I think Ashok Leyland Ltd. (ALL) deserves a separate thread on this esteemed forum. In the below note, I have summarised whatever information I can obtain (and whatever variables are worth tracking from the perspective of an investor) from the sources in public domain (the numeracy of which is an advantage in case of a large cap company!).

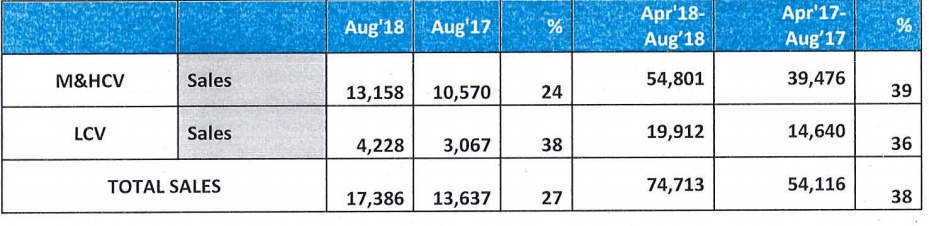

Looking at the past 5 quarter performance of ALL, the following picture emerges:

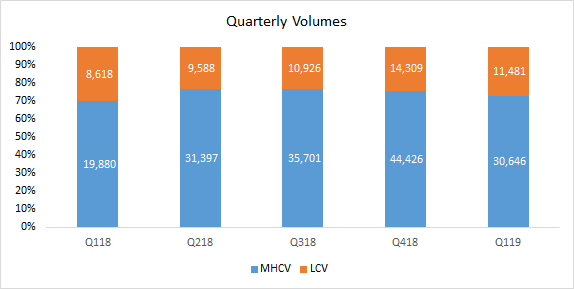

ALL is a reliant on medium & heavy commercial vehicles, which make up for ~70% of quarterly volumes:

Q4 of 2018 was exceptional in terms of volumes because of (as per mgmt comments) strong GDP growth, pickup in investment, mining, road building and construction activity in Rajasthan and UP along with rated load legislation/overloading ban. (GST, ban on overloading to lift heavy vehicle sales, says Ashok Leyland- The New Indian Express)

Things I like about ALL:

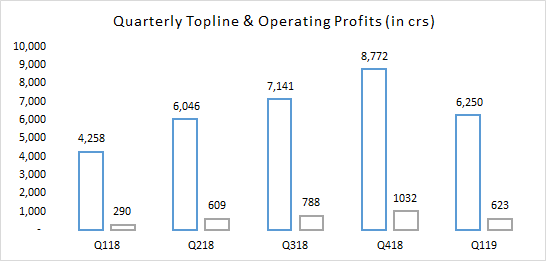

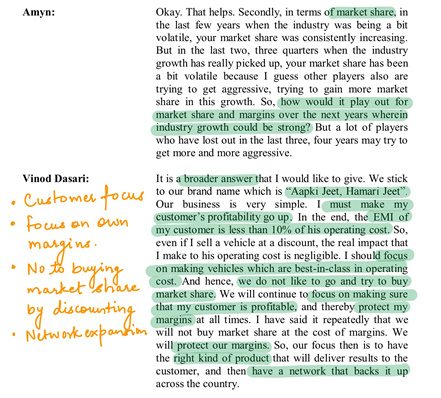

- Mgmt wants customer profitability first and wants to keep its margins intact by focusing on reducing operating cost/total cost of ownership of its CVs rather than initial purchase price. This is clearly visible from the financials as well (10%+ OPM in consecutive quarters). Refer below extract from Q4 concall:

In fact, ALL has increased its market share from 22% to 33% in the last 5 years. It’s dominant in the Southern parts and is gaining share in North, East, West & Central as well.

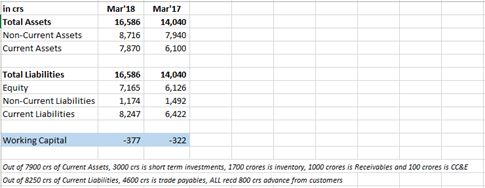

- ALL has reduced debt significantly and has strong cash flows as well (Cash from operations was 5400 crs driven by higher trade payables (ALL doing business with cash from its suppliers!) by 1500 crs. ALL also has 800 crs advance from customers on the BS. (I have a bias for companies with this kind of working capital management).

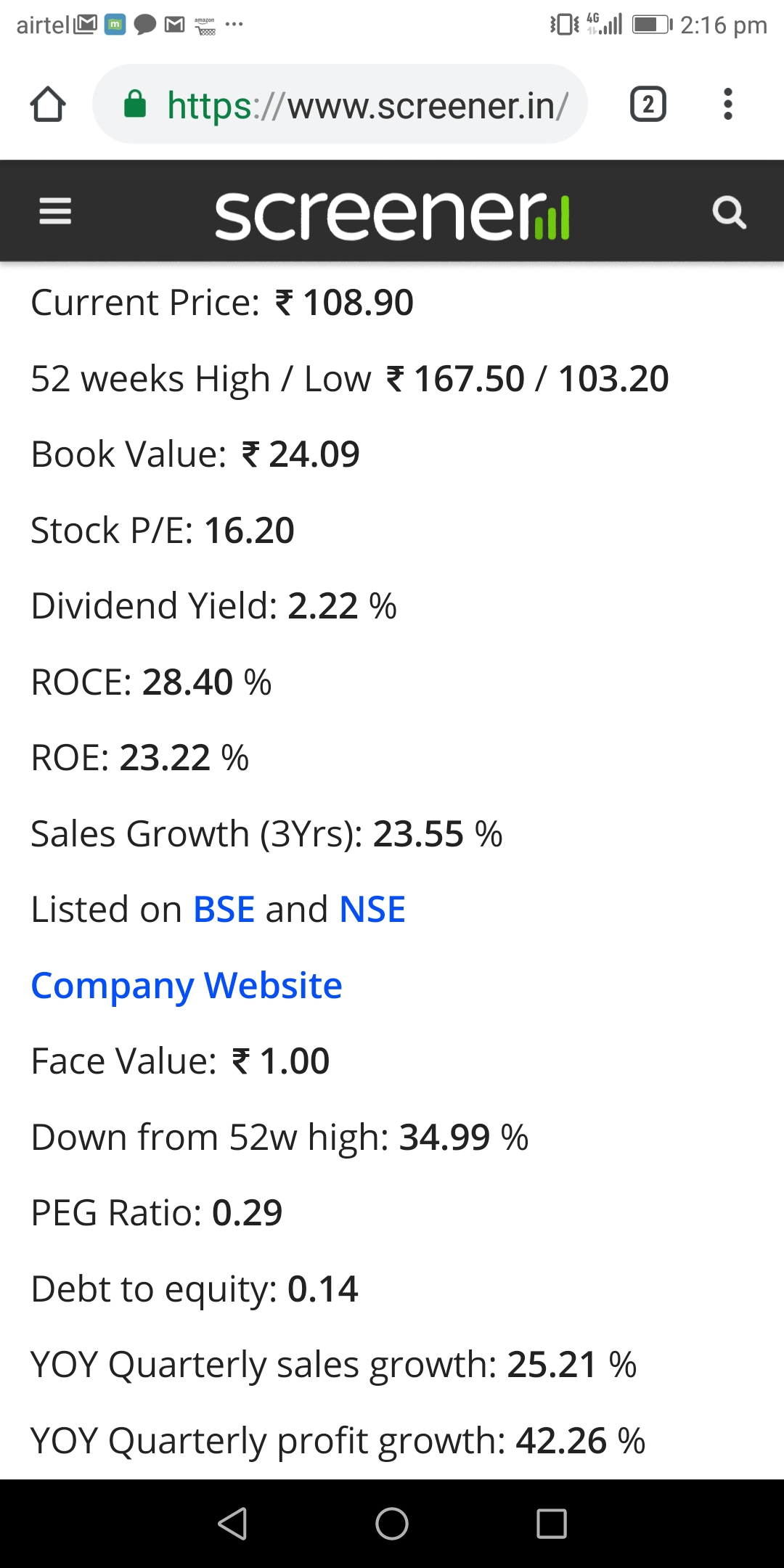

If we look at the Balance Sheet as of FY2018, the following picture emerges:

And the interest cost has come down:

-

Management is of high quality and with a strong pedigree (Hinduja Group). High promoter holding at 51%.

-

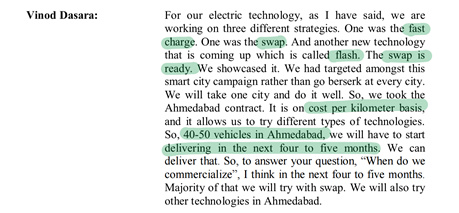

Electric buses is an area where ALL is planning a lot of things. Refer the following comment from ALL MD in the concall:

Steps ALL is taking to reduce impact of cyclicality of CV business on its financials:

-

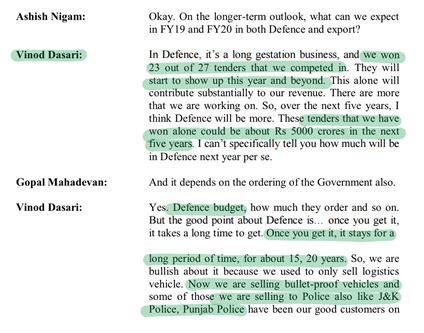

Getting deeper into defence procurement business – ALL won 25 tenders in the last 2 years and are going for more. Growth of 30% YoY in FY18 albeit making just 3% of Gross revenues. Though this business segment is a long gestation, it stays for 15-20 years once entered. (Read comments in screenshot) (https://economictimes.indiatimes.com/news/defence/ashok-leyland-looking-at-rs-5100-crore-revenue-from-defence-orders/articleshow/63815004.cms)

-

Expanding after-market solutions/services, spare parts offerings, network. 5% of Gross Revenues in FY18.

-

Expanding into more and more international markets. Growth of 36% YoY in FY18. (Recently they inaugurated Ivory Coast office to serve West Africa: Ashok Leyland makes Ivory Coast a hub for West Africa - The Hindu BusinessLine).

-

LCV business - grew by 37% YoY in FY18.

Key risks to the business:

-

Impact of cyclicality is still a concern. The business is based on primary economic activity, factors like GDP growth, mining, construction, roads & highways. Timing the entry and more importantly exit is important. Though India currently is a secular growth story (can’t see a sharp downturn on the horizon). Mgmt has also indicated the steps it is taking to reduce cyclicality impact (highlighted above).

-

Axle load norms recently announced allow higher loading by 20-25% thus allowing truckers to ship more on their existing trucks. (Whether this rule is applicable retrospectively or prospectively is still unclear: ashok leyland: Axle load norms may create short term impact but will reset in August: Gopal Mahadevan, Ashok Leyland - The Economic Times). Mgmt says overloading already happens and what this rule will do is bring unwarranted overloading to warranted overloading with strict implementation. And if this increases the extent of overloading further, it could impact safety of the vehicle.

-

High competitive intensity with players like Tata Motors, Eicher, Mahindra and Bharat Benz. Ultimately discounting price to win market share by competitors will force ALL to follow to some extent as well just to maintain market share. This will put a pressure volumes.

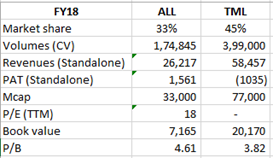

For comparison, look at the TMT numbers vis a vis ALL:

Note that in the above, Revenues and PAT for TML is PV+CV segments. If anybody can find out segmented financials for TML (CV, PV separately), please share!

- Raw material costs (which make up for ~70% of direct costs) dependent on commodity primarily steel which is in an upcycle. Mgmt has indicated it regularly raises prices to offset that impact but in a highly competitive environment, pricing power might be limited thus impacting margins.

Factors expected to drive demand in the coming years:

-

Hub & spoke model: Mgmt expects GST to encourage faster adoption of Hub and spoke model in the logistics sector which will drive demand. This demand will be for larger trucks resulting in higher avg sales realization. This is expected to improve demand for products like Dost (LCV) as well.

-

Cash for clunkers scheme: Govt is coming up with a scheme for old truck owners to exchange polluting trucks with new ones and avail a discount on the same to be funded by the govt. (https://timesofindia.indiatimes.com/business/india-business/cash-for-clunkers-set-to-hike-demand-for-trucks/articleshow/63372417.cms).

-

BS VI transition: Volume growth due to pre buy before BS6 kicks in expected in April 2020 as per mgmt. Also, ALL is readying a product portfolio expansion in the 2 tonne to 7 tonne LCVs for 2020 which will be ready with BS VI technology thus plugging gaps in product offerings.

ALL has planned capex of 1000 crores in small plants (not brownfield plants) and new product development for FY19 expecting strong demand in the coming couple of years: (Ashok Leyland plans ₹1,000-cr capex for FY19 - The Hindu BusinessLine)

I am sure there is a lot more to be discussed about this company and I would invite fellow VP members to share their perspective.

Disclosure: Invested recently after a sharp correction & will add more on clarity about axle load norms. ALL might correct more though valuations look comfortable at 18 times trailing 12 months earnings