Results are out and looks flat. Though revenue is increased the deferred tax and net of tax expenses has minimized the PAT. Can someone please explain whether the PAT should be considered as PAT against march 2018 fig ? Considering the strong headwinds faced by shrimp industry in recent months I feel the numbers can improve in coming qtrs. Please share your views. ThanksApex Results.pdf (1.9 MB)

Expecting better Q2 and Q3 due to dolllar realization and weather changes back to normal

From Apex Q1 FY 2018 Call Conference Transcript

Industry updates:

We had mentioned in the last quarter’s conference call that due to a mismatch in the demandsupply,

prices of processed shrimp had started correcting from the beginning of the second half

of the fiscal year FY18 and more so in the last quarter of FY18. However we had also mentioned

that both demand slowdown as well as price correction has been largely arrested and we were

witnessing a gradual pickup in consumption starting from May/ June 2018. We would like to

point out that off late, the export prices have also started to firm up.

Now, on the raw material supply side, the price correction which is typically passed onto the

primary producers, coupled with inclement weather in the past few weeks might have led to a

slowdown in the availability of processed shrimp. However that seems to be a short-lived

phenomenon as the recent pickup in the shrimp export prices along with improving weather

conditions is building a favorable case for shrimp farmers. The farmers are again looking forward

to stock seeds for the next crop of this year. We expect things to normalize and growth to revive

from the second half of FY19 and continue going forward.

Apex Concall Transcript:-

Has any one figured out EPS calculation rationale by Apex? Could not decipher, how they arrive at EPS numbers every quarter. Like, in Q2 (declared a while ago), they have declared EPS 6.35. Net profit for Q2 is lower than Q2 2017 (yoy) and lower than Q1(2018) this year. But still, EPS is higher than Q1? Even, if we assume that company considers income after comprehensive income, this quarter profit is only marginally higher than Q1. Where as EPS difference is almost 35%? And, H1 EPS is even more puzzling. If we add Q1 (EPS-4.7) & Q2 (EPS -6.35), it comes to 11.05. Where as, the company mentioned in their filing as 13.13?

Am curious to know, if there has been a new accounting policy or is it an erroneous calculation by the company?

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=0257794a-78a2-46a7-9fa7-41ec7d9b5110

3 Likes

It seems that in Q2 they are using net profit for EPS calculation , for Q1 EPS they used comprehensive income.

So for half year EPS they recalculated Q1 EPS with net profit and added it to Q2 EPS.

Since in IPO in aug 17 they issued fresh equity so the calculation for that half year cannot be straight forward.

Apex Foods Ltd

Highlights of Q2 FY19 and H1 FY19 results

Key Highlights

- Construction of new civil construction work which got delayed due to the inclement weather is now moving on track and it is expected to complete major work by Q3FY19.

- Current Work Status

- Construction of the cold storage building has been completed

- The civil work of the processing building is in progress while the prefabricated structures are nearing completion

- Some of the equipment like cold storage units, ice makers, etc. are currently being installed

- The machinery room is also close to completion and the work pertaining to the power line has commenced

- Dormitories for workers and other staff members are under construction

- Company expect to start the trial production in Q4 FY19 and expect full capacity utilisation of 20,000 metric tonnes from this new plant to be fully available for the entire fiscal year FY20.

- CAPEX incurred for total planned outlay of almost Rs. 90 Cr, Rs.62.5 Cr has been incurred as of 30th September, 2018

- Results were lower because

- The incremental festive sales, especially to the US, which falls typically in the Q2 and partially in Q3 of fiscal year were lower than expected on account of utilization of most of the piled up inventory in the warehouses and also shortage of certain prices during the last quarter, impacted the volumes which could be produced

- As a conscious strategy company remain selective in executing orders which met company pricing and profitability.

- Upcoming facilities will enable company to add new products like Ready-to-Eat category which will cater the demand for such products in existing as well as new markets that company plan to foray into.

- Company target is revenue of 1400 Cr by FY20.

- Company expect demand to improve and capacities to continue to be optimum utilized. Company continually strive to reduce cost through backward integration and enhance product offering to customer via addition thereby improving profitability of the business.

Industry Updates

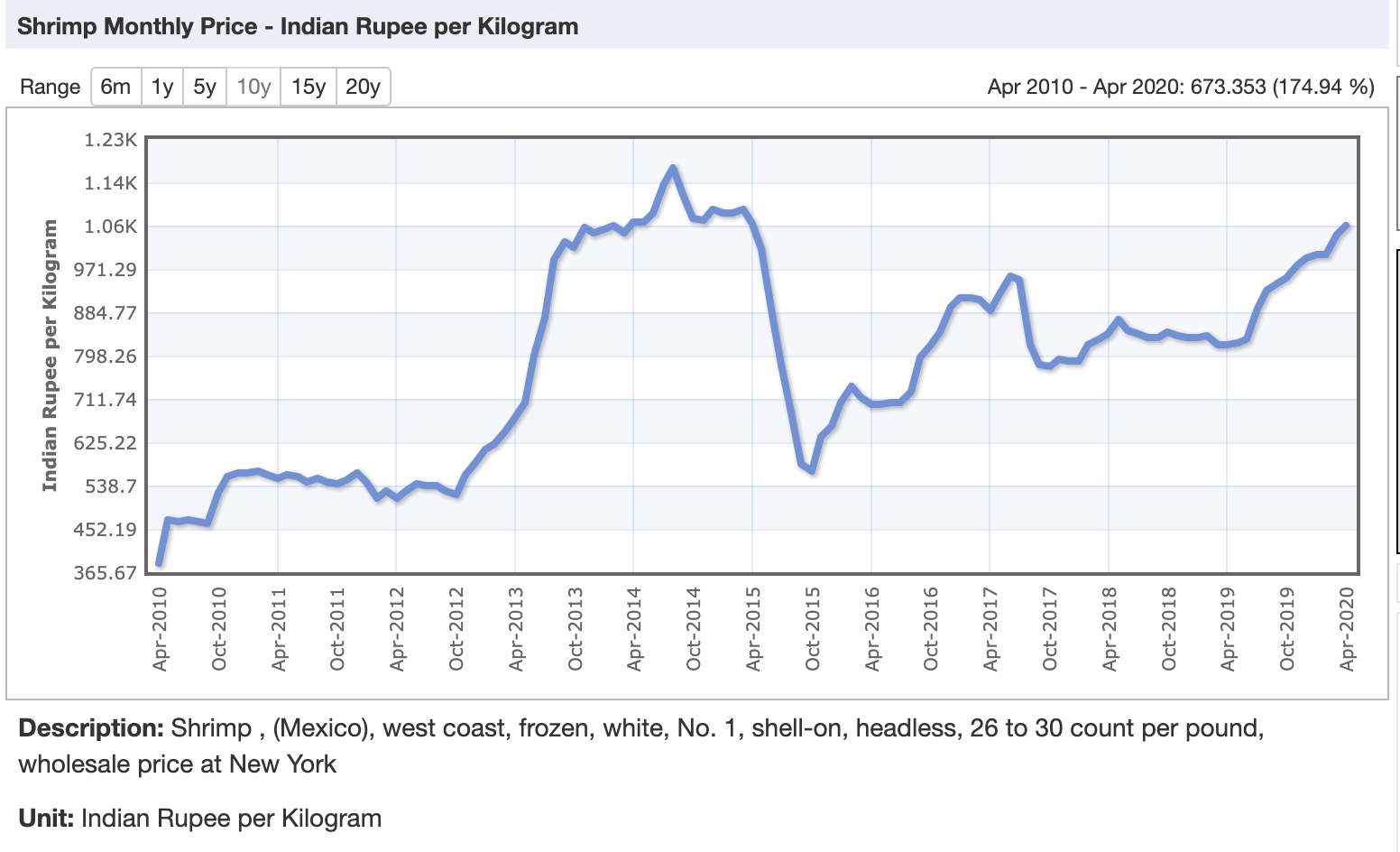

The shrimp prices which had hit the recent bottom in March and April of 2018, had started to inch up and is stabilizing at current levels. Similarly, farm gate prices have improved and the farmers have stocked seed for the winter crop, for which the harvests are taking place and would continue to take place over the next few months. Company expect market to normalized given the number of promotions being taken up by company end customers both in retail and food service segments.

Financials

-

H1 FY19

- Revenue stood at 508.2 Cr compare to 545.3 Cr s in the same period of last fiscal.

- Volumes sold were 7368 metric tons compare to 7598 metric tons same period last year.

- Average realization was Rs. 690 per kg versus Rs. 718 per kg in H1 FY18

- EBITDA grew by 3.9 % to 70.6 Cr compare to 68 Cr last year H1 FY18.

- EBITDA margin rose to 13.9 % compare to 12.5 % H1FY18.

- PAT grew by 6.2 % to Rs. 41.1 Cr as compared with Rs. 38.7 Cr in the same period of last fiscal year.

- PAT margin improved by 100 bps YOY to 8.1 % compare to 7.1 % H1 FY18.

- Share of European Union in the overall revenue mix increased to 25% during the first half of FY19 from 18% in the entire year of FY17, despite the strict quality norms and checks placed by the European Union authorities on Indian processers. Company aim to better the mix further.

-

Quarterly Results

- Revenue stood at Rs. 264.2 Cr as against Rs. 292.2 Cr in the same period of last fiscal year.

- Volume stood at 3688 MT compare to 3941 MT last year same quarter.

- EBITDA stood at 33.6 Cr compare to 37.9 Cr last year same quarter.

- EBITDA margin was stable at 12.7 % compare to 13 % last year same quarter.

- PAT stood at 19.8 Cr compare to 22 Cr last year same quarter.

- PAT margin was stable at 7.5 %

Q&A

- Did there was the demand muted in international market especially US ?

- Demand was muted for the incremental sales festive season which was supposed to happen did not happen and they were mostly being taken care by the existing inventories which were already piled up at the warehouses at the foreign locations. That is primarily in the US because the inventories were already more out there than what the market could absorb at that point of time or for the price level at which they are stored at. So that was the main reason where of course the volumes sold had reduced marginally.

- What would be the estimate in terms of inventory in the end market ? Whether it was high, low or medium ?

- The requirements of the market being taken care more by the product which is already available at the overseas locations than a new requirement arising for the finished product from the origin. So the demand at that point of time was already been catered by the inventories which were present at the destinations. So that means there was more product at the destination than what could have been absorbed or there was more product at a certain price levels which could be absorbed. That is the reason it took time and the customers, of course where basically buying only on need to basis to be precise. So, they were buying only those products which were not part of their inventories.

- What would be the reason for staff cost to be high on first half basis. First half that is for the first 2 quarters the staff cost is somewhere close to 24 Cr but this last year of 17 Cr. What could be the reason for this jump?

- Apart from adding more hatcheries and farm which company have done so far , is that there were quite a part of employees or workers who are working on causal labour basis or rather on a daily basis and company bring them on the rolls of the company. Because company need more people to work consistently because company want to have lesser turnaround of the manpower, not in terms of staff but it is mostly pertaining to workers. Because most of the staff are all very much part of the team; it is the workers who were working on casual labor basis. To be precise earlier it was part of the other expenses. They were the once who had got transferred into the employee that is the reason employee benefit it looks like manpower expenditure has increased. It is actually more of a transfer from the manufacturing expenses to employee related expenses.

- Does new facility will be available for full year to available for commercial production ?

- Yes for FY20 it will be fully available. Because there are certain certification and audits to be done and by end of march company will able to start . the first initial business once it is up and running in the fourth quarter sometime in February or March. So company can even first start doing for non-US markets for example. And as the audits and certification get over that is the reason it will be fully available for 2019-20.

- What kind of utilisation will be there at the first year ?

- Around 70 % utilization because company is going to look at phased wise transfer of utilization from lead facilities as of now. 6,000 metric tons will be available immediately and ready to eat product also. for which the customers have already started working with QA team on the specifications. So once company start the operation company will be able to start executing those orders and working more on those programs.

- Why company volumes were low in US against industry volume growth of 14 % in the quarter ?

- Company does not have any market share but there were certain sizes which were not available in fact the order book which was kind of buildup orders of pertaining from the Q1 are still to be executed in Q3 as on date because some of the sizes were difficult to be which the company has taken up in the best interest of the company So, those sizes which were not available and in order to the company not to just buy those sizes on at a much higher prices or rather reducing its profitability the company has decided to work with the customers to rather postponed those orders and execute them at a subsequent stage . So availability of supply is much more presently that is helping those orders to get completed. So, it is not really a loss of market share but more of volume drop mostly because overall sales of company customers who have been working with US had inventories and certain sizes which were working in smaller sizes was very less which made company to take a call to postpone those orders to subsequent dates. There is an lag of 30-45 days from the export to the import. Some of them are 60 days.

- Does company will able to grow volumes again at subsequent level ?

- Yes company expecting the volume to be made up in the subsequent quarters as company also have pending orders and company is working with customers and both retail and the food service segments lot of promotions are being done to encourage and rather to motivate consumers to eat more shrimp providing the value of shrimp products.

- Company is also working on newer products with customers offering so that company can show a difference e in value of newer products both in ready to eat and ready to cook category.

- So, those steps will definitely take care of increasing and maintain the volume as such similar to on par with what has been there last year.

- Why company receivable has increase from 38 Cr to 106 Cr and short term borrowings increased by 27 Cr ?

- As company have increase it market share in Europe from 18% of last year to 25% and still continuing to do that. The terms of payment with those countries with European markets primarily is on a much higher at a more number of days when compared to the number of days in the US. But company is working with customers to minimize it.

- What will be the receivable days in US ?

- 30-40 days

- What will happen to lease facility once company will start new facility ?

- Company had not finalized yet but idea is to shift all the operations and business to own facility and since it does not happen overnight, it will be transferred in phases because company need to bring the new facility into order and as it comes into order company will be moving all its operations into the new facility. However, it is more of a final decision will be depended on the market scenario, company order book and the demand growth in FY20 where company opt to keep one facility even if at a lower capacity to take care of such a demand.

- Does company is planning to export in new countries like South Korea ?

- Company have enquiries already coming in from South Korea as well as China which company will be opening up more because current capacities were mostly being absorbed by 2 major markets. Once the new capacity is available for company it will diversify the market like South Korea and China which is the major market right now for Indian shrimp products, taking up almost 30% of the India’s exports. So company is focusing on that market too. But company will be mostly focused into those markets to supply value added products whether it is in the raw form or the cooked but not base commodity products.

- What was the export incentive for the company ?

- 17 Cr

- Kindly give brief on the cost of goods increased by 17% quarter-on-quarter and other expenses reduced by 6 % ?

- Raw material expenses has come down. so the cost of goods has come down because of course also that also lot to do with the volume but also the sizes which company were handling the small sizes.

- Company volume is similar to previous quarter then why does cost of goods increased by 17 % so does it increased because of farm gate prices ?

- The main reason is farm gate pricing but also the sizes. Typically, the first quarter of the financial year will be dominated with small sized harvest typically, unless they have been stocked early. Company in first quarter was having mostly the smaller size. That is one point added to the volume. But then the other point is, of course the value the farm gate price also has stabilized. It has improved which is one of the major reasons for the farmers to gain confidence to stocking back their ponds again for the winter crop and of course making their decisions right now and the next month for their first crop of FY, the calendar year 2019.

- What is company guidance going forward on other expense ?

- The other expenses will, of course would be maintained around this level. But it is also depended on the sizes availability in the state of Andhra Pradesh. This year company had focused more outside Andhra Pradesh and also have been sourcing volume on par within the state of Andhra Pradesh. In second crop of 2018 company anticipate good volumes coming in within the state of Andhra Pradesh itself. So other expenses pertaining to transportation for logistics cost should be coming down in this year and in the last quarter. That is what based on the volume availability which is there currently in the state of Andhra Pradesh.

- How much capacity utilization looking for ready to eat category of 5000 tonnes ?

- Almost 90% to 100% to be precise FY20.

- Does the revenue of 1400 Cr guidance include the incentive part or not ?

- It include the incentive part.

- Did export incentive will reduce going forward or remain stable ?

- It will be 7-8 % but incentive has also got to do with premium and MEIS scrip sales which are there. So, that is one point and but with regard to the antidumping duty which has fixed is not going to be changing for now. So company will be maintaining this for at least 2 quarters.

- In current season what sizes company is looking for ?

- Farmer has started stocking so thereby the improvement has begun. And the sizes are typically the 40 count which was not that available around 2 months ago. Now that has started picking up and company is looking forward for a continuous supply of that size of 40 count primarily and 30 count because there was some issues with those sizes which will be available because now the prices for those sizes are attractive for the farmers also to grows and they have evolved their strategies for stocking in their ponds.

- Will be there any realisation improvement in next 2 quarters ?

- Company will not see significant improvement in the realisation . First point is on the unit value Dollar terms, of course based on increase in volume and value added that is in the ready to cook segment value added products definitely that margin whatever increase will be there that will anyway be there. But company also o have to keep track with regard to the realization in Rupee. Company have to keep a track on where the Rupee is also moving. For example rupee is marginally slightly appreciating on a day to day basis when company compare it to the depreciation which had happened around 45-60 days back. So, company had not seen a significant increase in the realization further for the current year in the present context of ready to cook products which company is exporting.

- Kindly elaborate on the antidumping duty ?

- Company have to pay 1.35 % till FY20 and company sales to the European Union and other markets are also going to increase. So, in the increased volume naturally the products which are sold to Europe and other markets are not subject to anti-dumping duties or any duties tariffs on company account. So more company increased the impact of the anti-dumping payment could be minimized a little bit based on volume being done on those markets.

- Did the export to China via Vietnam has been impacted due to some restriction from the Chinese people will impact Indian market from that front ?

- Actually in one way it was good that the for the Indian market it is good because Vietnam earlier the products going to China were being routed through Vietnam through their Hai Phong Port because they were the products being entered through Vietnam were duty free. Now the Chinese importers are visiting India. They are buying directly out of India and in fact India had started exporting directly to China. So, very soon hopefully in the next 6 to 9 months exports to South East Asia from India in generally even though company does not do any but exports to South East Asia will be coming down. That is Vietnam, Thailand and it will be increasing significantly to China because now China is allowing the imports directly from India even though there are some tariffs out there. It will be only in the interest of Indian Industry.

- Does company realisation is still declining ?

- : The realization per kg will be stabilized. Actually, in the third quarter prices have stabilized there was the prices have significantly corrected during the last quarter and the first quarter of this financial year. And they have increased and now they are actually stabilizing. So company e expect the realization to be more on to be précised on a flattish not significant drop and not significant improvement because now company is looking g forward for some bigger sizes which also have a higher value to be realized. That helps in having a better realization overall even though company would have all sizes also and the small size products.

- Company is also working to enter into China and south Korea So, those also those because of the lower realization lower unit value out there combined with larger value unit value realization from the western countries. It will pretty much maintain the same. There is no significant rise nor there was a marginal rise but that is kind of stabilized now. So, it is going to be around the same level.

- Will there be some kind of maintenance activity in existing plant ?

- Yes that will be looked at once the whole new facility comes in into utilization. Company have not planned it up currently because company cannot start any of such activity or any sort of rectifications until company have have the entire facility up and running. that is one of the reasons where even though company have 70 % utilisation in the new facility but there could be some marginal correction in the existing facility which will have an impact.

- How long will be the maintenance activity will go ?

- It takes 30-45 days approximately but still company don’t have complete plan for it/

- Did company is also looking into account which are the lean period which company want to factor in and go for the maintenance activity ?

- Yes that’s why on a whole year it will impact but it will get mitigated by taking the necessary measures.

- On 15,000 capacity of both company own and leased plant the staff cost as well as the other expenditure which company generally report on quarterly statement both put together works out to be around 180 Cr-190 Cr for FY18. Do company see similar kind of number ?

- Incremental cost would be there But it is not that it is going to be doubled. So, for example some of the team members who are required for the new projects or in the new facility are already with company. So, like those things people are getting trained up and the team is getting formed. So those, it is not that the entire costs will be doubled of course certain expenditure with regard to power and the electricity those will be of course increasing pro-rata to the volumes which are being going to be done. The cost will not get double in any manner it will be increased pro-rata with regard to the volume being done. It will be more of variable cost.

- What was the realization in raw material trend over last 2 quarters or maybe the one that company reported and as of today where it stands ?

- The realization for the half year in Dollar terms it was $8.7 was the realization. The raw material cost was an average of Rs 330-340 and today it is Rs 380-390. It is average of all sizes.

- In coming festive season did the mismatch of demand and supply will improve ?

- Yes. India is the largest India having almost a double of the nearest supplying nation to USA is Indonesia, the second biggest supplying nation which is at 96,000 metric tonnes while India is 175,000 metric tons. So, India has its presence well established in the US market. There is no doubt to that. It is just that there are certain products which they have been buying from China which are breaded and ready to eat products which have not been taking up much well from India until now but that is there India is going to look forward to mostly. Company is looking in the future of ready to eat products. In past there was 10 % duty started being levied on Chinese exports, sea food exports from China to the USA. And that is going to be changed to 25% from January 1st, 2019. So India supply to US will be major in a 9-month period it is 175,000 metric tonnes for the present year. That will be there and India’s products are the one’s which are occupying the most amount of shell space or plate space whatever table space one can call in the United States as far as that is concerned. And the demand supply, there were some issues with regard to supply, of course there are some issues with regard to demand too. So company think that this is the stable environment and company assume to consume more shrimps

- Going forward company have to meet with the protein competitor Whether it is poultry or the red meat whatever it is. So, right now the promotions are being done and pretty much the same thing is happening in Europe also. Company is also diversifying into other markets . So company is looking for US business to anywhere around 70% or lower while company will distribute the balance 30% and odd to other markets across the globe. .

2 Likes

Apex frozen foods Q3 FY2019

How come there is such a huge jump in sales/revenue numbers. Are they sustainable or some one time wonder. If anyone has some insight, please do share.

Sales are lower yoy and qoq. You are seeing 9Month numbers.

1 Like

They were trying to pull a fast one with the unconventional formatting. It is a never ending amusement.

I wrote to them after Q2 results seeking clarification, how come their EPS is always higher (some times they calculate EPS after adjusting OCI, some times they calculate on net profit). While they did not revert to me, but filed a revised submission correcting the error. I guess now, they would have forgot to include 9M FY 19 result column first and in the end, they had inserted it

Whats this comprehensive income? which has increased considerably this last qrtr as compared to Sep 18 qtr? And it did not increase EPS in that proportion. can someone explain.

Sorry for the ignorance

Comprehansive income is due to currecy depriciation additional revenue

Apex has gone below the IPO price for the first time. Results are poor, decreased revenue & profits. recievables are high…but borrowings have also reduced… Mine is a layman analysis… Can sombody summarize the Apex results from a different vantage point? future prospects etc…?

Is the shrimp industry as a whole going through a rough patch? & thats why Avanti & apex are battered to their all time lows… I read on the other thread that US shrimp imports are set to increase…

well this is Dec 2018 news.Refer Avanti Feeds thread. The latest US China trade stand off may help shrimp frozen food. There is some discussion on how china buys raw material headless shrimp from India via Vietnam (& now directly) & it processes & exports it as frozen food… that business will be impacted going forward owing to US import tariffs & India stands a chance to gain from this situation but the industry here has to upgrade from raw shrimp to processed foods… & I believe Apex is better positioned than Avanti in this regard. However Avanti & others are also building such processing capability… so overall I believe this is positive news for industry.

Disc: Holding small qty since ipo

apex seems to be resilient even to the global macros considering that US-Iran war is indeed a possibility and still Apex is continuing its slow upward march. I am wondering what is the right value for this stock?

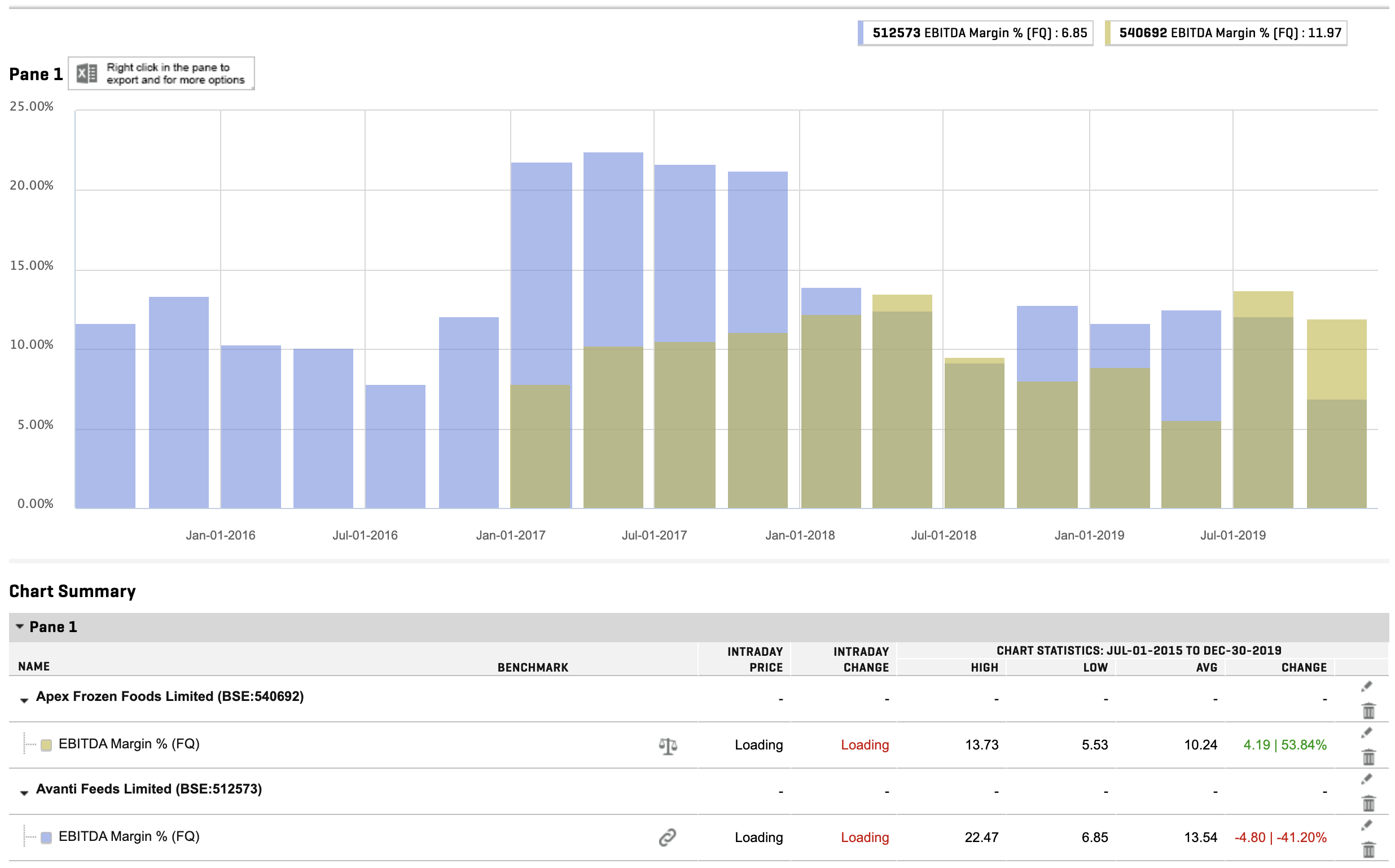

The shrimp prices are pretty good. There is no reason why the margins should decline in the December quarter for Avanti or for Apex. Why are the margins so volatile and pretty much all-time low?

Further, if you look at the EBITDA of the two companies Avanti and Apex, it’s a picture that I just can’t understand, the EBITDA margin was significantly higher for Avanti till Q3FY18, and Apex caught between Q4FY18 to Q2FY19, and then again Avanti was higher and now Avanti is significantly lower. I presume that the realization of the product can’t be very different for the two companies or at least have to correlate. Also, the cost of production can’t change significantly from quarter to quarter. Can anyone explain this?

Appreciate any insights. Thanks.

Disclosure: I have no exposure.

2 Likes

Both are in same sector with different products and hence the variation in margins.

1 Like

Hi Folks,

Recently ICRA and Crisil had raised some concerns regarding the non availability of certain information from the company. They have mentioned that the company hasn’t responded after continuous follow ups. Do you feel this raises a red flag from the Corporate governance point of view or am I missing something? I have referred to the announcements section from Screener.in.