I just can’t get my head around the fact that this company has an operating profit of around 7% and PAT of around 3% of Sales, yet commands a PE of 33. (all metrics from Screener)

Discl: Not invested

1 Like

Its the nature of the business, other players go into losses when their PAT margins fall to 1-2%.

There are two sources of ROCE:

1)Demand side: that is the margins

2)Supply-side: that is the turnover

Apl Apollo has been consistently able to chug out an ROCE of 15%+ due to 2x+ capital employed turnover. It’s the nature of the business with low margins and high capital employed turnover, since they have the competitive advantage on the supply side.

Given their high market share, in the management meet and plant visit (visited the Sikandarabad plant in January), the only plausible way left for them to keep growing the bottom line is to keep entering high margin and value-added products(Sanjay j commented a lot on this)

Plant visit pictures and videos:

https://drive.google.com/drive/folders/1gi1Bi9MMzeccVAmtHVRdAnEQmXWc2qfz?usp=sharing

Disclosure: Not a SEBI registered Advisor. This is not a recommendation to buy or sell

10 Likes

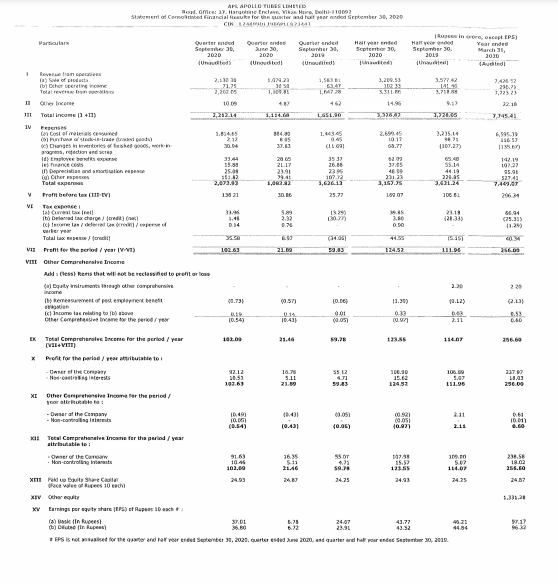

Result is out!!

Share split: The Board of Directors of the Company at its meeting held on October 28, 2020, approved a proposal for sub-division of the face value of

the equity shares of the Company from the present Rupees 10 per equity share to Rupees 2 per equity share i.e. 1 equity share to be split

into 5 equity shares, subject to approval of the shareholders and other regulatory approvals.

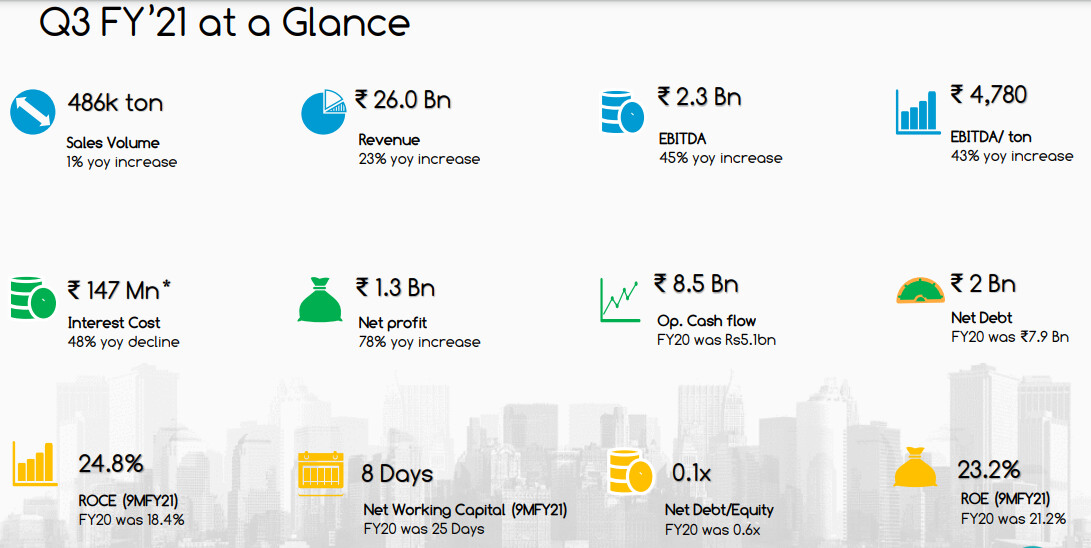

Performance Review for Q2 FY21 vs. Q2 FY20

Sales Volume up by 32% to 481k tons

EBITDA up by 135% to Rs1,691mn

o EBITDA per ton was Rs3,514 (+78% YoY)

Interest Cost declined by 41% to Rs159mn

Net Profit* up by 72% to Rs1,026mn

Net debt declined to Rs3 bn in 1HFY21 from Rs7.9 bn in 31 Mar’20

Employee cost down to Rs695/ton in Q2FY21 from Rs871/ton in FY20

Balance sheet figures:

Net debt declined to Rs3bn in H1 FY21 from Rs7.9bn in FY20

Net working capital cycle improved to 7 days in H1 FY21 vs 25 days in FY20

D/E ratio improved to 0.2x in H1 FY21 vs 0.6x in FY20

Business commentary

1HFY21 market share was 50%

Switched to cash and carry model

Rural sales mix increased to 55% from 40%

Converted crisis into opportunity

Great numbers overall!!

Disc: Invested for the last two years

5 Likes

Very good results and inline with management’s guidance.

The company has emerged stronger in all areas:

- Gaining market share - 1H21 market share is increased to 50% from 40%.

- strengthening its balance sheet by reducing leverage

- Improving working capital cycle

- expanding margins

- Improving cash flows from operations - 1H21 cash flow is higher than full FY20

- Reducing operational expenses

- New acquisitions

- Focus on innovation

- ESG initiatives

Given the huge opportunities in warehousing, affordable housing, urban infrastructure and urban real estate the future looks solid.

Disc: Invested.

1 Like

OCF was so strong that the company has created a 500 cr Fixed deposit! Also repayment of 250 cr of long term debt.

3 Likes

Q2 Concall Notes

Institutional participants

Phillip capital

Ask investment manager

Fidelity investment

Antique stock broking

India infoline

HDFC mutual fund

GS investment

Stallion asset management

Enam holding

1.Shift to cash and carry model reduced debter days to 6 from 25 earlier(Lowest in building material industry).

2. Working capital requirement is reduced to 7 days.

3.Market share up from 40% to 50% due to rural push… rural sales is 55% of total volumes vs 40% last year.

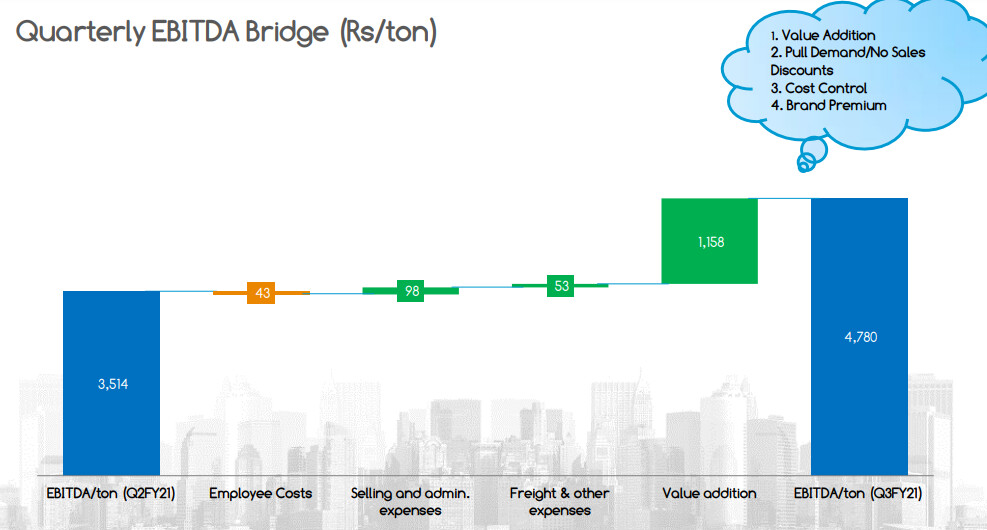

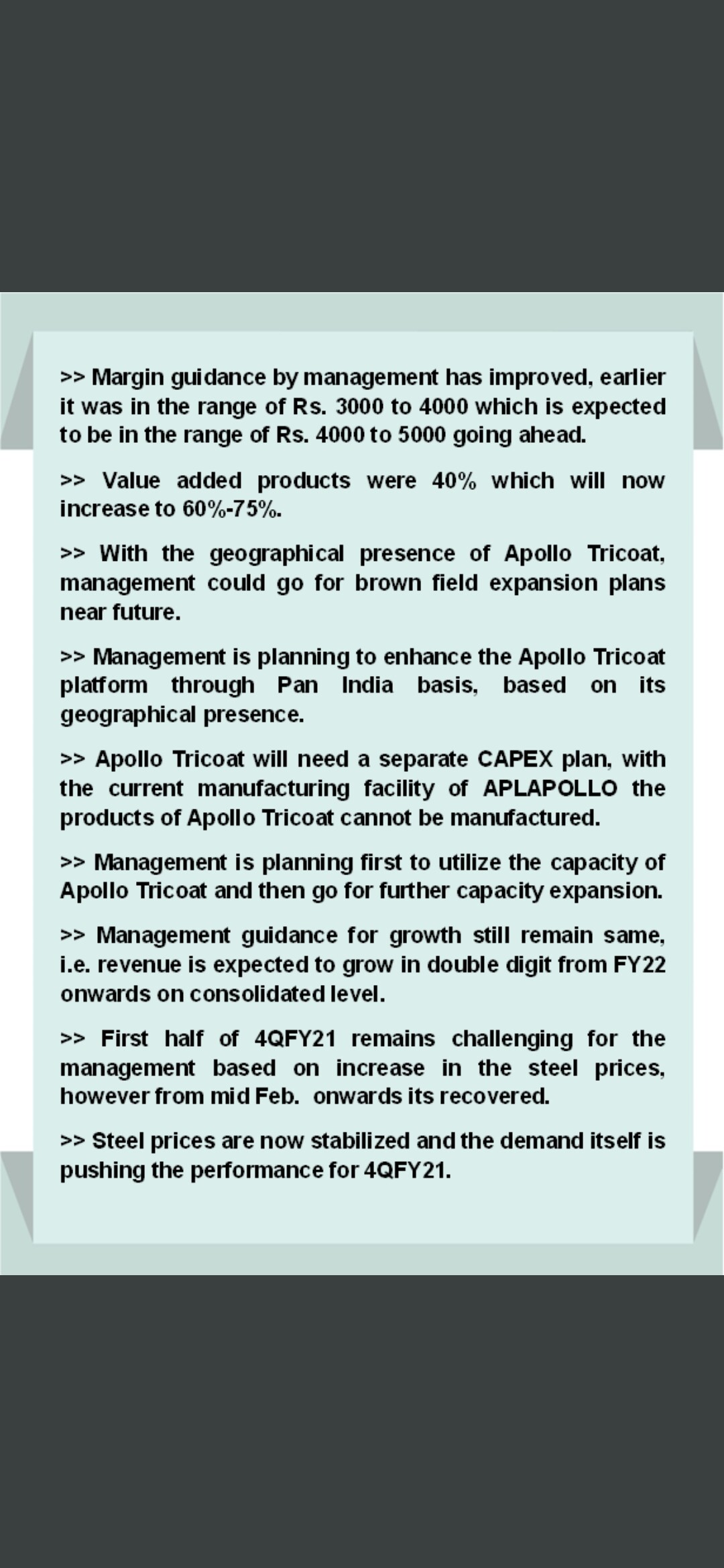

4.Going forward our focus will remain on cost optimization , branding and introducing more value added products to drive growth and improve EBIDTA per tonne… August and September EBIDTA was around 4000 per tonne…… want to make it regular and then will think about achieving 5000 per tonne.

5.Total market size is 7 MTPA of which 1 MTPA is pre galvanized and 2-2.5 is from secondary material.

(tubes made from secondary material is 10000 Rs per tonne cheaper).

6.New value added products like door frames and planks are growing at 40-60% .

7.We are working on three more value added product

a)Coloured tubes

b)Heavy building material (10 MTPA market )

c)ILG (In line galvanising)… for electrical conduit.

8.Total capex is 80-90 Cr in H1 and branding cost is 8-9 Cr in this quarter.

9.Not looking at aquisition but will take a call for capex at Raipur after 2 quarters(Land is already available and company has given some advances for machines but put on hold due to covid).

10.Don’t want to fight in GI pipes with established players (Jindal, Tata and Surya Roshni )as this is not our focus area (water transportation )… want to grow in value added products in building material space.

11.We command premium over competitors due to strong brand image of apollo.

12.Currently 45% is value added … want to grow it at 40% CAGR … want to make it 75% of total volumes in next 4-5 years… don’t want to grow very high in commodity products.

13.We have currently 11 plants… we want to reduce this number to 8 by shifting machinery from 3 small plants.This will help us to reduce gross working capital from 40 to 30… want to become net negative at working capital level.

14.HRC prices were down by 3000 in July and up by 4000 in August and September.

15.Total capacity is 2.6MTPA including Tricoat and maximum production can be around 2.2-2.3MTPA.

16.Not interested in growing distributors but we are working on improving their margins.

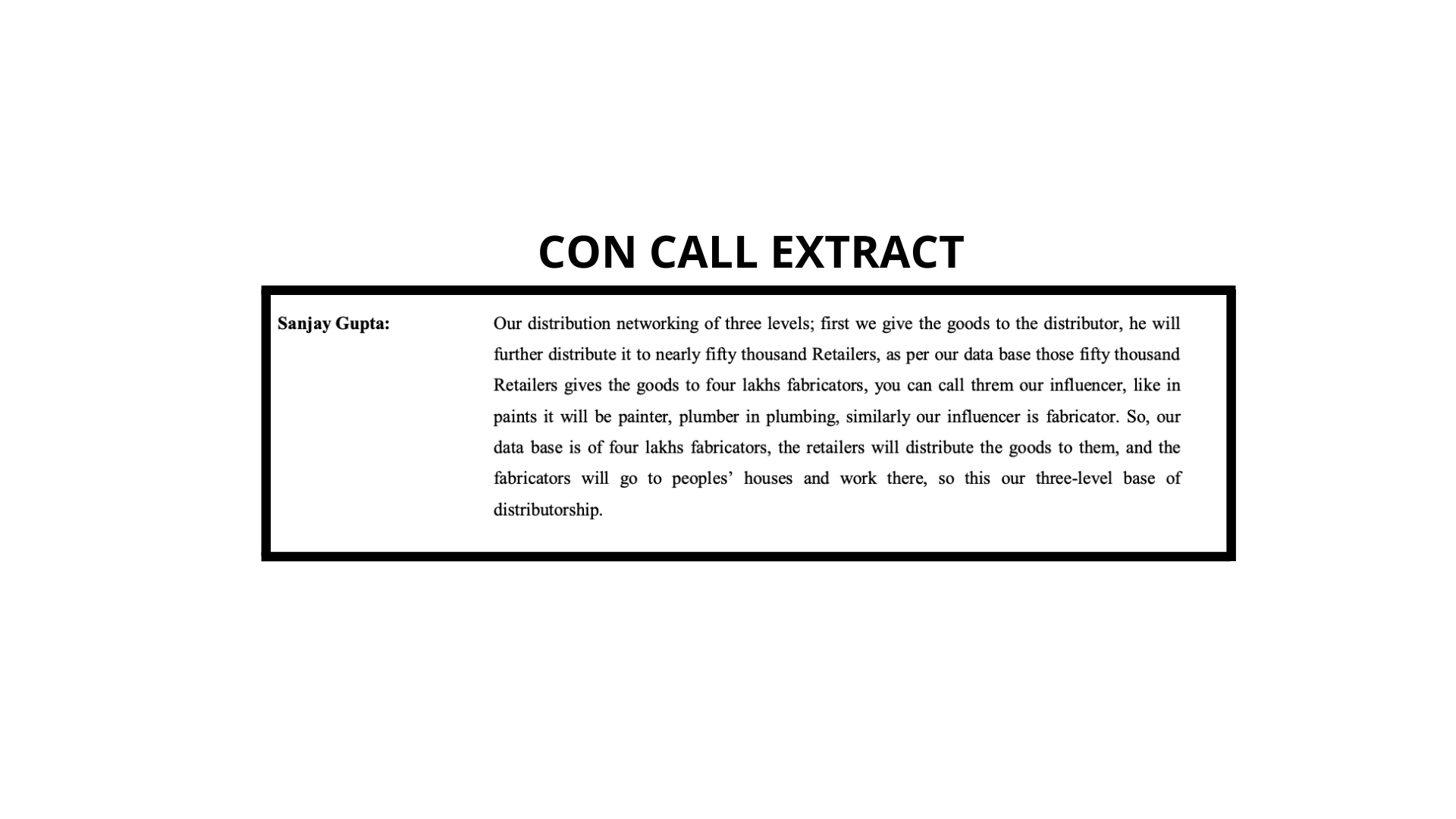

17.Product distribution flows through three layers :-Distributor to Retailers (50k)to Fabricators(400k).

18.DFT is helping to improve service in commodity products and exclusive products (1.2L tonne per annum ) are making 15-20 %.

19.We have reduced inventory from 2L to 1.1 L .

20.Business was going as usual before covid and whenever we thought of changing it … there was a resistance from outside as well as within the organization that this may disturb things… But after covid everything was messed up… so we took a bold call that we will not do business this way… we shifted to cash and carry model… and slowly everyone accepted it … this has happened for entire building material industry.

7 Likes

Business:

- Switched to cash & carry model i.e debtor days reduced to 6 from 19 six months ago. (lowest debtor days in the building material industry).

- On verge of becoming debt-free.

- Working capital cycle of 7 days (lowest in the industry).

- Market share expansion from 40% to 50% in the last 6 months taking away market share from small organized & unorganized players.

- Lower fixed costs: Employee cost down by 20% & interest cost by 75% on per ton basis.

- Current Capacity: 2.6 million

- Working extensively on coloured pipes & working on big sections as well.

- Trying to get margins from branding, controlling freight costs & other costs.

- Total mix: Value Added- 45%, Base-55%

- The volumes that APL Apollo crafts are 10,000 tons per month, 1.25 lakhs ton per annum in DFT exclusive products & in normal products the margin is 4-5%

- In PEB (Pre-engineered building), there is a company called Zamil of Saudi Arabia & APL has recently worked with them and has developed a column pipe.

Management:

- This quarter’s branding has already started, booked a cost of Rs. 8 to 9 crores & the branding expenditure will not exceed Rs.10 crores.

- Planning to shift Hyderabad to Hosur & Raipur & shift that plant 50%- 50% in Hosur & Raipur. This will save Rs. 50 lakhs.

- No plans of expanding distributors for 1-1.5 years.

- In Uttaranchal, Himachal & Kerela, pipes meaning is only Apollo. The brand has started reflecting.

- A survey conducted by APL Apollo showed that out of 500 people, 50% of thee people told that they get 50% customers who just want apollo.

- Value-added part should grow at the rate of 40%-50% per annum (Rs.3,500-Rs.3,600 per ton).

- Target this quarter is to achieve around Rs.4000 & progress to Rs. 5,000.

- July, August, September, October & November are always slow months for the business & Mr Sanjay has witnessed this for the past 15 years as the construction work decreases a lot during the monsoon. The real season stats December onwards.

- The company is yet to enter a good passage.

Risk:

- Volatility of raw material prices.

- Industry slowdown

5 Likes

Having been associated with this stock for the last 2 years, I feel that the current price factors in many positives for the next two years.

Would like to know the views of the other members of this forum regarding its current valuation

2 Likes

I think a lot of folks who have been holding this stock have the same question. It is a good stuck but do the current valuations justify the price? The challenge we have is if we exit, will it give us another chance. Definitely a stock to hold but the continuous price increase is not giving any valuation comfort. I don’t see margin expansion beyond 8%. So, what kind of revenue CAGR to folks foresee for the next 3 to 5 years?

One of the key structural changes that have happened is the decrease in working capital. As the business has moved to cash and carry model. This will likely push the ROCE well above 30%, some part of the re-rating will be structural. The business will be recorded a higher multiple before they moved to the cash and carry model. Another interesting thing that seems to be playing out is the mini virtuous cycle, historically we have seen APL posting the best EBITDA/per tonne when the HRC prices increase. However, the difference between this virtuous cycle and the other one has been that both parts of ROCE ratio are contributing, first is the EBIT Margins (increasing steel prices+value added products) and second is the reduction in capital employed (working capital has structurally reduced)

Few other changes which are yet to play out: Becoming a negative working capital company+Increasing proportion of value-added products.

19 Likes

if management is able to delivery on 5000/ton ebidta, debt free, grow B2C business there is no reason why 5 years down the line they can be in a better shape than today. It might re rate too if the current short term benefits of cash and carry becomes a permanent feature.

1 Like

Great set of numbers once again ![]()

Focus on value added products

Warehousing can be great demand driver

6 Likes

Would be interesting to see earnings conference call. Rising steel prices have also contributed which may not be a long term trend. But happy to see, higher margin products picking up.

1 Like

Why is the company of this size continuously missing CSR expenditure?

1 Like

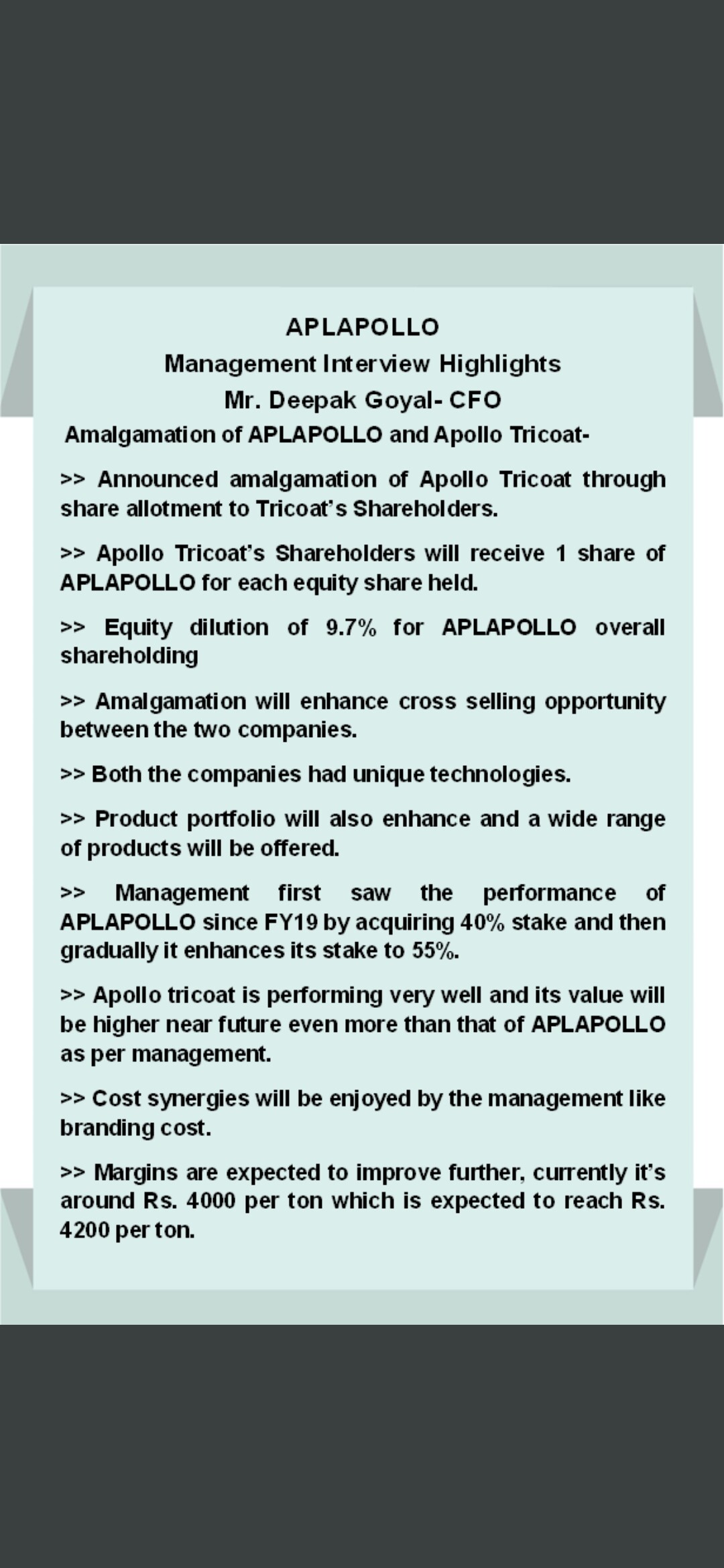

Merger of Apollo Tricoat and Shree Lakshmi Metal Udyog into Apl Apollo

Long term will create a strong company.

In short term, there is a gap in price of APL Apollo and Apollo Tricoat - so not sure if each Apollo Tricoat getting 1 share of APL Apollo is good for Tricoat share holders or bad for APL Apollo Tubes share holders - i say so as there is a big price gap between the two companies

It’s good for apl Apollo as apl Apollo on a higher pe is buying a stock with Lower pe

If market gives them same pe on new profit of combined business, it’s better for apl apollo

Apl tricoat didn’t lose anything but they might get a small rise even after the small profit of sp difference

2 Likes

Which concall / Interview is this from?

2 Likes