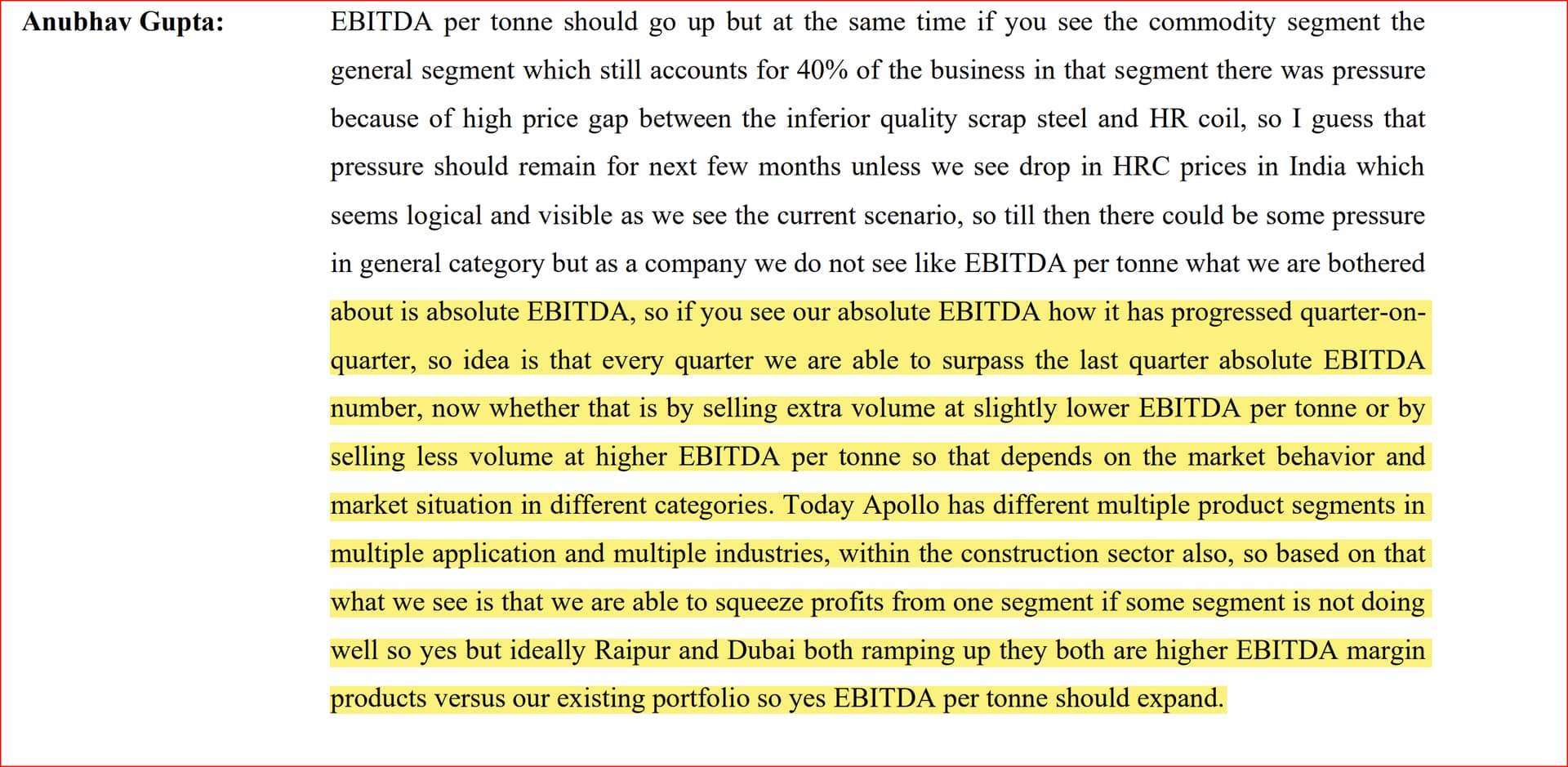

Please do check EBITDA/ton that JSW, Tata steel make vs APL. you will get a fair idea why this may not be that lucrative for them.

There would not be any impact on existing EBIDTA/TON if JSW/Tata steel expand in this segment. Its a high ROE business and has now attained a decent size to attract to the eyes of Tata steel /JSW …

APL PAT has grown to Rs 650 Cr , which is a decent amount to attract any one in a high ROE commodity business…

The more Apl Apollo expands the more it will get highlighted and the more it will be tempting for JSW/Tata.

Disclosure: Not invested, Just trying to find out anti thesis

3 Likes

JSW, Tata do EBITDA of 15000/ton vs APL 5000/ton. How will this not impact the EBITDA? I am not saying they will ignore the str tube market, just that they wont be as aggressive as APL

3 Likes

Q1 2023 update

3 Likes

https://www.bseindia.com/xml-data/corpfiling/AttachLive/10beceee-f4c9-4d9d-a155-54df20335282.pdf

great results as expected - 60% yoy growth

good to see an aggressive vision 2025 by the company

they have given a volume target of 4 mn tonnes which seems possible

EBITDA target of 2.5 times current ebitda- that comes out to be 2500 cr.

this gives us a potential of around 1700 cr PAT by FY 25-26.

these targets seem aggressive but achievable

it will be important for the company to get more growth from value added and super value added products to achieve these targets.

Disc- Invested

7 Likes

Summary Q1FY 24

- APL Apollo Tubes had a successful quarter with the highest-ever volume sold at 662,000 tons, demonstrating market leadership and growth-focused mindset.

- Operational highlights for the quarter:

- Revenue increased by 32% to 4544 Cr.

- EBITDA increased by 58% to 307 Cr.

- EBITDA/Ton for the quarter was 4645.

- PAT increased by 60% to 193 Cr.

- Value Added products accounted for 57% of Total Revenues; aiming for 70% when Raipur plant is at full capacity.

- EBITDA per ton was impacted by channel de-stocking but expected to improve and stabilize around 6000 in Q3 FY24.

- Efforts to reduce Employee, Power, and Freight costs to support EBITDA per ton in medium term.

- Excluding Raipur Plant, EBITDA per ton higher at 5700.

- Provided guidance for future volumes:

- FY24: 3.0 Million TPA

- FY25: 4.0 Million TPA

- FY26: 5.0 Million TPA

- FY24 EBITDA guidance: 1400-1500 Cr (40-45% growth over FY23).

- Raipur plant production started, aiming for 0.5-0.6 Million TPA for FY24 with EBITDA per Ton improving.

- Raipur plant for Value-Added Products; new greenfield plants for commoditized products.

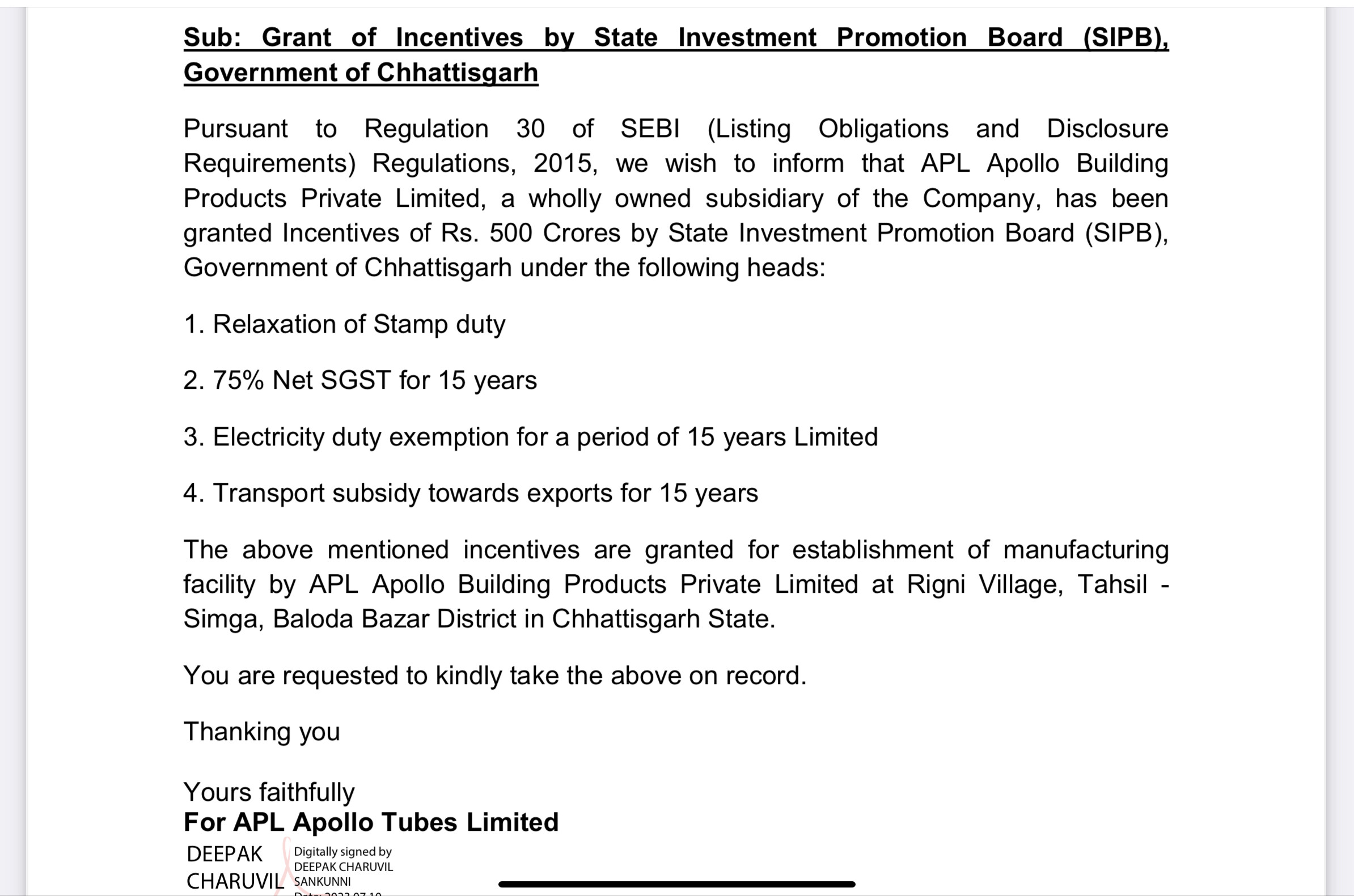

- Expecting 100 Cr incentive from Chhattisgarh government for Raipur plant investment.

- Capex of 300 Cr for 5.0 Million TPA capacity by Q4 FY24; plans for additional 5.0 Million TPA capacity later.

10 Likes

Promoter Rahul Gupta complete exit from APL apollo… Sold 243 crores worth of shares.

https://twitter.com/niveyshak/status/1696940136527794441?t=t2bqvhFnPhVQJhXPuuwiNw&s=19

He sold fifty percent of his stake two years before and remaining now . May be he is uncomfortable with the merger of Tricoat and APL due to reduced personal importance. To be seen as individual choice rather than red flag.

1 Like

Isn’t he running finserv?

Not only as director in SG finserve but many other companies as MD and as Director

Actually he was the Main promoter of Best Steel logistics in which son of APL Apollo Tubes worked and later bought the company from him. Then renamed as Apollo Tricoat and merged with APL Apollo after bonus shares. Rahul gupta held few percentage of shares despite selling the company which he used to sell in increments when ever Tricoat reaches a milestone which played as rise breaker. Now he sold his final holdings in the company.I find this as good indicator and the real growth story is yet to start for APL.

My views may be biased since holding good quantity from the bottom level since 2018

5 Likes

To keep it simple - ill ignore the sale and look at company fundamentals and decide if i continue to add/ hold/ sell accordingly…

2 Likes

Rahul Gupta is son of Sanjay Gupta, right? isn’t this the same Rahul Gupta?

1 Like

Fundamentally, co is doing great. But I think as Promoter, some kind of explanation should have been filed with the exchanges. It is not legally required but some clarification as to why the sale happened. Would give clarity to investors, ie may be from long term perspective, Rahul will be responsible for SG Finserve and that’s why he sold and other son would be responsible for APL Apollo. (just my view, I may be wrong).

1 Like

Why Sanjay Gupta, Chairman and Managing Director of Apl Apollo not attending AGMs? On 9th sept day before also he was not present due to personal reasons. And Id I remember even last year AGM also he was absent. How is this possible that he gets into personal problems just on that particular day of AGM?

1 Like

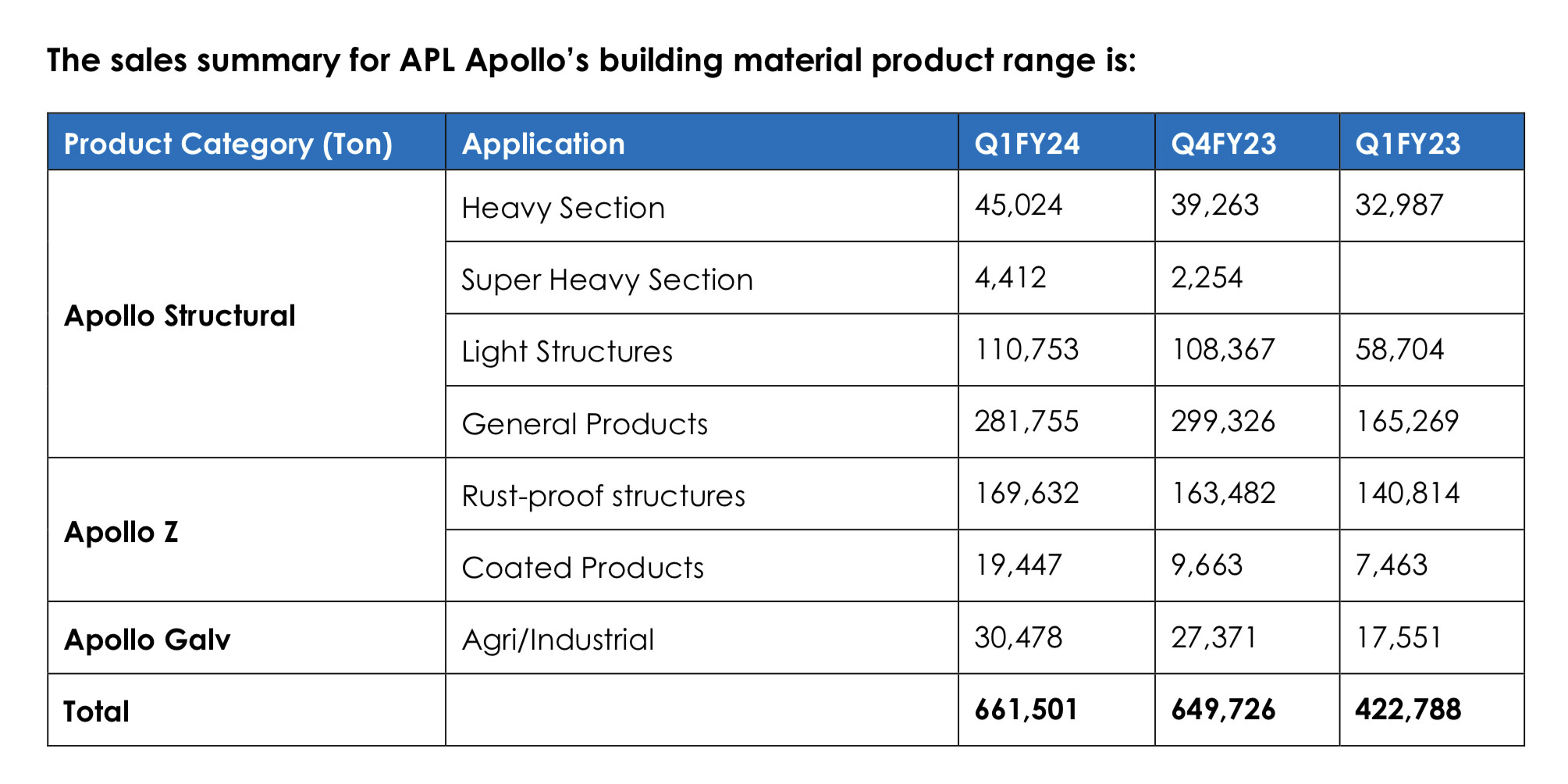

As per the latest volume nos uploaded, the value added seems to have dropped from 57% last qtr to 55% this qtr. Overall volume is almost flattish at 675k vs 662k last qtr and 11% up compared to last year same qrt nos . Raipur volume has shown a significant uptick from 19447t to 28755t. The ebitda for the nos should be north of 300crs.

3 Likes

1 Like

I am little skeptical on the business as the profit depends on steel commodity prices+The opertaing margins for the company is very low 6-7%.The only way it should increase is by volume increase in capex…Yet despite opening its branch in Ranchi,company has not shown significant profitablity-Last 3 quarters were almost flat.

Please suggest for more growth triggers in the business?

Disclaimer-Not Invested.