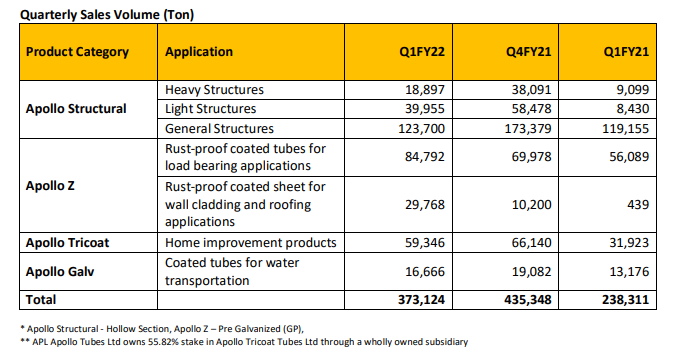

FY21 Sales Volume Performance

1 Like

Wonderful performance. It continues to soar quarter on quarter with great consistency.

1 Like

Any reason why volumes are down ~10% QoQ?

Is that due to higher steel prices or were Q2/Q3 just abnormally high as Q1 sales spilled over?

1 Like

Guptaji already said in last concall uptake in January was low due to price hike but I think February & March has taken care off.

3 Likes

It passes on any increase or decrease in steel prices to customers with a time lag so there will be no material impact on the margins

The things which can impact APL Apollo is:

- Subdued steel demand growth

- Sustained weakness/ decline in steel prices which could result into inventory losses

3 Likes

In freely available commodities like steel, if the price goes up steeply then customers tend to reduce order qty to see if the price comes down. But this can be done only for a limited time and the inventories have to go back to normal levels. Steel prices seem to have reached the top or near the top. Large buyers would be looking at the prices, inventory levels and demand very carefully.

1 Like

APL Apollo Tubes reported strong EBIDTA for Q4FY21. EBIDTA /tonne stood at Rs 4,742 (+59% YoY) on better product mix. Its EBIDTA jumped 72% YoY to Rs 2 bn led by higher volumes at 435kt (+8% YoY)

Operating cash flow for FY21 was R 9.8bn as its working capital days were lowered to 8 days from 25 days in FY20. Net debt fell to Rs1.6 bn in FY21 from Rs7.9 bn in FY20.

Surprisingly, however, no dividend has been declared for FY21. Wondering if management thinking massive capex/acquisition?

2 Likes

From Reliance sec report

What We Heard – Conference Call - Key Takeaways:

-

Quarterly Volume: The company reported 9% YoY volume growth in 4QFY21. Its market share stood at 50% in FY21 vs. 40% in FY20.

-

Working Capital: Net working capital improved to ~8 days in 4QFY21 from 25 days in 4QFY20 owing to successful change in business model to Cash & Carry. The company has an inventory level of <20 days and ~8 days of order book in hand.

-

EBITDA/Tonne: EBITDA/tonne stood at Rs4,742 with focus on achieving the Rs5,000-mark by FY22-end. Focus on value-added products (VAPs) should further aid the company on margin front, as the contribution of VAPs increased to 57% in FY21 from 45% in FY20.

-

Expansion Plan: The company plans to spend 20-25% of its EBITDA (~Rs1.75bn) on capex in next 3 years. It has already begun a capex to produce 500x500mm diameter structural tubes and color-coated tubes in Raipur. The fi rst phase is expected to start by Dec’21 with ~0.4-0.5MT capacity. The company’s current capacity stands at 2.6MT and expects to expand it to ~3MT and ~4MT by FY22E and FY25E, respectively. The company is currently running at ~60-65% utilization level.

-

Debt & FCF: Operating cash fl ow (OCF) stood at ~Rs10bn, while net debt decreased to Rs1.6bn in FY21 from Rs7.9bn in FY20. Shift in business model to Cash & Carry should continue aid the company on debt front. Free cash fl ow (FCF) stood at Rs6bn in FY21.

-

Outlook: Provided lockdown/restriction eases out, demand is expected to pick-up in next 2 months. The management expects double-digit growth, in case the situation normalizes. 7. Apollo Tricoat: Apollo Tricoat contributed ~15% and ~12% to the consolidated EBITDA and PAT, respectively in 4QFY21.

8 Likes

Your balanced view playing out really well.

As can be seen, the price of both APL and Tricoat are convering faster than expected, that too, on the higher side. All the concerns raised by those who sold out/wanted to exit after the merger announcement have been put to rest with this outperformance.

Business wise, it looks great. Concall went really well. Construction activity is in full swing (even in Tier 2 city like mine) and this should augur well for the undisputed leader

Note: Invested for the last 2+ years and has been a 7 bagger for me

1 Like

The prices of APL and Tricoat have finally converged today. All those who have kept faith in the merits of the merger annoucement have been rewarded since then.

2 Likes

I am assessing the company not only based on past performance but a feeling of the structural steel tubes finding greater share in construction. The new architecture of airports, Railway stations, Malls, Stadiums etc are increasingly using steel tubes instead of beams and angle irons. Similarly in low and middle income housing, steel is replacing wood in many applications. Value added products help in making it more acceptable and aesthetic for higher income group. The management has been agile, smart and bold so far.

6 Likes

Q1 FY2022 sales volume is 86% of Q4 FY2021 sales volume due to second wave related lockdown

The key takeaway is “sale of value added product contributed

67% in Q1FY22 as compared to 57% in FY21”

My take: Superior EBITDA margin due to value added products will compensate for reduction in volume.

9 Likes

To consider bonus shares… The story keeps getting better.The valuations may have run ahead of the business, but the future growth story remains intact

3 Likes

Even Tricoat is issuing bonus shares, primarily due to merger announcement earlier. Interesting development!!

Disc: Invested for the last 2 years

3 Likes

Although so much has been described in the thread here’s my summary on the company.

APL APOLLO TUBES.pdf (643.1 KB)

12 Likes

Nice Summary @Chirag.jain48 Thanks for sharing it

1 Like

Report on Apollo Tubes by Motilal Oswal

https://vid.investmentguruindia.com/report/2021/September/MORNING_INDIA-20210907-MOSL-MI-PG022.pdf

3 Likes

Can anyone throw some light on why arbitrage opportunity that lies between APL Apollo & Apollo Tricoat tubes. Both would merge, may be, by Q4.

Disc: Invested in both. In APL Apollo from low levels.

2 Likes