Q4FY17 Concall Transcipt: http://www.apar.com/pdf/financedata/Concall-Transcript/2016-2017/Concall%20Transcript%20Q4FY17.pdf

Overall

Guidance for FY18 remains muted as this would be a year of consolidation for transition between different manufacturing bases, newly commissioned plants getting traction and GST implementation settling in. Management is fairly optimistic on all 3 business fronts - Conductors, Transformer Oils and Cables doing fairly well in FY19.

The mega capex of Rs 550 crores that was invested over the last few years to build capacities in new generation of higher value added products across the 3 businesses i.e. High temperature conductors, high voltage transformer oils and automotive oils and then some of the specialty cable products (Defense, Railways) now started to yield results as seen in FY17.

Capex Commissioning:

• Conductor plant in Jharsuguda started production in September’16 and Q1FY18 should see a 70+% utilization of that plant.

• Capacity expansion for high voltage power cables commissioning in the first half of FY18.

• Restructuring of the manufacturing of low voltage instrument and control cables from 3 locations to one,

• Rs. 100 crores of CAPEX in total for FY18, but then we expect a fairly sharp drop in CAPEX for FY19.

• Interest outgo to remain at similar levels of with 80 Cr of Interest and rest in forward hedging costs. Additional forex fluctuations to be booked at actual.

Growth Outlook

As FY18, marks the beginning of the 13th plan, the T&D investments are expected to be about Rs. 2.6 lakh crores with a sharper focus on higher voltage transmission lines. Power grid is also trying to spend approximately more than Rs. 1 trillion over the next 4 years to expand various T&D networks. GST implementation which is likely to kick off from July 17 will definitely have positive impact over the next 5-year period.

Conductors

• Conductor business reported growth in profitability where in EBITDA per metric tonne post Forex adjustments grew by almost 60% to Rs. 11,882 from Rs. 7,469 per metric tonne.

• This was on account of more profitable orders executed in the year and the increased contribution of high efficiency conductors which has increased to about 11% for the year compared to 6%, a year ago. Target is to reach 20% high efficiency conductors by 2020.

• Apar awarded the best company award for high efficiency conductors by PGCIL for the year 2016-17.

• Executed some fairly challenging re-conductoring projects in Kerala, Telangana and various other states.

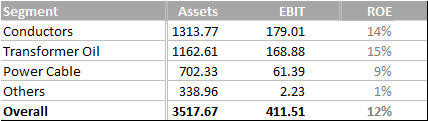

• The segment revenue is at Rs. 2,251 crores and exports contributed approximately 39% of sales.

• Order book stands at Rs. 1,519 crores as of FY17 end with exports comprising 48% of this order book.

• Domestic demand was slightly subdued and some of the projects awarded did not result in orders

• Increased competition observed in the last few months with some of the participants actually passing on expected GST benefits. Be risk averse to lose short term business is better, than risking all.

• All approvals in place for the newly commissioned plant in Jharsuguda, Orissa. So once GST is in place, this can can ramp up 100% plus increase the capacity at Jharsuguda

• Company can extract a maximum benefit of almost about Rs. 4,000-5,000 per metric tonne, if one were to produce the product in Silvassa and sell it into that part of the country versus producing it directly in Jharsuguda and supplying it into east and central India. This will give them an edge over competition.

• For the new plant, target of approximately 50,000 metric tonnes worth of volumes in FY18, if this is achieved plant will break even in the first year of its functioning.

• The Jharsuguda plant would focus almost entirely on domestic and the Silvassa plants would focus

on certain parts of North West India and export.

• Seeing quite a lot of interest coming from the state utilities on HEC conductor. This business should definitely see higher traction in the coming years.

Transformer Oil

• Coming to the specialty oil side, the consolidated revenues came in at Rs. 1,699 crores.

• The volumes grew by about 4% for the year to volume of 352,655 KL and this was led by growth in the domestic transformer oil segment, transformer oil exports, rubber process oils as well as we saw a 6% growth in automotive oils in terms of volume terms in spite of fairly large dip that took place in the third quarter post demonetization.

• The EBITDA per KL after Forex adjustments for the year came in at about Rs. 4,931 per KL which is lower than the previous year which was at Rs. 5,439.

• Hamriyah, Sharjah plant is ramping up. Seen considerably increased utilization of capacity now in the month of April and May. Target to breakeven in FY18…

• Company aimed for integrated certification (ISO 9001, 14001 and 18001) of ISO and this forms actually a precursor to be able to bid on a lot of business with some of the utilities overseas.

• The automotive lubes segment delivered a volume growth of about 6% to reach 24,893 KL. The growth was limited on account of demonetization. Double digit growth was seen in the first half of the year.

• Expect volume growth to come in from the UDAY projects which are showing signs of picking up now and uptick in the sales that are taking place to the higher voltage transformers.

• The 12th 5-year plan has exceeded target in 400 KV and below but it has slipped on 765 KV and above. Only 70% was achieved. So that spillover will be executed in FY18 and early part of FY19. So given this, increased volumes can be expected in this segment.

• In transformer oil, some of the increased growth will happen at the lower end which is at the distribution transformer side coming out of the UDAY related project.

• Management has guided for lower margins, as some inventory recalls are expected in Q2 with respect to GST.

Cable Business

• The cable business has delivered its best performance to date. Revenue growth came in at 28%. The EBITDA margins at 8.6% for FY17 compared to 5.7% for FY16.

• The power cable segment continues to be very competitive. Some of the niche segments, where Apar has leadership saw better margins.

• 20%+ growth is expected in FY18. Higher demand is seen from the non conventional energy segments which are solar and wind. The power cable segment also is showing increased demand from implementation of UDAY and more traction taking place in both Defence and the Railway side of the business.

• The capacity that is expanded in FY18 will be good to actually do about Rs 1,250 to Rs 1,300 crores worth of production.