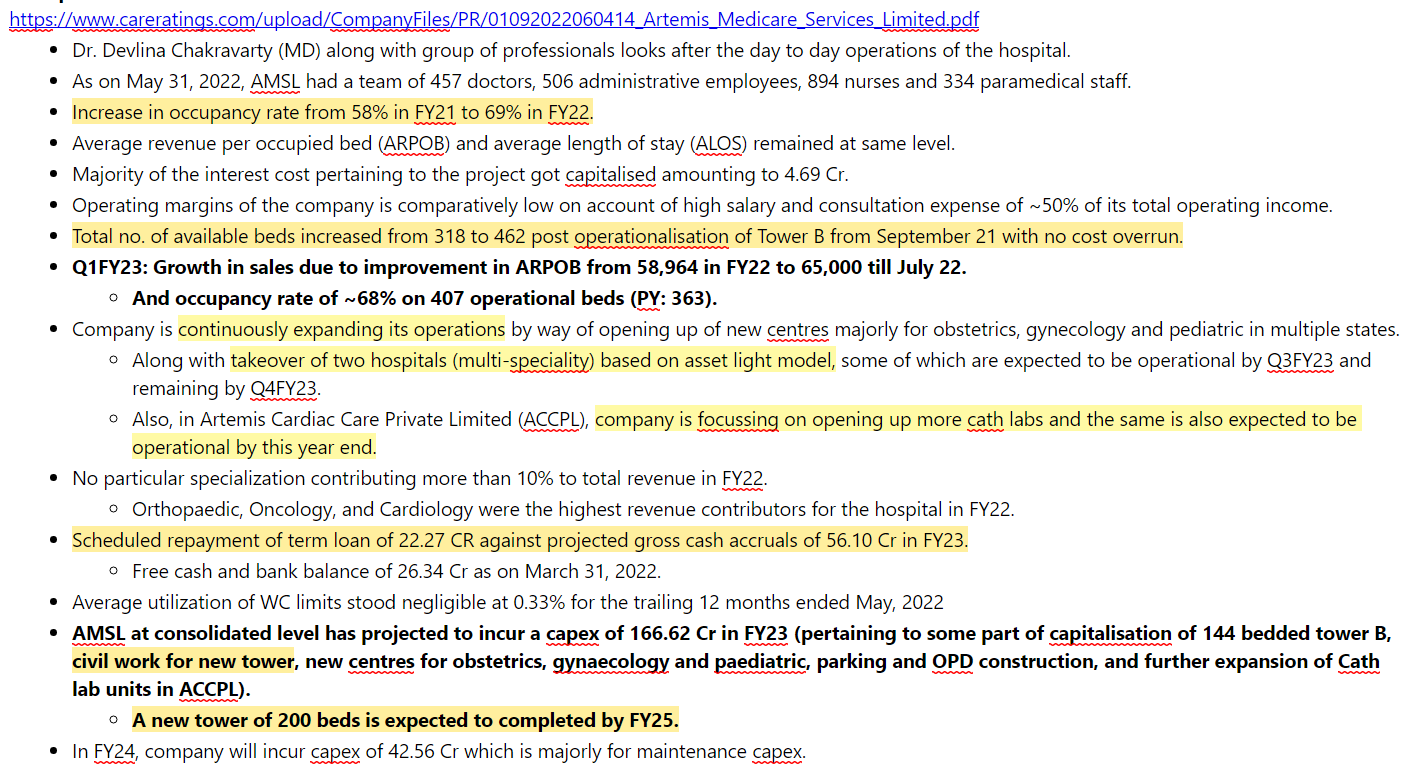

company took 168 crore expansion to add 144 bed . this is when land was already available . easily per bed replacement cost is >1.5 crore. hospital is based at prime location in gurgaon where land is available > 2 lakh/sqmtr . company is available at less than 1.25 crore/bed valuation which is cheapest in all hospital .

i am eager to see interest burden going down and opm going up which would bring interest of more smart investors in this scrip

I did attend the AGM however it was not very helpful as the discussion and participation was very limited. We wanted to send our questions but somehow missed sending them in due time.

Few points:

There was a good video about the hospital being played. It highlighted that there are many more ICUs and operation centers now, more parking and other facilities.

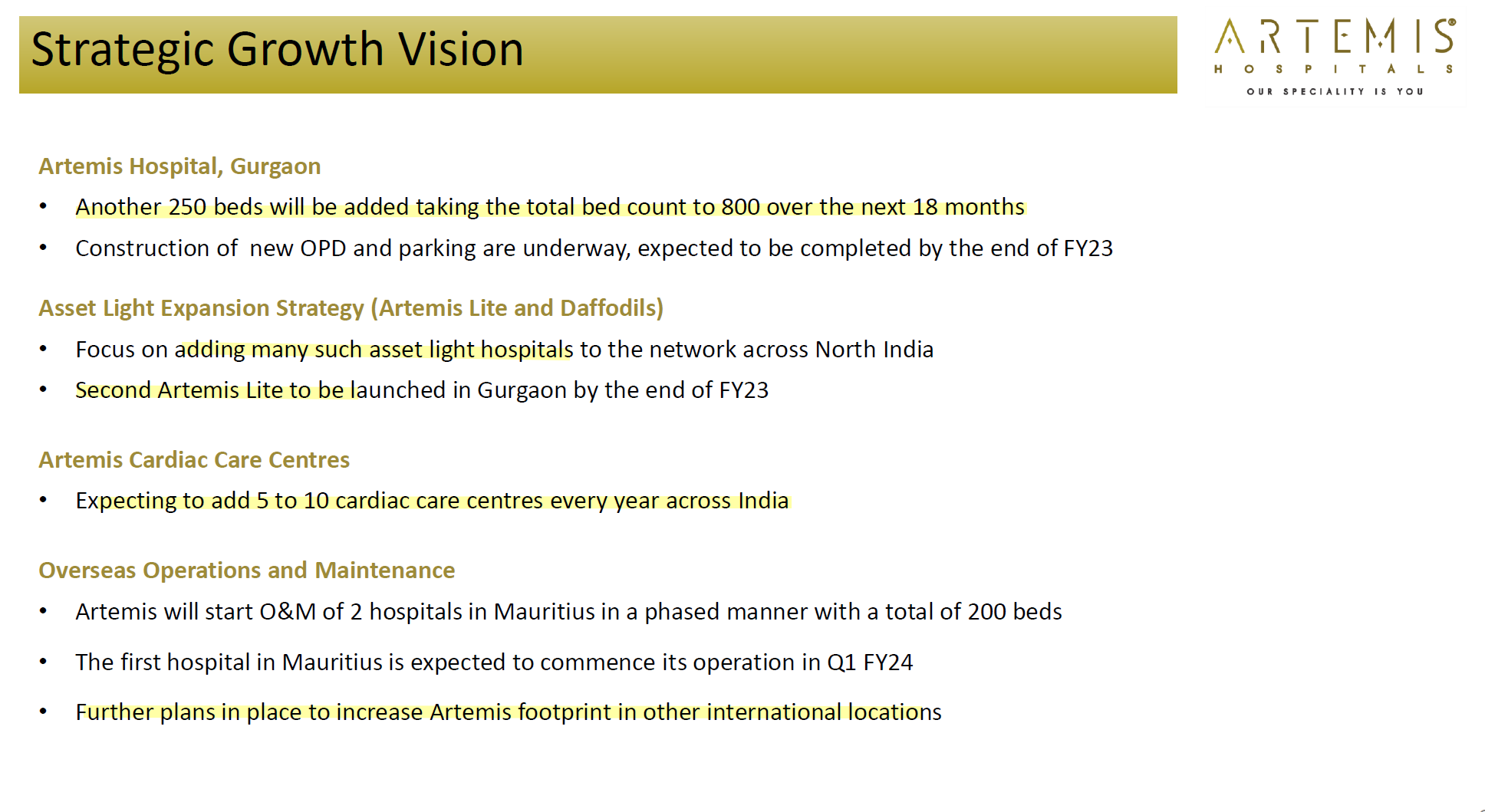

Co has recently completed the capex to expand to 540 odd beds. The chairman mentioned that we will not stop here and further expansion plans are underway

The CEO mentioned that there are multiple models underway. 1 - growing artemis at the existing location 2. asset light model wherein they will manage other hospitals and provide their expertise. 3. Luxury birthing centers by the name of daffodils.

The undertone did look positive and aggressive.

Personally, I feel it’s a very interesting story given the large brownfield expansions underway while the absolute market cap is not very high. Its not easy to build a brand name in hospital sector…Artemis has done well to become one of top 5 hospitals in NCR (esp Gurgaon). With the backing of Apollo group perhaps they can scale up a lot.

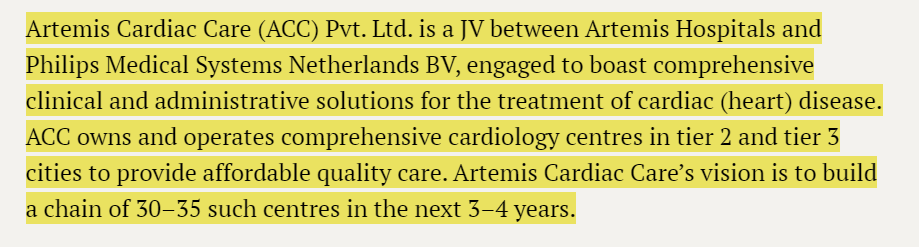

Artemis extended the healthcare services to New Delhi now. Artemis Lite, a multi-speciality hospital, offering high-end and personalized multi-specialty care. The hospital has 40+ beds including two operation theatres, 9-bed ICU, 5-bed day-care chemo suite, 4-bed NICU, labour delivery rooms and multi-specialty wards.

Disclosure : I am invested in the stock on fundamentals and added more recently. Rationale covered here Artemis Global Life Sciences - #40 by Lynch Still learning technicals/techno funda, so there might be more to this

Artemis opened new centre under the brand name, Daffodils in Jaipur.

Daffodils by Artemis is a premiere luxury birthing centre offering mother and child care services. Offering comprehensive mother and child care services, the centre will have 40 IP beds including specialised neonatal and paediatric ICUs, state-of-the-art Operation Theatres, emergency room, diagnostics and allied services.

Narayana Hrudayalaya just acquired Shiva hospital in Bangalore (in same complex as their existing hospitals) at 16-17x EV EBITDA / 4x sales.

The hospital margin profile is different from Artemis in addition to several factors in the deal such as adjacency to Narayana’s existing hospitals, but it still gives a decent level of comfort to current TTM valuations of Artemis at 13 EV EBITDA/1.4x sales.

Disclosure : Invested and biased. This is not investment advice.

Hi Ayush sir

do you see promoter as retail friendly ? being invested here. I have done scuttlebutt (i ma based at gurgaon) and have comfort of valuation. Only concern is promoter entity and words about them in market

How do you see the results. Artemis Cardiac Care , subsidiary posted losses. Also a seasoned leader and director who was driving the cardiac business moved out of Artemis to Paras after 11 years asper linkedin.

YoY 40% growth in profit before tax is encouraging. This seems they are on track of 40 crore net profit on sales of 700 crore in FY23. This net profit should give enough poweder to fuel expansions in tier 2 towns which will further bring the growth.On Mcap of 950 crore it looks valued comfortably. I will be tracking the results qoq and would be buyer on dip

mcap =1100 crore , revenue 700+ crore , profit 40 crore. while on pe and mcap/sales co looks fairly valued how ever given the growth plan , this certainly deserve a place in watchlist .continue to hold stock from much lower price position.