Apollo has started a substack

2 Likes

Hi,

This is a business which has clear optionally associated with it. The biggest challenge is a slightly hidden one.

They will move into big league when big platform companies use them to lend. But big platform companies have great tech and that tech team often wants to build everything in house.

Have experienced this very close hand while building PaySense.

PS- Invested as the optionality is quite large

4 Likes

Hi @constantseeker_

Curious to know more about your experience with PaySense and why you think platforms will want to make payments and loan management softwares which will not be core to their business. I’m thinking of platforms like say Zomato or Uber, why will they want to re-invent the wheel? In fact I think they may not even want to be in the lending business, but will likely lend only to help their partners scale. and so don’t think it will be worth the effort for them to build Apollo like infra from scratch. But please do share if your experience has been to the contrary.

1 Like

that is exactly the logical way to think through this. And i would 100% assume this.

However, like in case of PaySense or any other platform we always had chance to take an off the shelf product and then plug it with our API’s and custom design our front end. The problem is that you don’t raise money to buy things off shelf  but you raise money to build it in-house. The tech team needs to be shipping new things etc etc

but you raise money to build it in-house. The tech team needs to be shipping new things etc etc

of course from a rational view point this is nuts, but decision making is often beyond rational factors.

My bet on Apollo is that one of the large platforms will do think on this rationally and that will open flood gates then

4 Likes

i agree to this, every company may want to their own customised version LMS and have better control over it. building these things is not tough (excel sheet automation) so, may chose to develop their own.

However many may not have expertise to do it which will opt for Apollo Finvest platform. Its not very obvious to me today that everyone would want to use sonic.

In the lifecycle of a fintech business, just when they are starting their lending operations, it would make sense for them to use Apollo as they might not have too much money to spend on the tech and therefore use a plug and play solution.

But if indeed they are successful and raise money, they might as well do it in house for better control on their product and getting necessary tweaks done from time to time.

This is a model in which the successful the customer becomes, the lesser they are likely to de dependent on you. That is not necessarily a bad thing if there is enough future volumes. But how many fintech lenders does India need.

So, it looks to me that they might always be stuck with clients whose size will be lower and therefore the ability to earn from them. So its success depends on getting big clients who will continue even if they grow big or getting big Financial institutions or NBFCs as clients for their product bcoz the claim from team is that its far more superior.

But that does not seem to be the strategy

One of the point’s which made me think that, this might work is the discussion around who would be prospective AF’s customer.

He spoke about non fin-tech companies getting into lending to their own clients, backed by their knowledge of their client’s business potential. Zomato potentially getting into lending business for it’s restaurant owners is perhaps not the brightest example (as a prospective AF’s client) IMHO because even if Zomato may be considered non fintech it’s too tech oriented to forgo such development opportunity outside of it’s own tech team.

But it’s possible to think of a lot of other non fintech players who know their clients pretty well (mostly B2B) and their capital worries as well as business potential, to make a good business case for lending to them. Just as a lame example, every wholesaler/distributor perhaps knows it’s own clients well enough to become a lender to them (if he has capital). Nikhil spoke about PharmaEasy being in that situation, where it knew the potential of many retailers who were it’s customers but were not able to scale due to lack of access to capital and not being able to do anything about it even though they had capital. PharmaEasy in this case was non fintech but tech player. But one can imagine, lot of non tech players being in similar situation, wheather they have ambition to be a lender to their clients is a different question.

Thanks for starting this thread. I have a few friends in the fintech space so did a little bit of scuttlebutt on Apollo Finvest. Here are my findings:

Apollo Finvest makes money in 2 ways:

(1) Providing capital to fintechs - Already a big business for NBFCs given the advent of fintechs over the last few years. DMI Finance, Fullerton, ABFL, MAS Finance, Clix Capital and Avanse Financiers are some of the main lenders in this segment all having AUMs in excess of Rs 2,000cr. DMI Finance is the leader with Rs 3000cr+ AUM. NBFCs ask for a deposit of 10-25% to start a lending relationship. For ex: if a company wants to lend Rs 100, they have to provide Rs 20 as deposit to the NBFC. Most startups borrow at 10-14% and lend at 14-20%.

It will be very difficult for Apollo Finvest to compete with most of these NBFCs as their cost of borrowing will be much higher. They might attract a few very early stage startups but these startups will migrate to bigger NBFCs eventually to reduce their cost of borrowing and increase scale.

(2) Providing a plug and play software as a service (SaaS) to enable lending: This is a interesting way to capture clients and make up for the disadvantage in capital. The problem here is two-fold: (1) Most fintechs want to build their own tech hence the word ‘tech’ in fin’tech’. (2) There are SaaS companies focusing on individual aspects of lending ex: Setu for collections, Hyperverge for video verification, Digio for document verification. Most companies will start using these solution as their backbone and build out a layer on top to bring operational efficiencies, collection efficiencies and sourcing efficiencies.

The above points hold true for non-fintech companies too. For ex: BYJUs and OLA have been borrowing from much bigger NBFCs.

In a nutshell, Apollo Finvest is in a interesting space but don’t see them scaling too much unless they change something major about their business model. Will be very interesting to track their progress though!

7 Likes

Is it possible to know who are their top 5 costumers in LMS segment ?

and how much is the current revenue contribution.

https://www.apollofinvest.com/static/media/Digital%20Lending%20Partner-%2019.08.2021.2912191c.pdf

Details of clients from their website

1 Like

At 1:15:00 for a question on cost of api. The response is not encouraging. Usually costs are fixed for certain quantum when working with cloud technologies. As subscription cost will be fixed upto certain usage. Also everywhere it seems more like one man show. only Miklil talks, not a -ve thing but we have to live with such key man risks in microcaps.

Apollo Finvest, for all practical purposes, is a start-up. And like any start up, it is solely dependent on the founder. I think an investment in Apollo Finvest should be viewed as participating in a series B or C fund raise. This is an industry and model which is evolving - he is trying to create a market, and so the bet is largely on the pedigree of tbe founder and not pure play business fundamentals yet.

4 Likes

Annual Report 2021

https://www.apollofinvest.com/static/media/Annual%20Report%202020-21.e6aa1d8e.pdf

1 Like

Hi

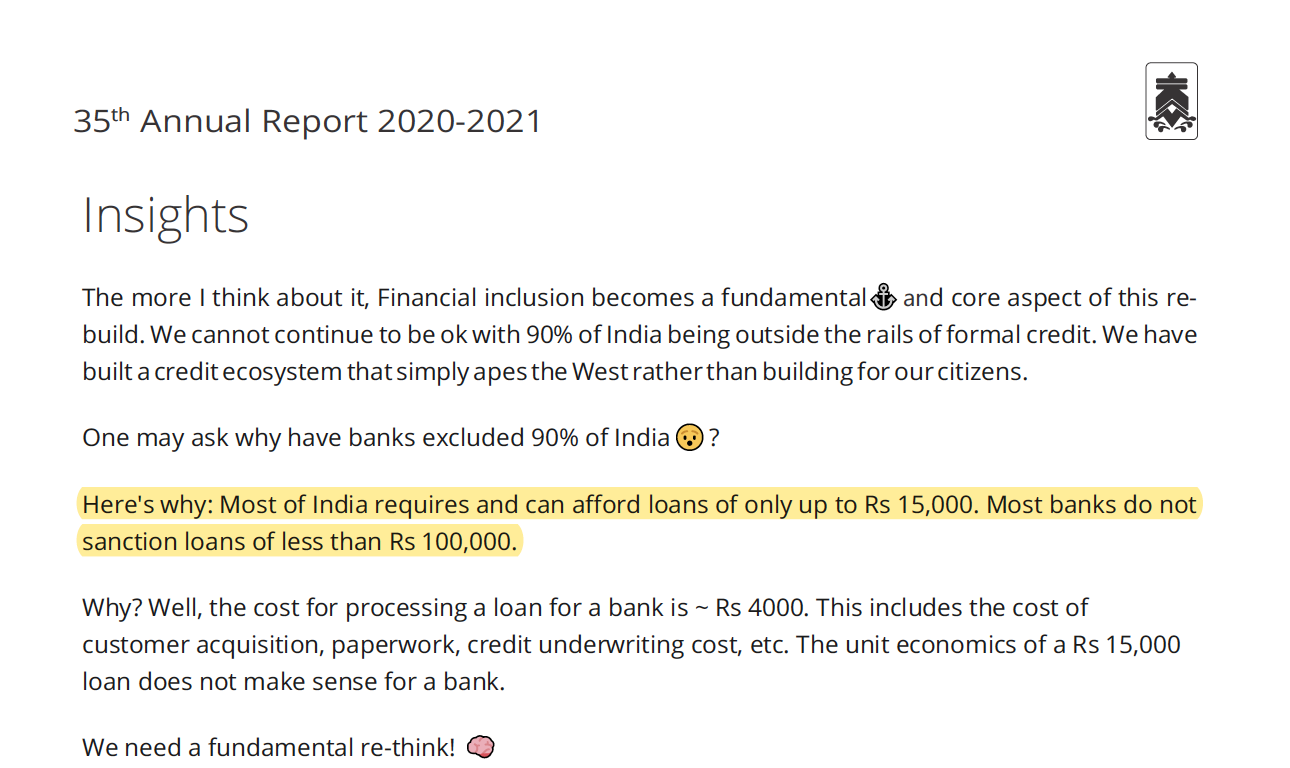

A query: In the previous ARs and tweets and substack letters I don’t recall them focussing on Financial Inclusion but in this year’s AR it seems now its their mission. What happened here? Or is something amiss in my understanding. The phrase ‘AWS for lending’ also is missing from AR21.

They say most banks don’t sanction loans below 1L.I would have hoped that they atleast checked data in public domain published by RBI for this.

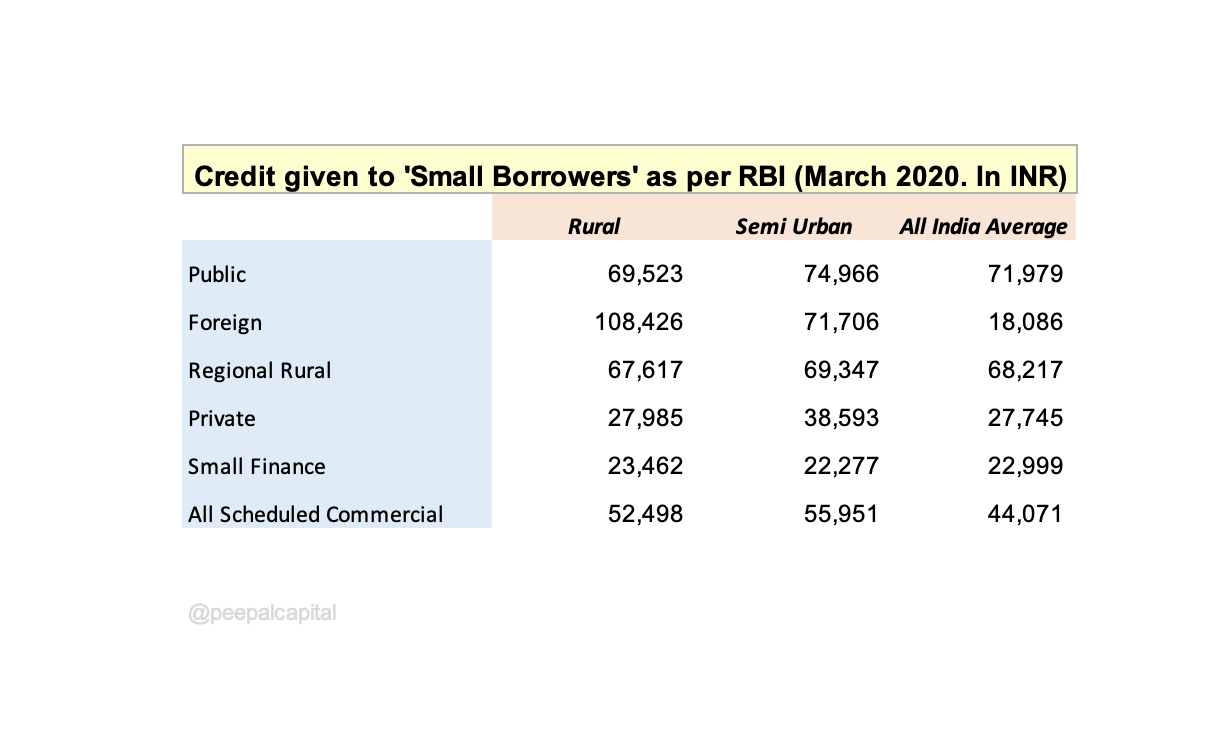

Here is the data for end of March 2020 across bank group wise and also population group wise. Focusing on Rural and Semi Urban as that is where most financial inclusion is required. These are average loan sizes in Rupees given to small borrowers.

Infact barring Foreign banks in Rural every single bank type across Rural, Semi urban, Urban, Metros have average loans of less than 1L. National average for these small borrowers in 44 thousand rupees.

Rgds

Deepak

Disc: Tracking.

12 Likes

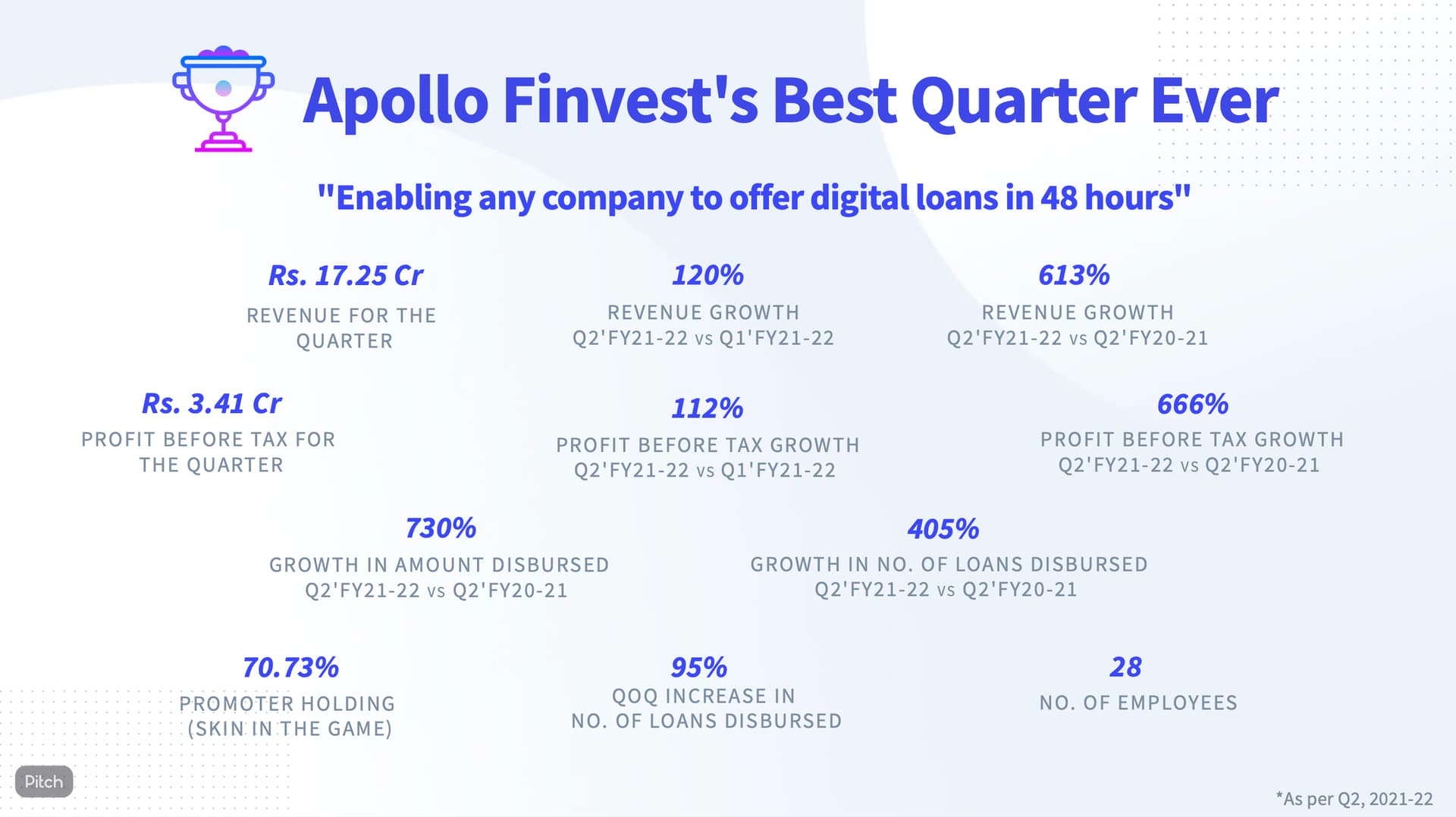

Q2 Results snapshot

The next big step for us is doubling down on our people. That is our secret sauce and our biggest treasure. Hiring is priority 1.

Opinion on results. Current employees are 28, any idea of employee strength in past…

Disc: Recently invested.

1 Like

28 is the highest its been. I saw the open positions and what they’re offering. Full stack engineer 3.5-5 lakhs, senior full stack engineer 6-8 lakhs, Assistant credit manager 3.5-6 lakhs, human resoumanager 3-5 lakhs, VP Operations 10-20 lakhs, Company secretary 3.5-7 lakhs and founders office 5-15 lakhs.

No equity for all except Assistant credit manager and founder’s office (https://angel.co/company/apollo-finvest-1/jobs).

I don’t see how they will get any quality talent in this market for such low amounts.

Good results though. Numbers are beginning to match the narrative

5 Likes

Interesting they are raising debt capital through NCDs

1 Like

Q&Q Revenue is down to 21.5 cr from 27.4 cr. Int income and fees & Commission is significantly down Q&Q.

Profit is up 6.3 cr from 2.7 cr qtr ago due to low expenses.

As per my opinion qtr result is bad. I Am invested due to young management. This is a microcap - a highly risky company, investment should be done carefully.

4 Likes

To be completely honest I don’t understand what they do.I’m betting on Mikhil because of the success he has achieved.

Having 2% exposure.

3 Likes