Background: Apollo Finvest is a listed NBFC run by Mr. Mikhil Innani. Mikhil is a 2nd gen entrepreneur who has earlier headed consumer products and growth at Hotstar and CouponDunia, which was acquired by Times Internet. Prior to working at Hotstar, Mikhil has co-founded PharmEasy, an online medicine delivery startup.

Post the acquisition of Hotstar in which he has played an active role in scaling the monthly active users from 10+ million to 300+ million, Mikhil has decided to venture on his own through family owned listed entity Apollo Finvest.

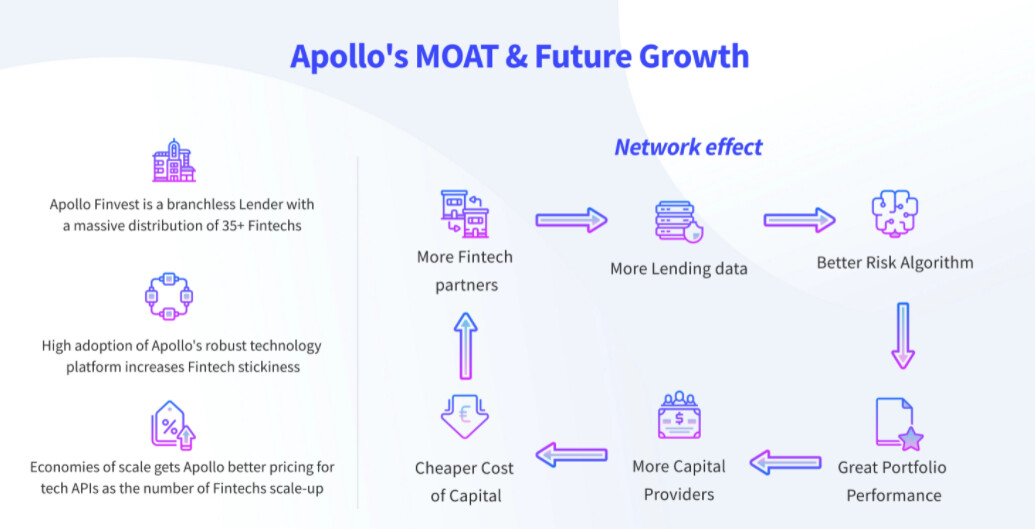

Business: Apollo Finvest essentially is a back-end platform for consumer facing digital lending startups. Digital lending companies and their unique underwriting can be onboarded into Apollo’s platform and start disbursing loans in a few hours with compliance being taken care by Apollo owing to its NBFC license.

The features currently include compliance, basic underwriting and loan management system (which itself has customized underwriting rules which can be added/modified by lenders based on their policy).

The company’s LMS product Sonic is explained in detail in this blog post

The company is currently working with 30+ fintechs who use Apollo’s platform to provide several products including consumer loans, pay later loans, MSME loans etc.

While I do not understand tech, basic secondary research about digital lending opportunity, the potential opportunities for businesses unbundling digital lending value chain to create unique business models is immense. Attaching some of the reports elucidating the same.

india_fintech_guide.pdf (3.9 MB)

India-Fintech-Report-2021_-The-Digital-Fifth.pdf (3.1 MB)

Financials: The company doesn’t have much to show in terms of financials owing to its short history in its new avatar. However, it is pleasing to see a profitably growing business with sales majorly led by fee business. YTDFY21 hasn’t been kind to the business owing to very high delinquencies for digital lending startups in 2020. The company’s revenue is linked to the loan book growth of its customers making customer selection a key factor for sustainability of numbers.

Having said that given the size of the business currently and lack of ton of public information, its the promoters who would be key differentiating factors in making this business scalable.

Promoters: I have had a one on one conversation with the promoters ( a very brief call so couldn’t really ask all the questions I had) and while the judgments can be subjective, I felt the promoter is a driven, focused individual unwilling to be flashy but at the same time ambitious enough to aim big.

I will briefly describe the thought process of the promoter during the call below

- Identifying winning fintechs is key in scaling this type of business. Rather than onboarding every random well-funded startup, key is to identify businesses that have unfair advantages leading to scaling up of their loan book

Have a look at this link that might give some insights

-

Company is currently focusing only on digital lending ecosystem but has ability to develop products for other fintech areas including insurance aggregators, online investment platforms, payment companies etc

-

Company is currently looking at onboarding some of the biggest tech companies in India including a large e-commerce company and a large food delivery company

-

The promoters don’t mind an equity dilution in the future in case they would want to take up loans on their books. (I didn’t really feel this as a positive though)

Key Questions to ponder: Given the stage the company currently is in, over analyzing financials or valuation doesn’t add too much of value in my opinion. What matters more is the execution and sequential improvement in topline and bottomline once the market environment for digital consumer lending revives. In addition, the following key issues need to be understood better

-

Sustainability of revenues/selection of customers: Apollo Finvest as a business claims it doesn’t really have any competitive advantage in lending space (refer FY20 annual report which clearly explains the journey and thought process of the promoters). Hence, what makes Apollo Finvest think that the fintechs with which it partners have an advantage in lending that can give a sustainable revenue to Apollo Finvest? As a corollary, how does Apollo Finvest choose its customers so as to fool proof its revenues and profits?

-

Value proposition: How does Apollo Finvest as a business deal with the possibility of Fintechs deciding to go their own way once they achieve scale? In other words, what exactly is the value proposition that Apollo Finvest offer its customers across the life cycle of its customers (seed stage, early stage, growth stage and mature stage)

-

Talent: one of the major constraints would be “People” for a tech company like Apollo with limited resources (as of now) to attract the best talent. How does Apollo Finvest plan to manage the same?

There are several other micro questions that are relevant and important for such a business but I feel if the company is able to get these major issues right, it would be able to scale-up profitably.

Request fellow members of the forum to share insights on the business and other KPI’s for such a business.

Disclosure: Invested at CMP