price, I worry about the margin of safety.

MIC Electronics

As per its website, MIC Electronics Limited is a global leader in the design, development & manufacturing of LED Video Displays, high-end Electronic and Telecommunication equipment and development of Telecom software since 1988. An ISO 9001:2008 & ISO 14001:2004 certified, it has a marked presence in the highly dynamic domains of:

• LED Video, Graphics and Text Displays

• LED Lighting Solutions

• Embedded, System and Telecom software

• Communication and Electronic Products

This company’s exposure to the display space piqued my interest. However, I personally am not qualified to determine if they have any unique expertise here. Additionally, much larger players are lining up to get approvals and incentives to set up LCD display manufacturing units in the country, and looking at MIC Electronics’ 10-year revenue trend, I am not bullish about the company’s prospects.

Mindteck (covered previously, but recapping over here)

Mindteck has expertise in developing supporting software (apps, databases, etc.), and control systems (including factory automation systems) for semiconductor industry operations. In its filings, the company doesn’t explicitly mention client names, but is more open about project details when compared to ASM Technologies. Semiconductor industry clients include capital equipment manufacturers, subsystems vendors and fabs.

Process design, along with subsystem and system design, prototyping and manufacturing (whether it’s proprietary or as a contract manufacturer) is going to be a much harder domain for potential competitors to break into here in India, versus software and control system development. Since Mindteck is primarily focused on the software and control systems aspect, I will give the company a pass.

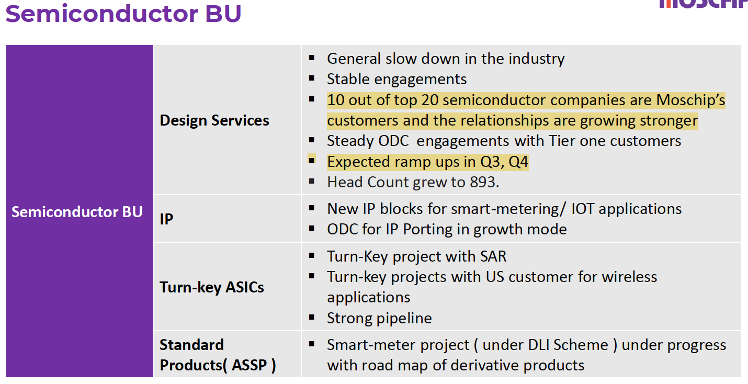

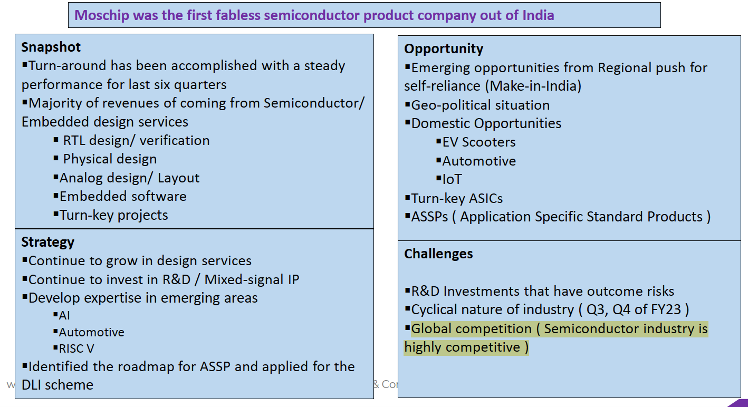

MosChip Technologies

This is a very interesting company. In the semiconductor space, MosChip offers turnkey analog, digital and mixed-signal ASIC (Application-specific integrated circuit) and IP (intellectual property) design services. With an overall unparalleled tape out expertise on more than 200 multi-million gate ASICs with stringent power and speed requirements, taping out designs in all leading foundries in process nodes all the way from 500nm to 7nm, and with time tested and proven methodologies/flows using leading EDA (electronic design automation) tools, MosChip has emerged a leading semiconductor design services house providing expert Spec to GDSII services for customers globally. MosChip has been building its own digital IP and analog IP over the years. Over the past 2 decades, MosChip has developed and shipped millions of connectivity ICs. MosChip has expertise in Serdes (serializer/deserializer) designs and its 6G and 10G Serdes designs are production ready.

Moschip has additional feathers in its cap. It is part of TSMC’s DCA (design centre alliance), and has been shortlisted for the Government of India’s HPC (high performance computing) project.

There are is a lot of terminology in here, but in my estimation, Moschip is a fabless engineering services company that helps clients design and optimize their integrated circuits (chips). The company’s website and investor relations page has definitely improved over the last few years, and management has mentioned that a ramp up in revenue is on the cards. This is all good news, but with the company trading at around 10x revenue, and the fact that I would rather bet on the shovel maker/designer, I still like ASM Technologies.

RIR Power Electronics

In the semiconductor devices domain, RIR Power Electronics manufactures low and high-power semiconductor devices like diodes, thyristors modules, and bridge rectifiers by processing chips from 28mm to 125 mm in diameter.

The company made headlines with the Odisha government’s approval to invest ₹511 cr in the establishment of a state-of-the-art fabrication and packaging facility for SiC (silicon carbide) devices.

I do not know enough about RIR’s semiconductor device manufacturing expertise to comment how they would perform in a very competitive environment. Additionally, with the company currently trading at over 20 times revenue, I worry about the margin of safety.

SPEL Semiconductor

SPEL is a pioneer the Indian OSAT market. SPEL is a trusted & strategic contract manufacturing partner for many of the world’s leading Semiconductor companies. SPEL provides full turnkey solutions that include Wafer sort, Assembly, Test and Drop-shipment services which help Customers accelerate time-to-revenue for their new products. SPEL also offers value added services such as Package Design, Failure Analysis and Full Reliability Test, Test Program Development & Product Characterization.

So, this company also is in the OSAT portion of the semiconductor industry value chain, well outside my preferred area of interest (semiconductor industry capital equipment). Additionally, given how much larger players like CG Power and Micron are entering this space in India, I worry about SPEL Semiconductor’s prospects. Their 10 year revenue trend is a cause for concern.

Titan Engineering and Automation Limited (subsidiary of Titan Company)

TEAL, a wholly-owned subsidiary of Titan Company, was born as the in-house engineering team dedicated to high precision component manufacturing and designing manufacturing automation machines. The company now caters to external clients as well, and has over 500 employees in two divisions – Manufacturing Services and Automation Solutions.

Its solutions span Aerospace, Defence, Transportation, Electrical & Electronics and Medical sectors. Driven by its ambition to be a significant global player, it now provides solutions in over eighteen countries, including Germany, France and the USA.

What caught my attention was an article from December 2023, where the company said that it would spend ₹220 cr to ramp up its fab component unit. The company started supplying components in 2022 and may probably be the first Indian company in the supply chain for semiconductor wafer fab equipment. So while ASM was focused on design and optimization (and maybe some prototyping) back then, TEAL was already in the manufacturing game.

The CEO, NP Sridhar added, “We are now making 200-250 components required for our semiconductor manufacturer client. We have invested Rs 30-40 crore already in setting up processing lines and a 1,000-class cleaning room.” He declined to name the client, citing a non-disclosure agreement.”

Additionally, as of last week, Apple is in the final stages of discussions with Murugappa Group and Tata group’s Titan Company (specifically TEAL) to assemble and possibly manufacture sub-components for iPhone camera modules, according to a report by The Economic Times. This move could increase Apple’s dependence on the Indian supplier ecosystem for its products as it continues to shift operations away from China.

In FY2023, TEAL had a revenue of ₹510 cr and an after-tax profit of ₹21 cr. I mention this because compared to Titan’s total consolidated TTM revenue of nearly 49,000 cr, these numbers are a drop in the bucket, and TEAL’s revenue would have to increase by an order of magnitude to meaningfully impact Titan’s stock price. Therefore, even though the company is showing promise in the semiconductor equipment manufacturing space, as well as high-end electronics manufacturing, I still like ASM Technologies more, especially given the higher consolidated revenue contribution that semiconductor industry work would bring, as well as ASM’s many more years of experience in this domain. However, I would like to point out that TEAL has a headstart in actual equipment manufacturing, and should TEAL be spun off and listed, then its valuation could meaningfully move higher.

Disclosure of holding: I kept buying shares in ASM Technologies from 2021 to 2023, with an overall cost basis of ₹227. I have a fairly concentrated portfolio and do not own more than 10 companies at any given time.