Hi Deepak, from where do you track monthly shrimp prices? I am thinking of investing in Apex and wanted to track this info as well. Thanks!

I’ve been thinking of investing in Apex myself. Whats interesting to me is the recovery story of their markets broad, chief amongst them America and Europe.

An additional point of interest is there increased capacity in both the shrimp processing capacity and the increased focus to the Retail segment via their RTE segment and that capacity doubling in the current financial year. They have also pared down their farming (owned) activity and just ploughing all their efforts into processing in the future. That shows for a lot of focus on Mgmts part.

Plus you have the recent PLI announcement for Food Processing of 10900 crores. Debatable as to when that starts showing benefits, since it requires filing with the govt and then payments coming back in the system.

Marine exports as of March (no data available for April) shows recovery as compared to many previous months.

Plus I have always liked the good ROCE numbers this company has managed over the years. I see this as a post Covid recovery story (6-12 months) and not a long term bet. Will look forward to see the AR filing, but given that SEBI has allowed time uptil June for filing last years performance I guess its going to be little longer we see that come through

Welcome anyones view on the above

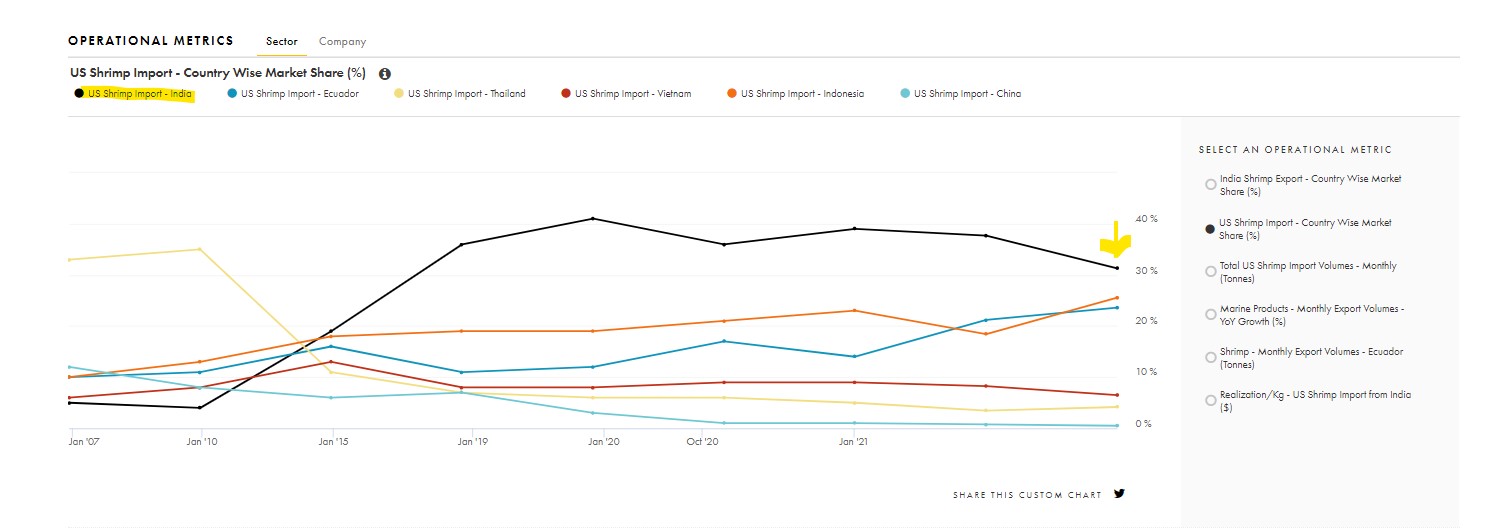

Apex is on my watchlist as well. For me Apex growing its volumes is a function of two variable (1) Apex growing its marketshare in exports amongst domestic suppliers (2) India growing its marketshare in the US vs other countries.

Point (2) is my key concern since India seems to be losing marketshare in the US to other countries. We have lost 1000 bps marketshare in 4 months

Source:Tijori

Link: Tijori Finance

Agreed, however my understanding is that the drop you correctly cited is owing to logistic issues atleast in the near term thanks to Covid.

@pennywise - Did you happen to do a DDM and/or DCF valuation?

I came with a share price around 200-215. I am not an expert so I can be inaccurate.

I dont usually do DCF as such, DCF according to me would work for more stable companies like Nestle or Asian Paints which are not on my radar. My only monitorable for Apex is will it be able to 5X volumes in the next 10 years from TTM values. If it does that I believe returns will take care of itself.

This stock looks most ignored one in current environment though:

^ capacity expansion, last year worked on one third of the capacity hence huge operating leverage available

^ integrated player

^ high ROCE business

^ undemanding valuations

^ best opening up trade since US has opened up

^ as per CRISIL, India will increase its Shrimp export by 20% this year

^ increase in realization is also on the anvil

Negatives:

Slight cyclicality

Looks like a quintessential opportunity wherein capex is over, depressed profitability and huge demand undercurrent. May be positioned where Deepak Nitrite was 2 years ago.

Disc: invested

3 Likes

Apex has expanded total capacity to 29240 MTPA and cold storage of 3,500 MT

New plant at Ragampeta: capacity of 20,000 MTPA and cold storage of 2,500 MT.

(In FY 20 the company discontinued the leased facility of 6,000MTPA and commenced a new processing plant at Ragampeta).

New plant includes 5,000MTPA capacity for ready to eat product. Company planning to increase it to 10,000MT.

Kakinada plant : capacity of 9,240 MTPA and cold storage of 1000 MT

Apex frozen foods Q4FY21 results were decent with revenue growth of 26% to 184cr with EBITDA growth of 14% to 21 cr(without export incentive during Q4). After stagnant revenue during the last 3 years and depressed return ratios, finally things seems to be getting better for Apex frozen ltd.

During Q4 concal management has guided for shrimp sales of15,000 MT for FY22 (they did 11,701 MT sales in FY21) with capacity utilization of 50% as export demand picks up with the opening of the food service sector in the USA and good retail demand.

Increase in revenue share from value added ready to eat/cook products (23% in Q3, 21% in Q4 and 15% for FY21) leading to realization improvement. Company has an order book in ready to eat products and is guided for 60% capacity utilization with better margins.

Company focusing on core operation of shrimp processing and export. Its exiting shrimp farming business except for company owned farm land of about 120acre.

Risks to watch:

Raising inventories and receivables leading to increase in WC cycle( receivables are doubled to 154 cr vs 79cr)

Ongoing shipping/container issues, if persist longer can further worsen WC(shipping days have increased to ~50 days)

Geography risk: more than 80% revenue is from the USA. Any surge in covid cases may lead to reduced business from restaurants.

USFDA risk due to any possible contamination with microorganisms like salmonella.

Increase in shrimp prices may lead to margin compression.

Risk of disease outbreak causing low availability of shrimp.

Uncertainty over export benefit scheme to be announced by Govt.

Discl: invested

5 Likes

Anyone know why the share dropped 20% on 16th August and has been on downfall ever since?

Q1 performance was bad and profit was down 60% On YoY basis.

1 Like

Shipping Costs have Finally Started Coming Down.

https://www.ft.com/content/b6bfe708-3f2d-491b-8887-650c3e4f1ec1

Have anyone short note on Q2 FY22 concall ?

Please send it.

Con-call summery(Q2FY22)

• Global demand for shrimp continues to remain strong with large parts of the developed economies beginning to return to normalcy.

• Company are seeing a robust demand both from the food service sector, the HoReCa clients as well as the retail clients. The average realization increased on account of better product mix and stable shrimp prices globally.

• Additionally, company business with the European Union has witnessed improvement this year which is basically a higher realization market when compared to markets like China.

• U.S. market specifically both the food service sector and the retail sector have opened up and the demand has been strong. Company are having products which are completed, and still waiting for equipment support from the shipping lines.

• company have not started the ready to eat products to European Union because the regulatory approval for the new market for ready to eat products, which is a delayed trigger between the government authorities of the EU as well as the Government of India.

• With regard to China, shipments for the past quarter were zero. With regard to various trade barriers related issues as well as company focus to utilize the current capacity mostly for the US and new markets in the present demand supply situation.

• Company would of course continue to look at the Chinese market when the market is in a favourable condition to the company, for now, company focus continues to remain mainly on the US and the EU market.

• Capacity utilization of course is more dependent on the availability of supply of the product. Company goal also for the whole year is looking at 50% plus so that is the minimum, which company were looking at but of course subject to supply conditions. So, company look forward for supply to be improving if not in the Q3 maybe by Q4.

• India still continues to be the number one supplying shrimp nation in the world as of now and because of the availability of the large-scale farming which happens across the country and newer areas also being added and there is no immediate threat for India to lose its market share to somebody else.

• Ecuador has become relevant only in the year 2021 in the US market. That is primarily because of the issues(covid) being faced from China. Ecuador’s primary market for the past seven to ten years has been China and it is only because of the restrictions from China in the year 2020 – 2021 that has made it focus on the US.

• Is Ecuador a threat to India? - Not really because India’s production which company get is at a much larger scale compared to Ecuador. Yes, Ecuador continues to have an advantage of shorter sailing period to the US market when compared to India which is having anywhere between four and six weeks of sailing period while the Ecuador in shipping industry has to deal with only with one week to the US market.

• It is a livestock industry and disease also playing its role, weather conditions, climatic changes all these play a role with regard to shrimp aquaculture across the country and having seasonal factor.

financial performance

• Despite the second wave of COVID-19, the capacity utilization during the first half year of FY2022 improved to almost 54% of overall capacity of 29240 metric tons as against 41% in the full year of FY2021.

• However, due to the logistical issues for the past few quarters, which translated into lack of container availability.

• Company volumes sold was restricted to around 86% of the production, dispatches of sales of 6804 metric tons in the first half year of FY2022.

• The ready-to-eat sales formed almost 21% of the overall shrimp sales in the first half of the current fiscal, which is a significant increment over the 15% share in FY2021.

• The average realization in Q2 FY2022 improved by almost 8% to 10% when compared to year-on-year as well as quarter-on-quarter on the back of improving product mix and better global prices of shrimp.

• Overall availability of containers is improving slightly, company are still having to pay very high premium rates for reserving the containers for shipping finished products.

• The PAT for Q2 FY2022 stood at Rs.220 million, lower by 13% year-on-year but growth of 56% quarter-on-quarter.

• As a result of improving product mix and stable prices company total income increased by 2.3% on year-on-year basis and 18.6% on a quarter-on-quarter basis to Rs.2699 million in Q2 FY2022 and by 2.6% year-on-year to Rs.4974 million in H1 FY2022.

• Company have booked export incentives of Rs 3.53cr. in this quarter.

3 Likes

I have been working more on the shrimp sector and it seems that finally, the sector is making a come back after a challenging period of last 2-3 years due to multiple factors one after another. If the recent growth trends sustain, I think the valuations are very attractive for almost all the players of this industry.

Interestingly Apex management seems very confident in the recent concalls and AGM and has been guiding for a high growth this year with much better margins. It would be great if we can do more work on this and the sector.

The stock price have also been dull as people would have lost interest after multiple dis-appointments.

Disc: Invested in family and client acs

23 Likes

For anyone wanting to go through concall of q4 fy 22, transcript

apex frozen q4 fy 22 concall.pdf (898.1 KB)

attached here.

3 Likes

Here are my thoughts-

On the management-guided volume growth of 60% +, I sense a few systemic concerns -

- Capacity was never utilized at these levels and might involve a lot of new learnings, constraining volume increase to such an extent.

- Availability of the suitable raw material crop - Management stressed this multiple times in the conf call and I infer that they have some concern around the suitable sources of supply.

- Do not see any solid reasons for Ready-to-Cook demand, which is 83% of the current capacity. In the conference call, the management sounded confident about better usage for the ready-to-eat demand (only 17% capacity).

On the cost side, most of the costs are variable and shall increase in line with the volume growth. Going by the conf call commentary “The current freight charges, I think we shall speak at least to the extent of USA. We have signed new service contracts between USD $14,000 to $16,000 from major destinations, compared to the previous quarter or last year’s contracts were between $9,000 to $11,000.”, I anticipate freight cost will be way higher compared to the last year.

If freight cost escalates even by 25% over the FY22’s freight cost, topline growth of up to 25% in FY23 would not change the bottom line. Anything above that might improve PAT but way lower than the sales growth.

It seems that Q1 and Q2 are their major quarters. I will be on the lookout to see how Q1 turns out.

2 Likes

Please correct me if I am wrong.

They are doubling ready to eat capacity and will be in utilisation from September. As realisation is 12-15% higher should support bottom-line I guess ?

Any way freight cost is at peak so I guess it should go down from here based on management commentary of easing out in next few quarters.

2 Likes

Per the latest conference call, booked Shipping line costs in Q1 were 35% higher. Since management expects substantial volume in the current year, I assumed that they would have made some forward contracts at similar rates to avoid shipping delays. Their maximum volume will happen in H1. Also, management expects the cost to ease out in the next few quarters and that being an open statement does not imply immediately. Hence, I guessed that freight costs will remain elevated.

Margin accretive RTE business volume is small and there are other costs that will flare up such as electricity cost that management admitted in the latest call.

Above all are just opinions. Reality will follow its own random walk!!!

6 Likes

World’s shrimp production to surpass 5million metric ton this year which is 10% growth over previous year. India’s estimated growth rate is around 9.5%. Also Ecudaor’s production is growing at much higher rate around 25-30%. Also Technological advances in shrimp production should reduced cost for Ecudaor and their hold on US market is increasing. With supply chain constraints and huge production globally there will be margin pressure in shrimp export in my opinion.

I am not an expert but generally huge supply is negative for any sector. With this kind of production can 2022 be starting of another positive cycle of this sector? Views invited

6 Likes