What exactly you want to indicate?..Kindly elaborate

Banks have their own NBFCs. Auto companies have their own NBFCs. All due to a variety of solid reasons, which ultimately boost their business on the ground. There is no Gaming in that. On the contrary, it is an old, well-accepted, successful way of boosting business. Consider APL joining the same league.

Cheers

RR

1 Like

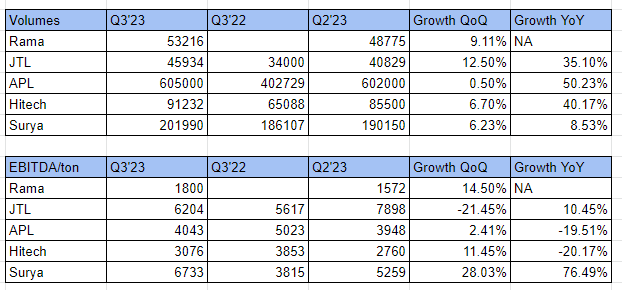

The entire structural steel space is heating up due to pick up in infra. Smaller players like Rama steel, Hitech are benefitting from Jal Jeevan mission as well. Rama has recieved few orders for Jal jeevan. Tata metallics who make DI pipes also are big beneficiary of the mission. Have done a benchmarking below of QoQ , YoY volumes and EBITDA/ton growth.

2 Likes

Thanks for this update. Do you know why EBIDTA/ton so less for Rama ?

Thanks

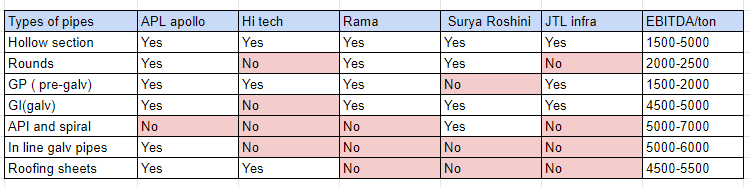

There arent great updates from Rama, but the value added products is <20% as compared to 50%+ for APL. The below mapping is an approximation of SKU’s the competition has.

4 Likes

Good data in the article.

2 Likes

Hi everything looks good in the company, aggressive growth funded by internal accruals, very good ROCE.

Only thing which is worrying me is promoters stake is continuously reducing…

Anyone has insight about this?

this is the same trend in many midcap companies… Numbers are improving but promoter keeps selling.

31.16 % promoter holding is too low.

APL Apollo Tubes (APL Apollo), India’s largest structural steel tube company, is honored to announce that this year marks the monumental 37th anniversary for the company as an industry leader and innovator. Since the company’s inception in 1986, APL Apollo has developed pioneering products that have transformed the market landscape, setting the bar with innovative solutions for the customers, latest technologies in steel tube manufacturing and best industry practices related to consumerization of structural steel tubes in Indian markets.

Team APL Apollo is thrilled to be celebrating 37 years of excellence and wishes to express its profound gratitude and appreciation to the channel partners and all stakeholders who played their role in APL Apollo’s success story.

On this occasion, we are proud to announce that the company has signed MoUs with its top distributors for sale of 2.4mn tons of structural steel tubes in FY24. This gives us enough confidence to achieve our sales targets for the current financial year. These MoUs do not include sale from exports division, OEM division and sale of coated products from new Raipur plant, which are newly launched.

We are equally thankful to our raw material suppliers who have supported APL Apollo to achieve heights in the steel downstream industry. Our main suppliers have assured of even stronger support for FY24 to enable APL Apollo to run its operations smoothly and efficiently. We also dedicate our success to the thousands of employees and shareholders who have reposed faith in the management of APL Apollo and the board members who have guided us. With strong operating cash flow generation and completion of Capex cycle, the management is focused towards improving shareholder reward as per the board approved policies.

APL Apollo looks towards the next 25 years to not only develop additional technologies but also to expand upon the value that it can add to steel construction industry in India.

3 Likes

will the sale from exports divison,OEM division and coated products from Raipur be around 0.6 million? As they had guided for 3 million ton in FY 24

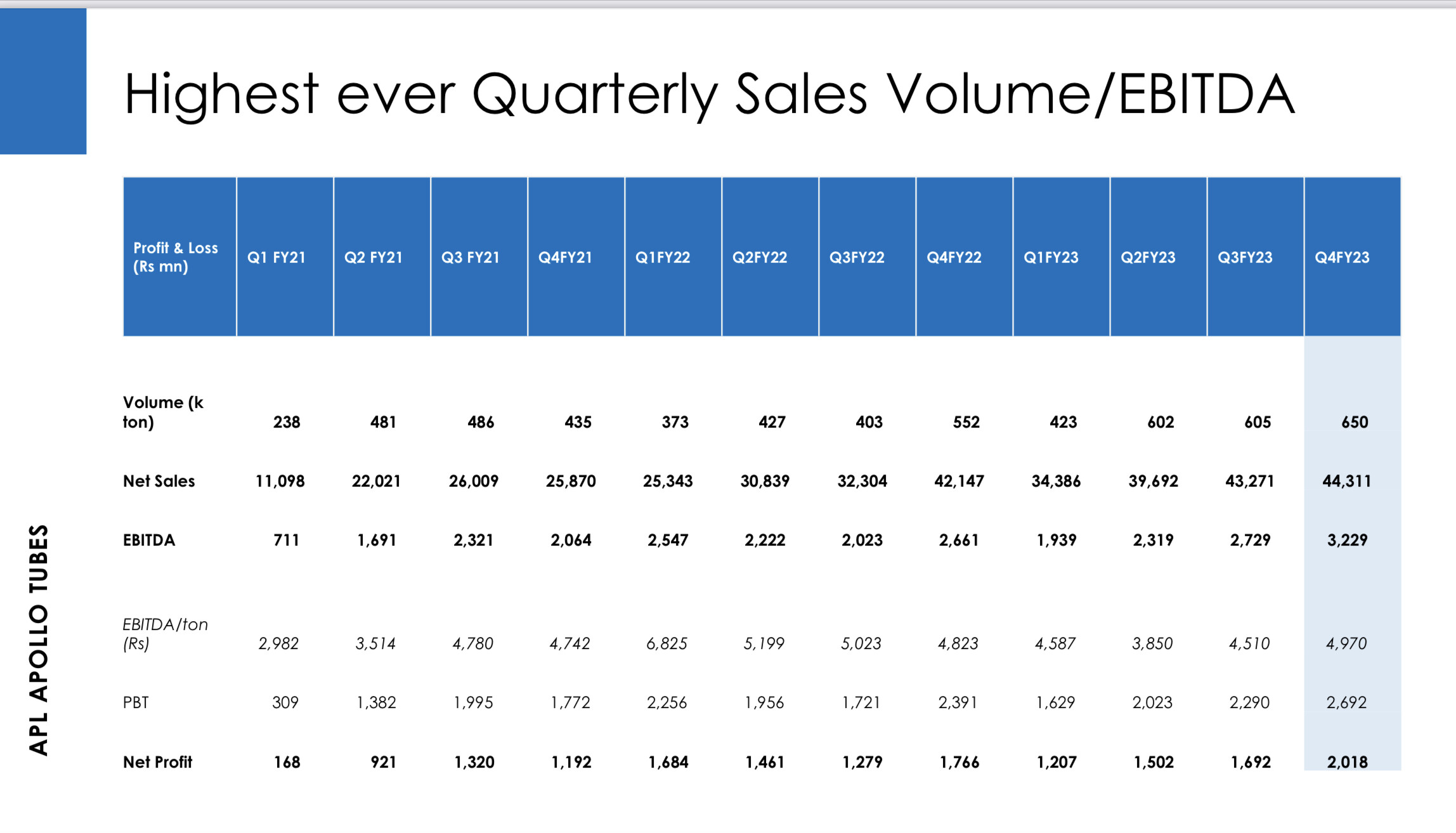

While volumes are important, EBITA/ ton is also very important. As per Q4 presentation, about 40% of sales are at a low EBITA of about 2600/ ton. APL appears to be loosing moat in a business of metal pipes, which ultimately are a commodity, and, with passage of time, will sell at commodity price.

I have been invested since last couple of years, but now loosing confidence in its super profitability that APL had in the past. Competitors are catching up fast.

Can you elaborate on competitive intensity? I was under the impression that they are the sole player in this speciality.

Disc. Holding from last 1 year.

In FY 20, 21 and 22, NP increased by 79%, 59%and 52 % respectively. However, in FY 23, NP increased by only 4%. OPM in FY 21,22and 23 has been about 8%, 7% and 6% respectively indicating inability to pass cost to consumers.

In last four con-calls, promoter’s tone been subdued and defensive rather than very positive earlier. Stock is at a high PE of about 47-48 even after price fall.

I have sold 90% of my holding. Will consider entering again - not on hope- but actual solid performance of sustainable improved OPM.

Promotor bought APL shares worth 168 CR on last Friday via his shell company to boost stock price. Details of bulk deal on BSE/ NSE site. I didn’t appreciate it.

2 Likes

Many of your observations are subjective and heresay.

- You cannot deduce the future performance of a company from the tone of a promoter in concalls. There can be so many reasons for this.

- Also how can you be sure that its a shell company of promoter and if its so, why dont you complain to Sebi about it?

- I asked you about competitive intensity. I was expecting that you will quote the numbers of other companies which are operating in the same segment and taking away Apl appollo’s market share. But you didnot talk about any of the competitors.

One request to you is, while talking about any publically listed company, please talk with utmost responsibility as thousands of invetsors have invested their hard earned money into these shares and with wrong information or rumours , they will lose their life long capital. Kindly be kind.

5 Likes

Investor Concal

Hi. Good evening. Thank you for the opportunity. Congratulations on

consistently meeting the stated targets and good to see how they will play out as well. First question,

Sanjay ji was more on the competitive landscape. We hear from certain regional channels that Tata

Structural and JSW Steel both have ramped up their capacity in structural tubes and JSW Steel has

actually started manufacturing that. Few regional players also we hear are picking up quite a decent

amount of volumes on a monthly basis. I just wanted to hear your thoughts because what is happening

is, there is a lot of competition now building up for APL Apollo which was absent for many years and we

had a very clear runway of growth. Just your thoughts on, you know, is it really real and what do you

expect going into next two to three years?

What are the thoughts of Forum members in this regard.

Management reply was defensive and elusive

Mr. Sanjay Gupta (00:11:13): Thank you, Rahul. Rahul, I also hear and read in the presentation of Tata

Steel, right now they have a capacity of 1 million tonne and they want to go to 4 million tonnes by 2030.

But I have no plans in which sector Tata is going to or want to go for 4 million tonne in the next six,

seven years. If we go for 4 million tonne, right now it is in the structure to buy 2 million tonne. If we

calculate, so he has the capacity for structural tube of 1 million tonne or 1.5 million tonne, this is not a

big threat for us as well as Tata is a responsible player in the market. He never destroyed the market so

we are not worried about the Tata Steel. JSW just taken a plant called Bhushan Power in Orissa. They

have a little bit of capacity of tube in the parental plant. Still we have no such as information from the

market towards their planning in that commercial. In JSW, we have no worry so when they are helping

JSW or Tata Steel also, they are healthy players. They is not worry if anyone comes I don’t worry about it that as they are not a market destroyer, if they increase a little bit of capacity my cost is in control, my

everything is in control, I have a good value addition product with me. I have good branding in the

market, I have a good social network, I am not worried at all. Market is also growing very fastly in the

two business. What we are saying is that there is a good lot of work, maybe all can survive it is not a big

issue for us, but time to time, there is a healthy concern, we will learn from it and take the collective

action and go forward. I don’t see today any big threat.

2 Likes

May be atleast for next 5 years, there is no real threat to APL Appollo.

1 Like

true, real dent in business may happen after 5 years but Mr Market may start factoring it well ahead…

1 Like

What is the entry barrier for Tata Steel & JSW to enter into this high ROCE business…

JSW has entered even into paint segment also…

JSW & Tata steel will never been in a hurry infact they would strategically allow Appolo to develop the market for structured product and once the pitch is ready they can come and bat for a long innings. This will be a forward integration for them and definetely they can command a better margin than Apollo. As per my understanding Apollo is only playing volume game and the margins are wafer thin.

2 Likes