Apar Industries is involved mainly in the power ancillary business - Conductors, Specialty Oils (mainly transformer oils) and Cables.

Conductor Segment

• CO generates 45% of revenues from conductors

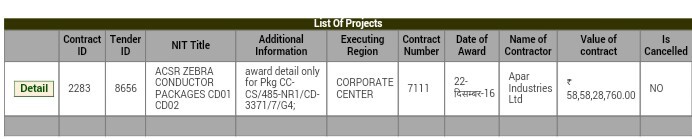

• Apar has a market share of 23% in the domestic market

• One of the top five manufacturers of conductors in the world. Largest exporter of conductors from India.

• Estimated conductor market size in India is 7500 cr growing at 13%

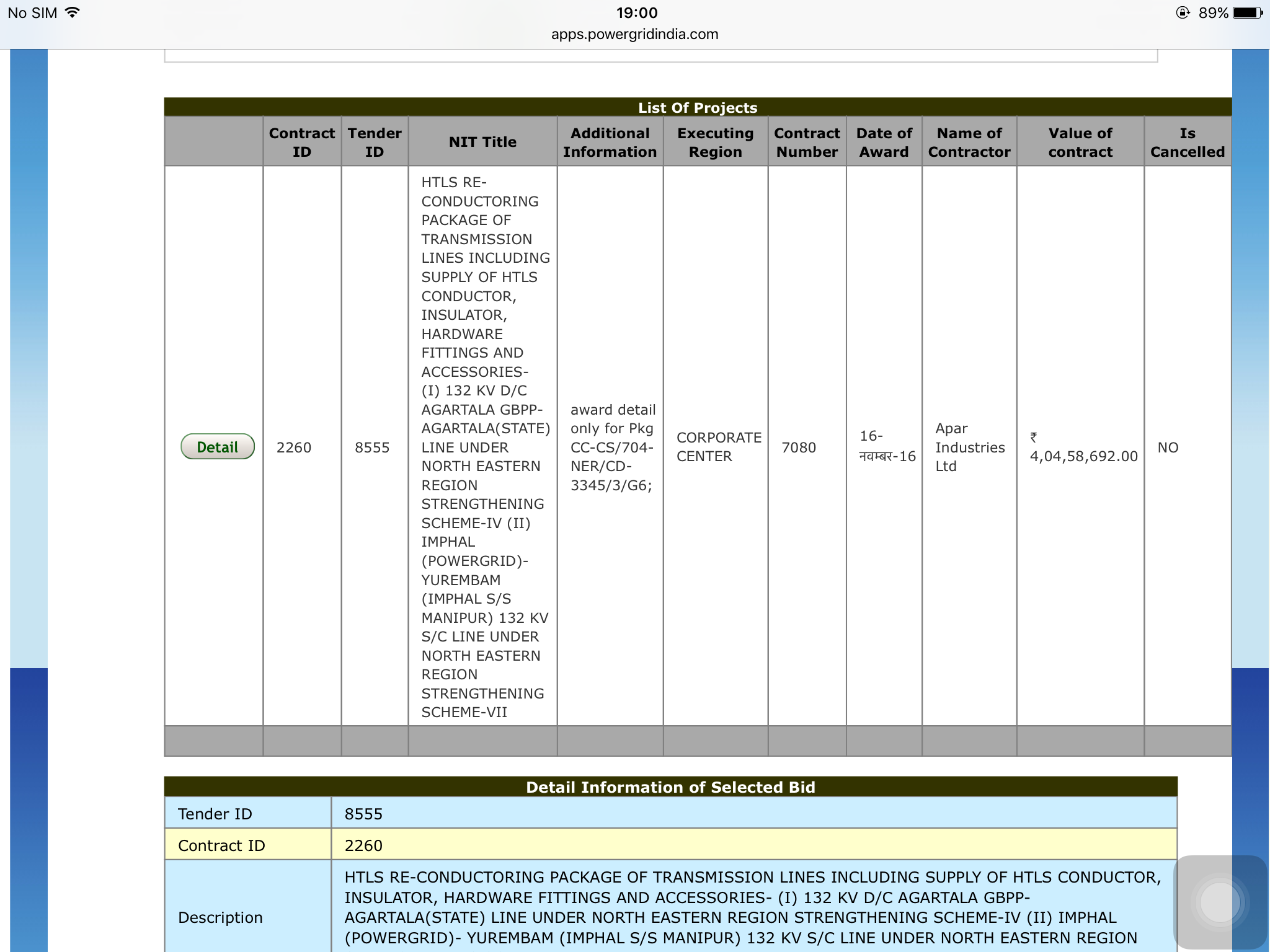

• First turnkey project for High Temperature Low Sag (HTLS) conductors was successfully executed. It is a higher margin product compared to conventional conductors.

• Co is expecting a growth from 2% of revenues to 7.5% of revenues in FY16 in HTLS

• Co is expanding capacity by 30,000MT. Commercial production is to start by September 2016

Specialty Oils

• Domestic market share of 45% in transformer oils

• Fourth largest transformer oil manufacturer in the world and exports to 100 countries

• This segment is dependent on crude prices. Fall in prices depresses topline revenue.

• Shift in demand to 765KV & 1200KV transformers driving demand for higher voltage transformer oils

• Co has 2 manufacturing units - Rabale (222,000 KL) & Silvassa (220,000 KL)

• Co has setup a R&D center in Rabale

• Commissioning a new plant at Sharjah which will start production by Q3 FY17

• Tie-up with ENI of Italy from 2007 to produce auto lubricants

Cables

• Co has 2 manufacturing sites in Umbergaon & Khatalwada - Gujarat

• Domestic market sales is 78% and exports comprises of 22%

• Co moving away consciously from HT LT cables due to low margins and moving into Elastomeric & E-beam cables

• National Optical Fibre Network (NOFN) will create a network connecting all gram panchayats

• 3G & 4G rollout will also add to the requirements

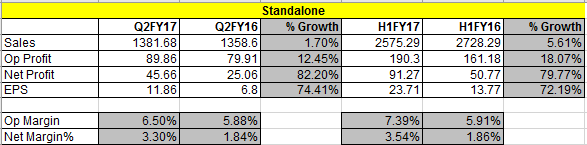

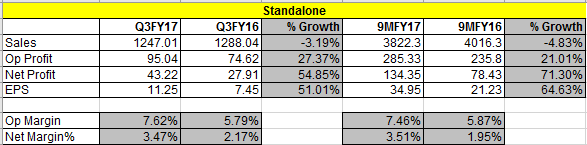

Financials

Market Cap.: 1,767.58 Cr.

Current Price: 459.15

Book Value: 196.60

Stock P/E: 20.52

Dividend Yield: 0.76%

Face Value: 10.00

52 Week High/Low: 541.95 / 321.00

Dividend Payout Ratio: 28.14%

Debt to equity: 0.78

Price to book value: 2.34

Sales growth 5Years: 20.19%

Profit growth 5Years: -7.16%

OPM: 6.19%

NPM last year: 0.96%

Return on assets: 7.97%

Return on equity: 7.66%

Return on capital employed: 18.72%

Risks

- A delay in power distribution sector turnaround may impact the profitability of the company.

- Exports may get impacted due to volatility in currencies

- Speciality Oils are derivatives of crude hence any sharp price movement in crude can impact the company

Opportunity

With a turnaround in the power distribution business and possible benefits from the UDAY scheme, all the segments are likely to benefit. Apar has a good potential to benefit from this trend.

Company website for Annual reports and Concall transcripts - www.apar.com/financials.php

Screener Financials - https://www.screener.in/company/APARINDS/

Disclosure:- I have a tracking position in this stock with the intent of adding based on future progress.