ASM Technologies : Engineering innovation

ASM Technologies is founded by Mr Rabindra srikantan in the year of 1992.

Company evolved over a period of time and divested their enterprise software services business and started focusing on their niche skills like product development Engg RnD,Automation solutions,product life cycle, IOT, Virtual reality etc.

Today company standing on a cross road with multiple optionalities under the able guidance of Mr rabindra srikantan.

Before discussing about the company and its fundamentals let us figure out what is Engg RnD and how this is differentiated from conventional IT businesses.Compared to IT service business it is a sticky business involves IP rights/patents etc.IT business focus cost savings whiles ERD creates revenue stream and operational cost savings.Key sectors using ERD verticals are Aero , Auto , Telecom , Defence etc.

Engineering RnD segment as a sector

100 bn USD is globally spent on outsourced ERnD. India account for 30 Bn USD business, unlike other IT segments china is the market leader here.Currently tailwinds are favouring indian companies due to multiple factors like

Growing RnD spent due to digitalisation / Electric vehicles / Automation / innovations / adoption of IOT (internet of the things) / Artificial intelligence etc.

# IP protection and trust factor favourable for indian companies

# A growing manufacturing base in india

# Large pool of engg talent

# Changing to Innovation mindset / Startup eco system

Some of the large companies who are spending big money for Engg RnD outsources are GE , Samsung , Cisco, Intel , Benz , Airbus , Boeing , Bosch and Volvo.

Major indian players are HCL technology, Cyient ltd , LTTS etc.

ASM Tech is a small kid in terms of revenue and scale of operations.

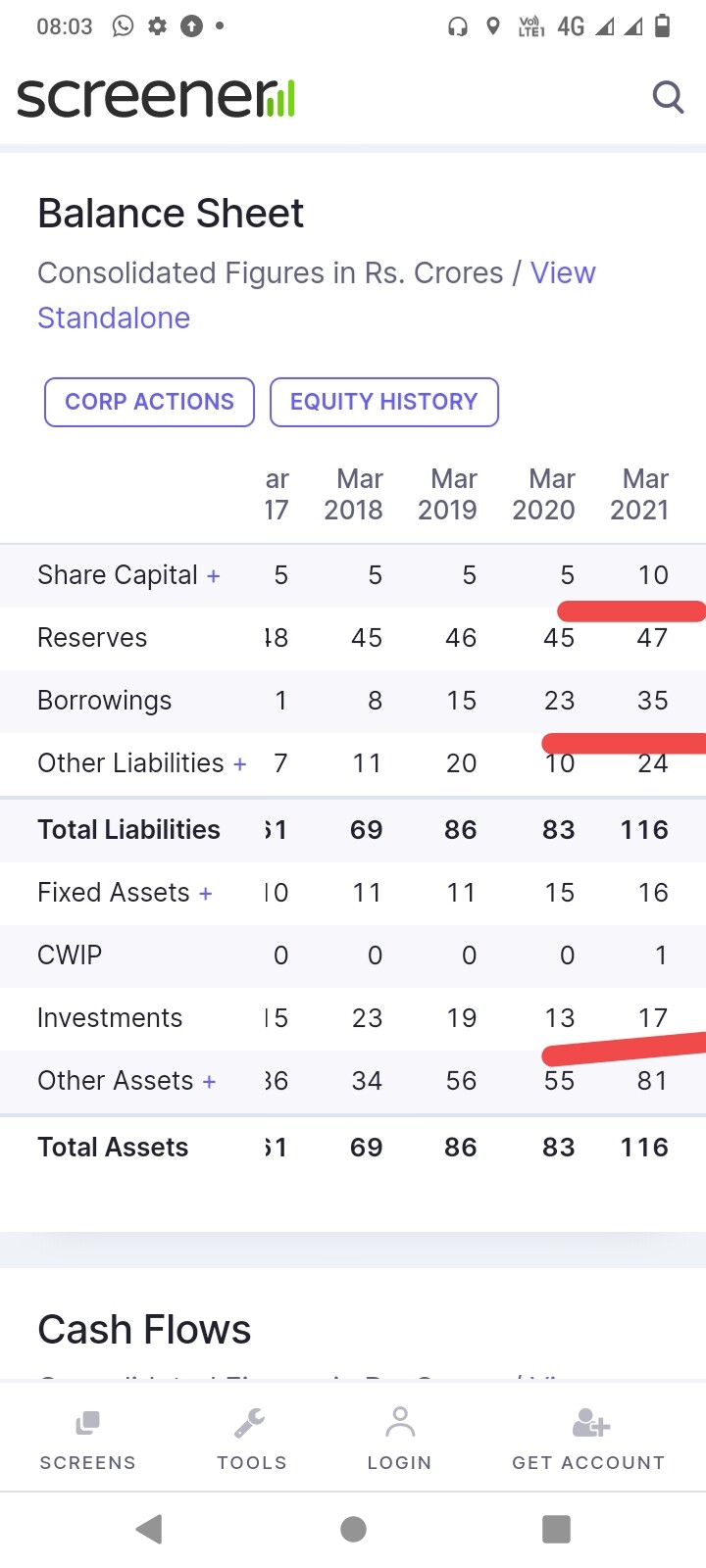

CMP : 160

Marketcap : 80 cr

TTM Revenue : 107 cr

TTM PAT : 10 cr

PE : 8

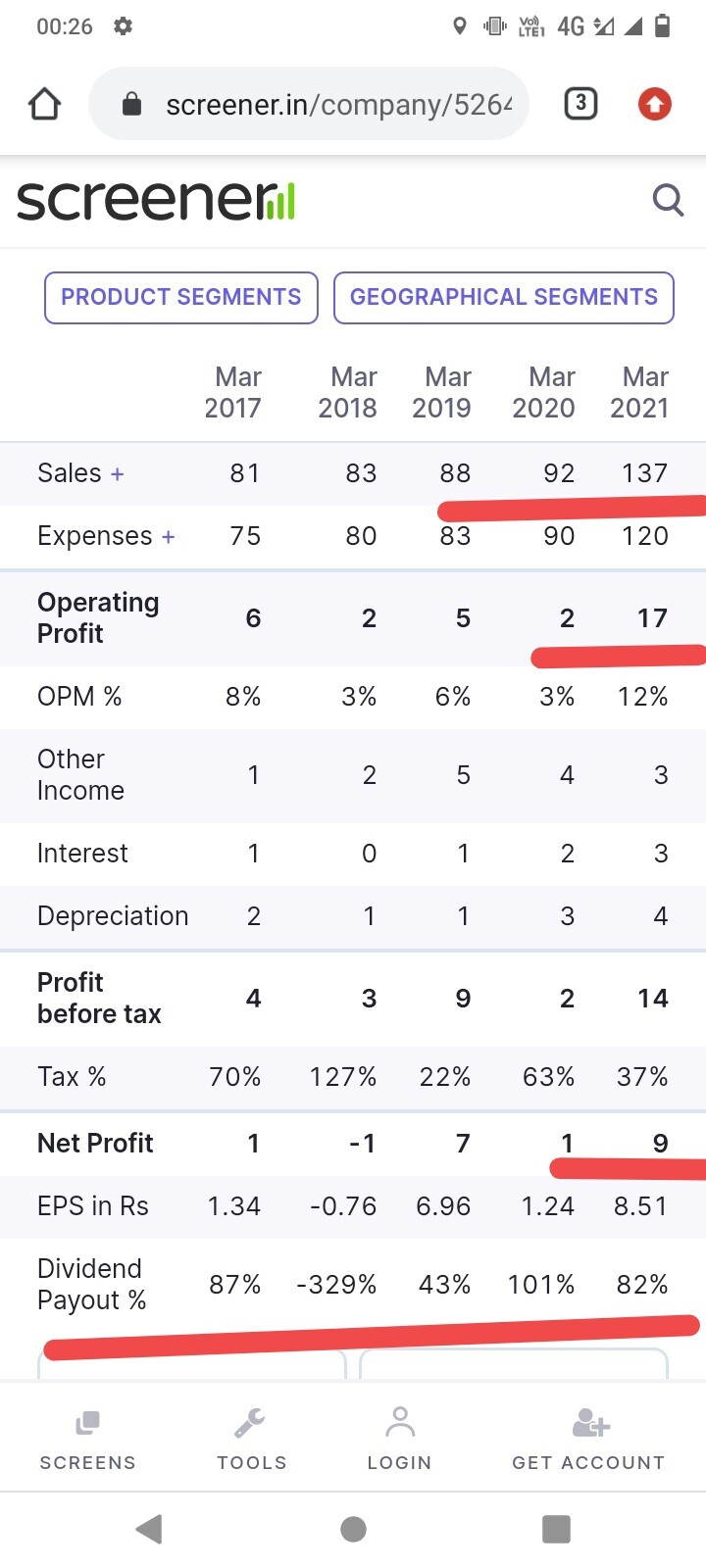

H1 revenue growth is around 35% yoy , there are not much public available informations to understand the reason behind this revenue growth.But if we carefully go through the credit rating reports available at screener.They clearly states about new orders in company hand also telling FY 20 poor profit figures majorly due to the unproductive days bcz of employee trainings for new orders received.

ASM credit rating report ICRA - Aug 2020

"Revival of margins over last few quarters, healthy order book and new product profile augur well for FY2021 - ASM’s profit booking has Revival of margins over last few quarters, healthy order book and new product profile augur well for FY2021 - ASM’s profit booking has depicted a lumpy trend in FY2020 due to higher employee expenses during the Q2FY2020 and Q3FY2020 due to employees being trained for an order received by the company. Order book from key clients continues to remain healthy with an addition of orders from new customers in Q1FY2021 augur well for the company. The q-o-q revenues and operating margins improved from Rs. 22.34 crore and -3.8% in Q3 FY2020 to Rs 26.1 crore and 20% in Q4FY2020 which it has maintained in Q1FY2021 due to healthy order execution.depicted a lumpy trend in FY2020 due to higher employee expenses during the Q2FY2020 and Q3FY2020 due to employees being trained for an order received by the company. Order book from key clients continues to remain healthy with an addition of orders from new customers in Q1FY2021 augur well for the company. The q-o-q

revenues and operating margins improved from Rs. 22.34 crore and -3.8% in Q3 FY2020 to Rs 26.1 crore and 20% in Q4FY2020 which it has maintained in Q1FY2021 due to healthy order execution "

80% of the revenue comes from top 3 clients.

- Applied materials (Leader in semiconductor industry)

- Infloblox (Cyber security and cloud company)

- Ruckus wireless (wireless LAN device manufacturer)

So basically this is a microcap illiquid company available at cheap valuations due to small scale of operations and high client concentration risks.

Nothing wrong with current valuations company have not done much in last 30 years of existance.Am not trying to figure out this is a cigar butt trade or not rather am looking at a long term view on this company on following factors and why i believe the company is in cross roads.

Promoter pedigree

Optionalities infront of the company

I will try to discuss one by one in coming days.

I also request the fellow boarders to study on the company and do some research and share your feedbacks.