Transporters are on the verge of surrendering 50,000 vehicles to financiers, after being hit by sluggish economic activity, low freight availability, and end of the moratorium on August 31. This is based on the estimates of the Indian Foundation of Transport Research & Training (IFTRT), a New Delhi-based think-tank.

2 Likes

Posting relevant sections :

Ashok Leyland has launched Bada Dost, a single cab, light truck developed on a completely new platform to take on the segment leader Mahindra Bolero pick-up.

The new vehicle will address a near-white space in the light commercial vehicle (LCV) segment dominated by Mahindra & Mahindra.

It will be the first Ashok Leyland product addressing the LCV segment developed on its own platform. The Chennai-based CV maker invested Rs 350 crore into the product and began work on it in 2017. The Bada Dost will be sold through 570 touch points of the company.

Speaking to Moneycontrol, Nitin Seth, Chief Operating Officer, Ashok Leyland, said: “In the LCV segment, we enjoy only 34 percent of the market. Obviously, your market share cannot go beyond 18 percent if you have a limited product portfolio. With the launch of the Bada Dost, our addressable market goes up to 65 percent in 2-3 years”.

Ashok Leyland, with the Dost, dislodged Tata Motors in FY21 in the same segment, with a share of 18 percent. At 15 percent, Tata Motors market share slipped the most despite products like the Super Ace and Yodha.

As per Ashok Leyland’s predictions, the sub 7.5-tonne (goods + passenger) segment is expected to increase to 6.55 lakh units a year by FY25 after closing the current year (FY21) at 3.91 lakh.

Ashok Leyland has designed the Bada Dost to accommodate the left- hand drive (LHD) option, allowing it to address markets outside India, too. About 80 percent of the world market is left-hand driven. The Bada Dost will be exported to markets like Africa, SAARC, Gulf countries and ASEAN.

As of FY20, less than 4 percent of Ashok Leyland’s production was exported at 1,570 units from the LCV segment. Though Seth did not provide details of the company’s aspirations, he did not rule out the possibility of the Bada Dost clocking more sales outside of India than within the domestic market.

Disclosure : Tracking,not invested.

6 Likes

Updates for Ashok Leyland, pure long term CV play:

Nomura believes Ashok Leyland will benefit more due to higher share in tonnage trucks; new LCV (Light commercial vehicles) range an added upside to the company. MHCV (Medium and Heavy commercial vehicles) volumes would reach their FY19 peak levels by FY25. For MHCVs over FY21 - 23, Nomura have factored in -33%/ +47% / +38% growth in volumes.

Credit Suisse (CS) highlights near term concerns on the timing of CV (Commercial Vehicles) cycle are now being resolved, with strong freight demand in September and seasonality supportive of sequential improvement over the next six months. Additionally, collection efficiency of CV loans has shaped up well in Sep and there is low likelihood of material repossession.

As per Axis Securities, AL is scaling up its non-truck businesses to mitigate the impact of business cyclicality and earnings volatility. These businesses include spare parts, exports, LCV, defense and power solutions. AL has reiterated its focus on diversifying revenue and building a lean business model to better withstand current and future downturns. AL’s electric vehicle thrust is likely to drive most of the EV bus sales volume in the upcoming financial years.

:::: Shareholding ::::

Promoters: 51.5%

FIIs: 15.7%

DIIs: 14%

:::: FULL STORY LINKS ::::

There’s a lot in Indian media that’s just outright junk. I work in 3PL industry and from my limited visibility - currently transporters are actually doing quite well because rates have spiked and this Diwali season is looking good. Diesel increase has been passed to customers and drivers that had gone away are returning

The only thing that’s a concern still is the financing which would also settle by Q4

2 Likes

KR Choksey on Ashok Leyland going forward:

The company is focusing on a cost reduction plan under the Project ‘Reset’ which will reduce overall cost structure and improve efficiency. The management stated that the company achieved cost saving of Rs 540 crore in FY20 due to efficient cost management. KR Choksey expects new platforms to reduce the production cost and overall overheads. The capex of all the major projects is almost over and capex for FY21 is expected at Rs 550-600 crore mainly towards maintenance and for small projects. The brokerage recommends traders to buy the stock with a target price of Rs 86.

Hi!

Does anyone know what is the split between Defense contracts and other commercial contracts?

Is there any way to verify it?

Secondly, which OEM partners does AL have. Are there any auto ancs (listed) that are a supplier to AL.

1 Like

Sharekhan gives 38% upside from current levels, Target: INR 131

12/05/20

ICRA: Ashok Leyland Limited: Ratings reaffirmed; rated amount enhanced

Ashok Leyland Limited_r_04122020 ICRA.pdf (349.2 KB)

READ ONLINE: https://www.icra.in/Rationale/ShowRationaleReport/?Id=99775

UPDATE - Zee Business Report - December 22, 2020: JM Financial conducted checks with Ashok Leyland dealers to gauge the market response of the recently launched Bada Dost LCV. JM Financial rolled forward to Mar’22 and increased the target price to Rs 120 (from Rs 100 earlier) based on 18x PE for standalone and Rs 7 contribution from Hinduja Leyland Finance (1x FY23 BV and 30% holding company discount). The new 3ton+ LCV has received positive customer response driven by benefits such as better mileage, superior pick-up and lower service cost vs. peers. The increase in addressable market and product acceptability should aid the company to gain market share in the LCV segment. Additionally, macroeconomic indicators such as e-way bill generation, IIP growth and manufacturing PMI are showing healthy signs of recovery in the past three months.

Ashok Leyland MHCV volumes are recovering in tandem with the economic recovery, while LCV volumes are already recording YoY growth.

JM Financial expect Ashok Leyland to benefit from:

a) increased addressable market with introduction of the Phoenix platform

b) modular platform for MHCVs

c) start of 3-5 years of MHCV up-cycle

d) increased focus in export market

Ashok Leyland estimates revenue/volume/EBITDA CAGR (over FY20-23E) of 15%/10%/39%, driven by a sales up-cycle and margin expansion. Delay in volume recovery, increase in competitive intensity are the key downside risks, while implementation of scrappage policy is an upside risk.

Prior to the onset of the Covid-19 crisis, the stock price for Ashok Leyland has witnessed a steady decline since early 2018. And, in parallel to that, the quarterly GDP growth rate of India has also followed a similar declining pattern. This suggests that prior to the Covid-19 breakout, India’s own cyclical slowdown was already in existence. The following two charts should help us to establish that correlation wherein the stock price fall for Ashok Leyland has coincided with the trend of fall in the GDP growth :

The Covid-19 outbreak has caused a debilitating effect on all sectors of the economy, the auto sector being one of the most affected. And with the second wave of Covid-19 infections setting in, the reality is that we can hardly establish with precision that when this pandemic will end once for all & when the economic activity in India would normalize. Gone are the days when we could easily say that India’s GDP is in a secular growth trend for a long time ahead and so is the future of the commercial vehicle industry.

Ashok Leyland, being a CV player, is prone to Cyclicality and thus needs to be looked upon with caution when it comes to investing in it. So from a retail investor’s point of view, under such uncertain circumstances, the wisest thing would be to give utmost preference to the Safety Analysis of the company ahead of its growth potential. Because in such unprecedented times the companies with better safety metrics would not only survive in the economic disruptions but also would recover from it rather quickly and relatively less unscathed so as not to hamper its future growth prospects substantially.

In that context, it becomes very necessary to have a look at some of the important safety metrics of Ashok Leyland Limited:

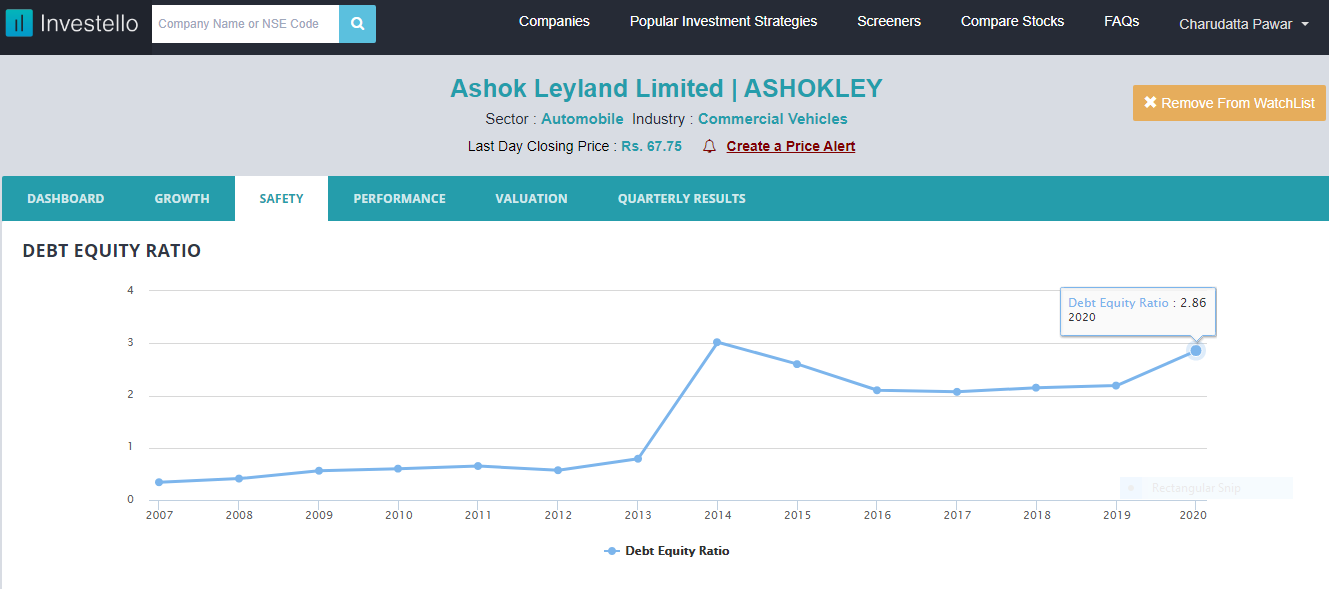

Debt-equity-ratio:

The following chart shows the debt-to-equity ratio of Ashok Leyland Limited for the last 13 years. And as one can see, in the later part of these 13 years the debt-to-equity ratio of the company has been in the range of 2 to 3 which is quite high. Moreover, it has spiked to 2.86 in the latest year.

A debt-to-equity ratio in excess of 1.0 indicates that the company has high debt in comparison to its net worth and anything beyond that value should be seen as a point of concern as it will put pressure on the future earnings of the company as a result of the additional interest expense. From that viewpoint debt-to-equity ratio for Ashok Leyland has increased to a dangerous level in the last few years and thus presents a red flag for the company. So one should analyze thoroughly that where the company is using its funds obtained from debt and whether it is capable to pay off this debt in the next few years.

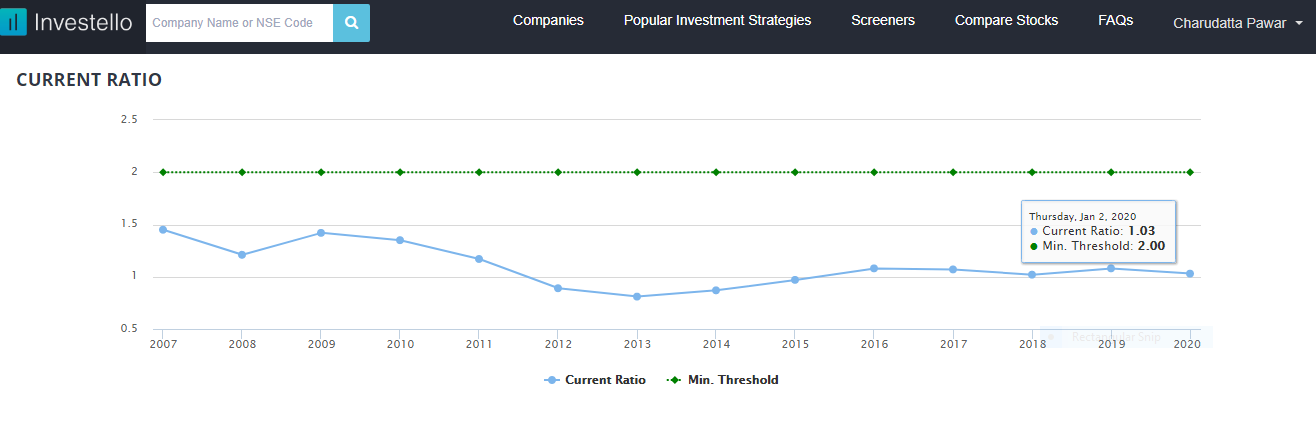

Current Ratio:

The current ratio denotes the operating financial health of the company and measures the capacity of the company to pay off its immediate liabilities with the immediately liquefiable assets. The commonly acceptable current ratio is 2. For Ashok Leyland the current ratio over the last thirteen years is captured in the following chart:

As we can see current ratio for Ashok Leyland in the last thirteen years was far from impressive, the latest value being at a mere 1.03. It was never above the safe value threshold of 2.0 in the entire time span mentioned in the chart. This is not a good sign and raises the question about the efficiency of a company’s operating cycle or its ability to turn its products into cash.

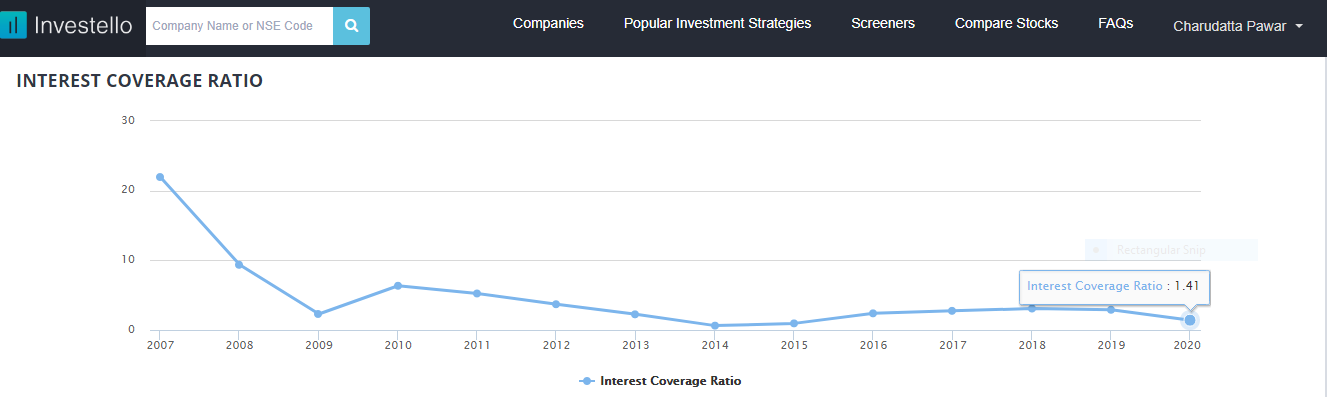

Interest Coverage Ratio :

It is a measure of the number of times a company could make the interest payments on its debt with its EBIT. It determines how easily a company can pay interest expenses on outstanding debt:

In order to ensure the safety of the investment, one should try to refrain from investing in companies that have a interest coverage ratio of less than 2.5. But as we can see from the above chart, the interest coverage ratio for Ashok Leyland has been hovering around 3.0 but in the last few years and in the latest year its value is quite low at 1.41. This is not a good sign because when a company’s interest coverage ratio is only 1.5 or lower, it raises the questions about its ability to meet interest expenses & indicates the difficulties faced by the company in generating enough earnings from its operations for the same.

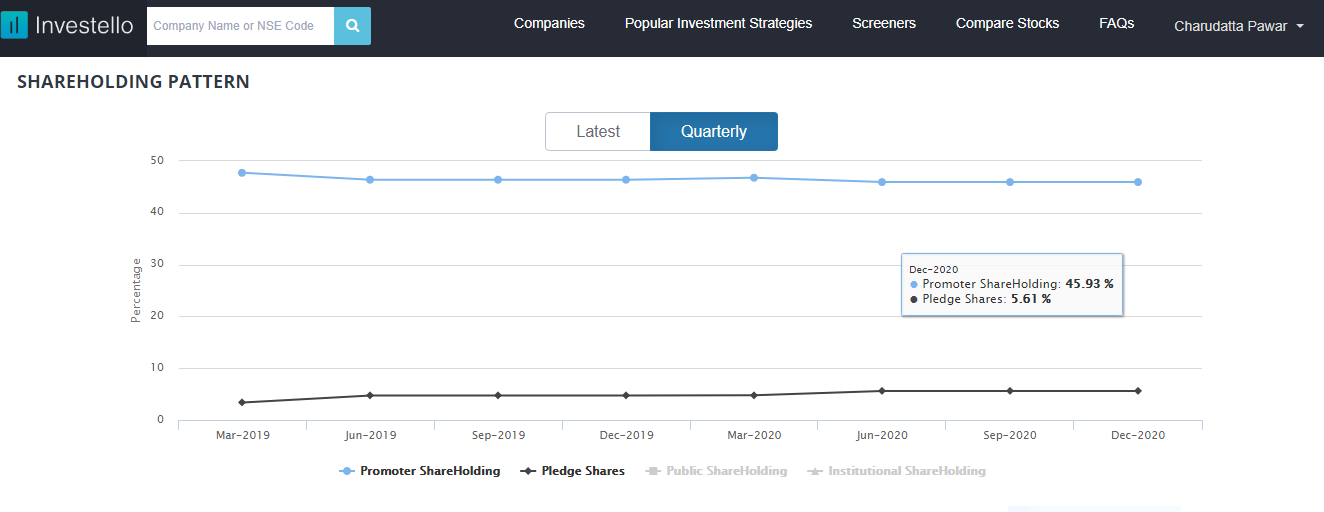

Pledged Shares:

From a Safety perspective, it is equally important to have a check on the amount of shares pledged by the promoters. The following chart depicts the pattern for the amount of pledged shares by Ashok Leyland promoters in the last eight quarters:

From the above chart, we can see that percentage of pledged shares by promoters of Ashok Leyland has significantly increased from 3.4% to 5.61% in the last eight quarters. This doesn’t sound good because pledging of shares is usually the last option for the promoters to raise funds. It is comparatively safer to raise funds through equity or debt for the promoters. However, if the promoters are looking forward to pledging their shares, then it means that the other options of raising funds have been vanishing owing to the weakened fundamentals. So this is also a concern point from the investor’s perspective.

After going through the above Safety Analysis, we can see that on the fundamental front, Ashok Leyland has performed poorly in the last few years with the above-mentioned safety parameters getting deteriorated or parted away with minimum safety levels ( i.e. Higher debt-equity ratio, lower current ratio & interest coverage ratio and a considerable increase in the amount of pledged shares). Given the current unprecedented situation (a confluence of a cyclical downturn & economic activity disruption by the pandemic), these parameters should have been at the optimum safe levels to withstand as well as to recover from the crisis and to ensure resilient recovery in earnings. But that not being the case, the stability in financial profile seems to be in the doldrums. Though there are few green shoots of recovery in recent times. But, from the point of view of long-term investing, it would be rather wise to wait and watch from side-lines unless there is a visible recovery in the demand scenario and the company is able to restore the safe levels of the above-mentioned safety parameters.

8 Likes

Due to reckless and incompetent governance, COVID19 has slowed things down again, effect of which is being observed on cyclicals too. However, if and when we overcome the situation, auto rally will continue its upward journey and CV pureplay Ashok Leyland will benefit. Keep it simple, over-analysis is useless.

1 Like

From Reliance securities report

What We Heard – Conference Call - Key Takeaways:

-

Quarterly Performance: The company gained market share in M&HCV truck segment and reached to the level of 28.9% in 4QFY21 (up 80bps QoQ and 130bps YoY) backed by successful launch of AVTR range. Quarterly LCV volume increased by 7% QoQ and 112% YoY due to launch of Bada Dost. During the quarter, the company manufactured 26,596 M&HCVs as against 17,911 units in 3QFY21 with an inventory of 3,448 units in 4QFY21 as against 3,171 units in 3QFY21. Working capital for the quarter stood at negative Rs1.3bn vs. negative Rs5.2bn in 3QFY21. The company hiked the prices in 3QFY21 (by ~1.5%) and 4QFY21 (by ~2%) to partially offset the higher RM cost.

-

International Markets: The company added ~6-7 major distributors in Africa and Middle East. With the launch of ‘Gazelle’ and ‘Falcon’ in Saudi Arabia, the company achieved signif i cant growth on the exports front. It aims to record healthy growth in these markets, going forward.

-

Capex & Debt: AL incurred Rs6.2bn capex in FY21 (vs. Rs12.9bn in FY20) mainly towards modular business programme (AVTR), ‘Bada Dost’ programme and EVs. It has earmarked Rs7.5bn capex for FY22E. In FY21, the company invested Rs3.7bn in subsidiaries (vs.

Rs4.5bn in FY20) and plans to invest Rs2-2.5bn in FY22E. Net debt stood at Rs26.1bn as on 31st Mar’21 gearing at 0.37x vs. Rs.20bn as on 31st Mar’20 gearing at 0.28x and Rs.28bn as on 30th Dec’20 gearing at 0.43x. -

Hinduja Leyland Finance: As per the management, the company is doing extremely well with no liquidity issue and a collection eff i ciency of >90%. Gross and net NPA for the quarter stood at ~4% and ~2%, respectively. The company has an RoE of 11.6% and a cumulative provisioning of >Rs2bn.

-

New Launches: While AL launched its modular vehicle platform AVTR in Jun’20, its next gen LCV platform called ‘Bada Dost’ along with ‘Boss LE & LX version’ (ICV segment) was launched in 2QFY21. All these products received positive response from its customers, which increased its topline in 4QFY21.

5 Likes

Interest rates are at historic lows worldwide and might remain so for some more time, India is following the suit and interest rates should go down further in coming months/years. Growth/Market share at the cost of rising debt might turn out to be a good thing as interest payout remains stagnant or reduces further in future.

In case interest rate cycle reverses then lot of equations will change for a lot of sectors and companies.

Summary of the article - trunk rentals have increased over oct-dec and Improved utilization, robust rentals, the waning effect of higher axle load norms on higher tonnage commercial vehicles and aging of fleet, with scrappage policy inching towards implementation, are all coming together as strong tailwinds for CV segment.

7 Likes

This stock popped-up when I ran screener on improving Q-o-Q NP stocks…

Had lost all hope in CV stocks having burnt in 2018 meltdown…

Q4FY22e showed good improvement both on QoQ and YoY basis with one-time losses the spoiler. If the trend continues this may be a stock to watch in the bear market…

PS: Haven’t studied the stock in detail like high leverage etc… this is an ad-hoc assessment

Really amazed (shocked) by the ignorance on Ashok Leyland on this forum. It reminds me of the narrowed down and limited view of L&T a few years back when us contrarians were piling it. Nevermind, the more you ignore, the more for us to accumulate, as it has been all these years. ![]()

1 Like

Ashok Leyland’s volume is expected to grow 15-20% in FY23. They gained market share in the truck segment (32.3% in Q2 FY23 vs 22.2% in Q2 FY22). The demand pick-up in LCV segment (expected to grow by 30-35% in FY23) is strong, driven by e-commerce & opening up of schools & colleges. The company is also focusing on EVs & them to form a large part of business in the coming years.

1 Like