Bringing in Orry for Flying machine could prove to the be midas touch. FM has had it tough times coz of competition in that sub segment. But its a mature category and influencers like Orry look to be the right move.

1 Like

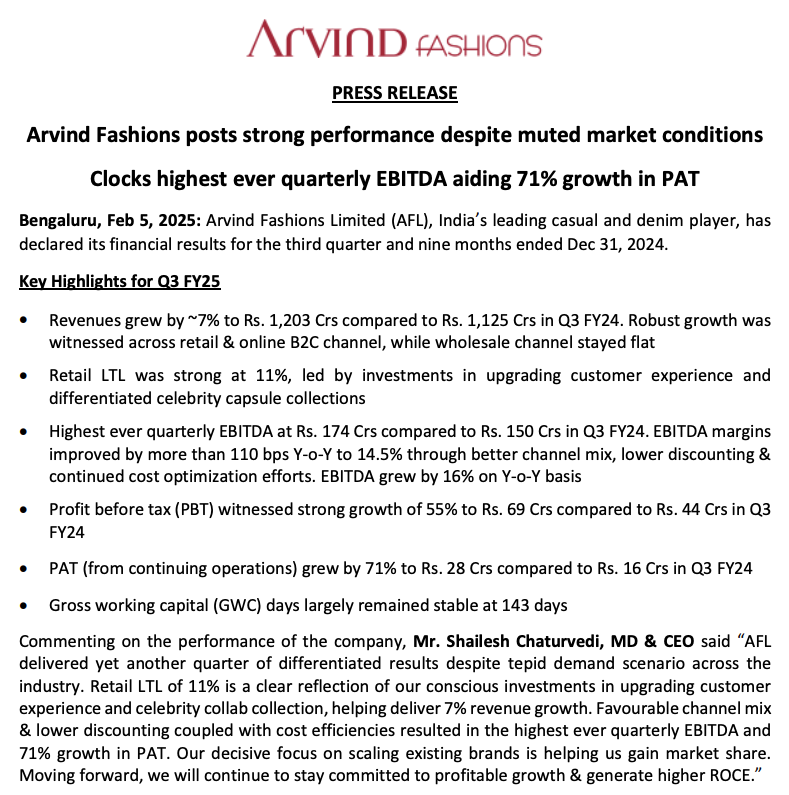

Arvind Fashions Ltd Accelerates Growth: 34 New Outlets and Record Revenues!

- If the aging of inventory and the share of freshness in the business are observed, they are at healthy levels. This is one of the reasons for gross profit to increase, because the company has high freshness and they don’t need to discount and their sellthroughs are good across channels.

Conference Call Takeaways

- Retail sales experienced a solid 15% YoY growth, with like-to-like (LTL) sales expanding by 11% across all brands.

- The company remains bullish on future growth, supported by new product launches.

- Winter portfolio sales were strong, with a higher proportion of full-price sales.

- The online segment has surpassed pre-pandemic levels, with the direct-to-consumer (B2C) channel growing 20% YoY. Going forward, online growth is expected at 10% annually.

- The online business, which previously leaned toward B2B, has now shifted towards B2C, projected to contribute two-thirds of the total online revenue.

- Wholesale channels have a potential growth rate of 8%-10%, though a major store closure had a slight impact.

- Multi-brand outlets (MBOs) are also positioned for 8%-10% medium-term growth.

- Arrow and Flying Machine delivered strong double-digit LTL growth, with expansion planned through multiple retail formats, including exclusive stores and departmental chains.

- Margins are expected to improve by 100 bps annually, with Arrow and Flying Machine anticipated to see even stronger gains due to better cost efficiencies.

- Retail footprint is set to expand by 15% each year.

- US Polo and Tommy Hilfiger footwear sales dipped due to regulatory restrictions on imports.

- Women’s wear showed exceptional performance, doubling revenue during the quarter.

- Adjacent categories—including kids wear, footwear, women’s wear, and innerwear—now contribute 20% of total sales, with a stronger share from US Polo.

- The company maintains its 12%-15% annual revenue growth outlook.

This should benefit Arvind fashions too

2 Likes

2 Likes

Might be a naive question, but why tax regime change now ? Don’t think there has been any corporate tax change last year. It was a big turn off.

This was supposed to be the 1st year post disposal of all discontinued brands, and was supposed to set the baseline for future growth. But again there is an exception tax loss. With such exceptions, comparing the performance YoY is becoming increasingly difficult. This along with the fact that the most profitable part of the business is only 50% owned by the company, prompted me to sell off post the results.

1 Like

- PAT Impacted by Tax Regime Change: Exceptional DTA charge of INR 120 crore in Q4 due to shift to lower 25% tax regime. Adjusted bottom line grew >70% YoY.

3 Likes

Why the tax deduction is 36% again in q1fy26

2 Likes