149cr QiP with 10% of it as fundraising expense raises some doubt. Usually for IPO its in 3-7% range, Qip should be much lesser. Incremental 4cr (not mentioned in the offer document) towards Jajodia Equity Advisors Services Limited. Not much info around, unusual for someone who gets 4cr out of nowhere.

#Invested.

4 Likes

4 Cr for QIP of 149 Cr is 2.68%. That’s not very off from the normal. Btw what’s the source of this expense info?

Suppose he redirected ₹10 Cr or ₹14 Cr through overpayment to the issue manager, while another promoter infused ₹15 Cr by buying a subsidiary with no revenue. In this case, funds flowed out and returned, resulting in a net impact of zero—assuming the disclosures are accurate.

Very basic question : I am not able to understand why would promoter buy an subsidiary with no revenue for 15 cr.

Why have they not issues more preferential share for the same amount?

CFO resigned, large KMP restructuring. I don’t know what these guys are upto.

1 Like

Manoj Sharma, CEO of Annapurna Swadisht bought shares worth 48.5 lakhs on 13th March 2025

1 Like

CFO is moving internally so not a red flag per se

Won’t read much into this. Digging deep, Ravi Sarda and current CFO pawan jaiswal had sold 4cr worth shares each in 22/23

1 Like

The growth story of Annapurna is been fabulous and their vision gives an optimistic outlook but the loans and advances of 28.5 cr (FY 24) and 61cr (Sep 24) is worrying. As per FY24 AR, out of 28.5cr it has given a 3.4cr loan to a corporate and another 7.7cr being categorized as other advances. Wondering what the split for 61cr be?

Would appreciate if some colour is thrown on this.

Comparing Similair Items on blance sheet of FY 24 and Q2 FY 25:

| Particulars | Mar 31 | 2024 ( Lakhs) | Sep 30 | 2024 ( Lakhs) |

|---|---|---|---|---|

| Short Term Loans & Advances | 2858.21 | 1615.52 | ||

| Other Current Assets | 846.13 | 2090.81 | ||

| Long Term Loans & Advances | 994.16 | 4645.66 | ||

| Non-Current Investments | 218.9 | 208.9 |

- Short term Loan and Advances includes: Mar 24 :

- Capex Advance : 595.53L

- Purchase Advance: 834.67L

- Loan to Body Corporates: 332.12L

- Darsh Advisory :380.58L

- Other Advances: 775 L

Q2 FY25: No breakup given

- Other Current Assets includes: Mar 24

- GST Input:372.30L

- Stock of Coins :448.48L

- Salary Advance & Imprest :20.00L

Q2 FY25: Bifurcation not provided

- Long Term Loans & Advances includes : Mar 24: Primarily capex-linked advances

Q2 FY25: Item wise details not available

From above it may be noted that:

1.Company has given loans to Darsh Advisory and a Body Corporate. Inaddition, details of other Advances on Rs 7.74 Cr( FY 24 AR) is not given.

2. There appears a recalssification from Short Term to Long term .

3. Hugh Spike in longterm loans and advances in Sept 24 (Q2 FY 25) may be linked to acquisiton of Madhur Confectioners Pvt Ltd. , ( Acquistion in Nov 24), but difficult to say with certainty or partly may be due to higher advances/ loan for expansion.

Disclosure: Invested and bias

2 Likes

Any comments on why the shares pledged have increased so much?

Ritesh Shaw (Promoter group) owns 1/3rd. Pledges might be coming from his part for Warrant subs amount of 13cr and an additional 40cr to be paid for exercising them. 83cr QIB at rs. 351 a share.

Biger issue is Cash flow, Merger was funded by QIP at rs 400 dilution, now additional capital raises for a FMCG for BAU is suspicious.

Disc: Big value bet.

1 Like

Being a FMCG Company,how come the CFO is negative for the past 2 yrs?

Something is very wrong in this company.

2 Likes

Annapurna promoters pledge has increased to 53% in March 25a sudden rise from 4% in Sept 24 . Management doesnt do any concalls so hard to understand their strategies or logic in some strategies

1 Like

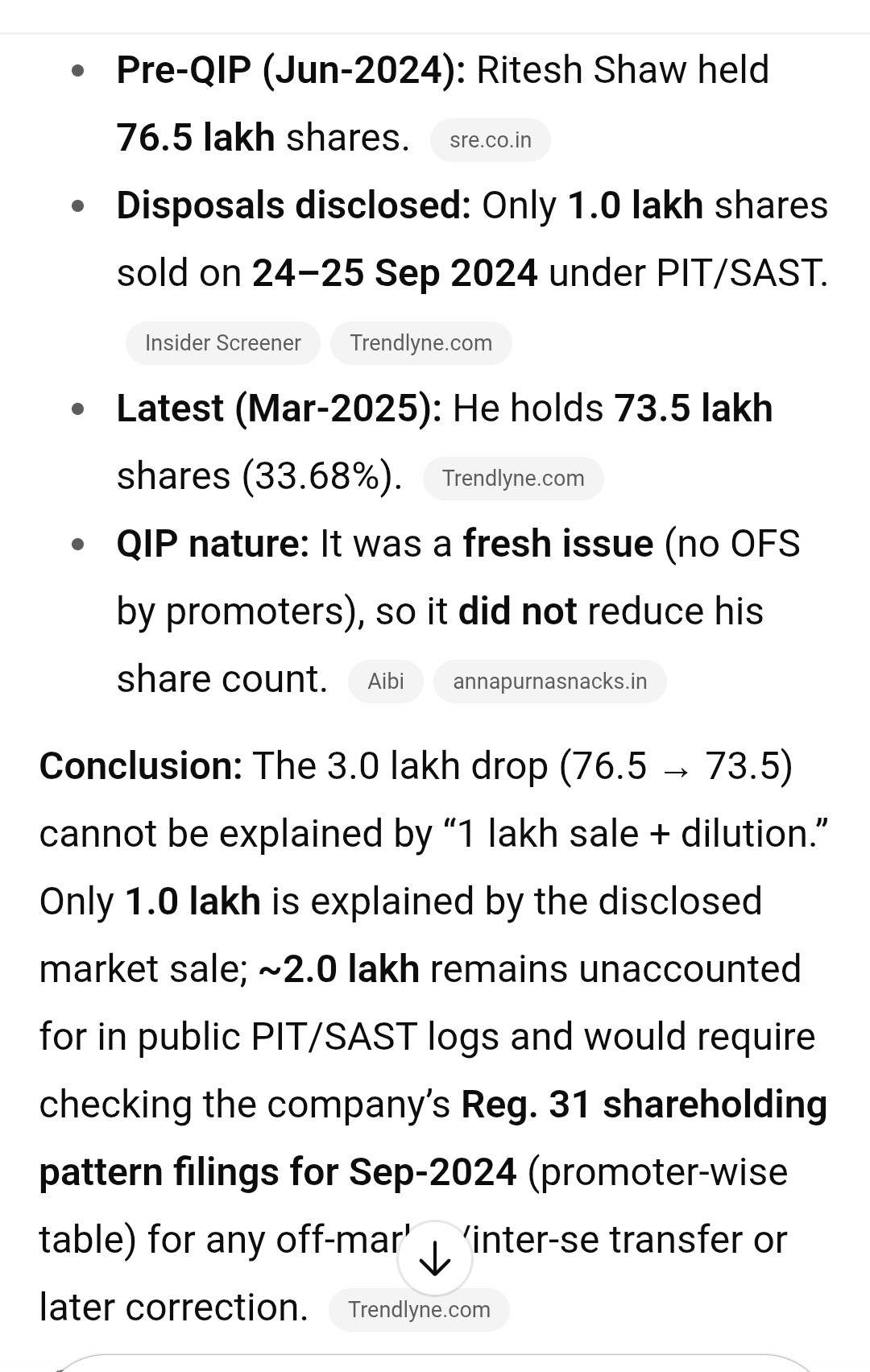

I was trying to understand the discrepancy in the shareholdings of Ritesh Shaw. If any one can explain I would be thankful to him.

1 Like

the sales have almost went up 4 times in the past five years.What could be the reason.they say that their western foods department is seeing a lot of growth and also noodles.Any ground idea as to why consumers like these products in east and north east india.

Stock seems promising.Imagine if it can double in a few more years.

My view is slightly negative about this company. I did slight scuttlebutt on this company because my native place is in Asansol where the company has manufacturing plants and business place. I got so many negative inputs about this company and its promoters. Want to warn retail investors but If Anybody or Admin of this forum finds my post objectionable, my post could be deleted.

2 Likes

Please share whatever you know about this company which is not known in general.

1 Like

@binay1702 Please provide more info on this.

1 Like