ANDHRA PETRO

|

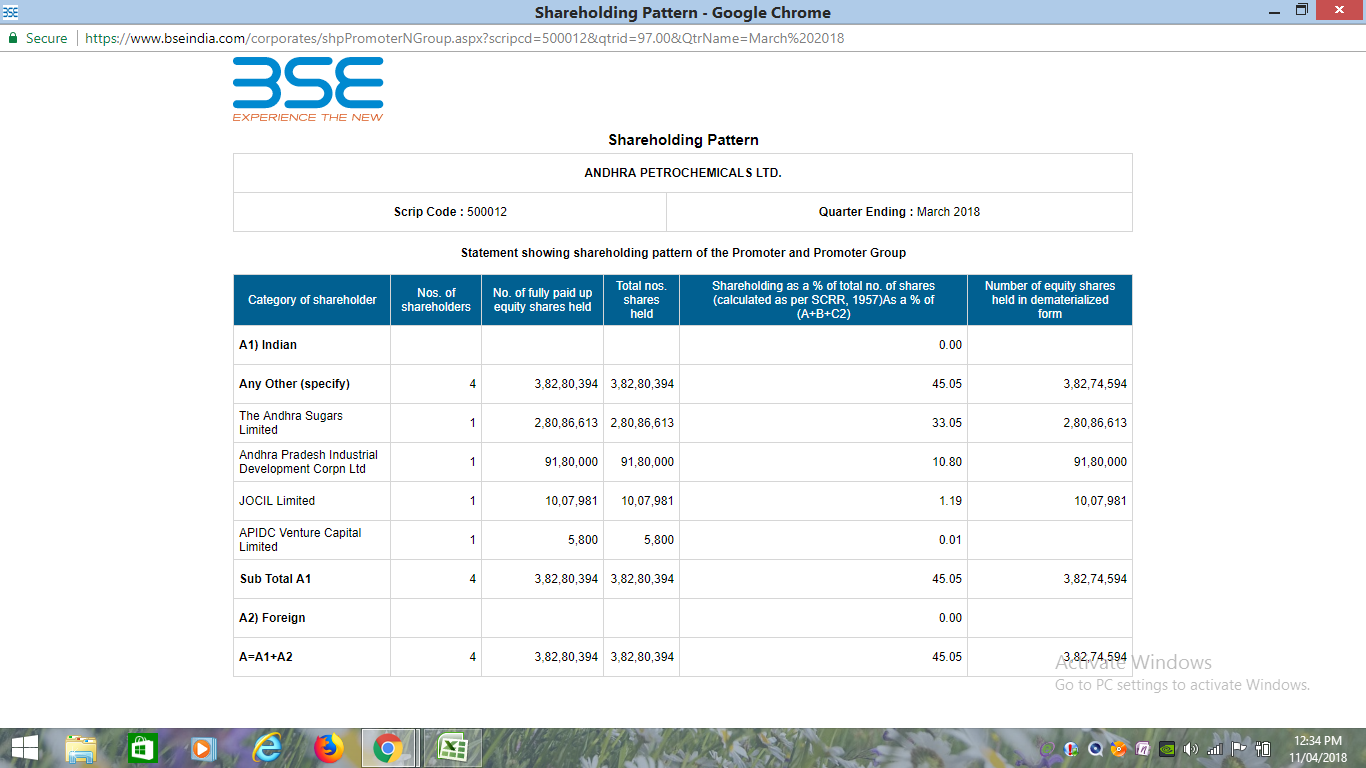

The Andhra Petrochemicals Ltd. (APL) was promoted by The Andhra Pradesh Industrial Development Corporation (APIDC) and The Andhra Sugars Ltd. (ASL) in 1984 as joint sector Company. Subsequently the structure of the Company has changed into an assisted sector. |

|

|

APL was established with a licence capacity to produce 30,000 MTPA of Oxoalcohols at Visakhapatnam, Since then the capacity has been expanded to 73000 MTPA by expansion and has been operationalised since May 2010. |

PRODUCTS

The company manufactures OXO-ALCOHOLS and has a market share of around 27% with balance demand met by imports . As mentioned in the last AR for fy 10, the company now has around 55% market share in oxo alcohols and the rest of the demand is met by exports.

FINANCIALS

EQUITY AROUND 85 CRORES, cmp around 22-23, market cap of about 195 crores

Debt as on March 2010 is around 143 crores.

|

Quarter |

Mar 09 |

Jun 09 |

Sep 09 |

Dec 09 |

Mar 10 |

June 10 |

|

Sales |

41 |

45 |

54 |

37 |

1.6 |

73 |

|

Interest |

0.36 |

0.38 |

0.53 |

0.36 |

0.07 |

3.6 |

|

NP |

1 |

-1.65 |

2.46 |

-1.73 |

-4.43 |

4.31 |

Now this was a stock I posted on TED when it was around 12-13 levels in Nov 09.

Link: http://www.theequitydesk.com/forum/forum_posts.asp?TID=2532&PD=1

Now comes the interesting part.

The plant was closed in Nov 09 for the purpose of assimilating the new capacities with the existing capacities. It remained shut till May 2010 when it was re-opened.

In fact this was the exact announcement:

With reference to the earlier announcement dated November 10, 2009, Andhra Petrochemicals Ltd has now informed BSE that the Modernisation-cum-Optimisation of the Oxo alcohol Plant has been implemented with an investment of around Rs. 275 crores and the Expanded Plant with a capacity of 73,000 MT per annum has commenced commercial production from May 01, 2010.

Now if you look at the June qtr results, the production effectively took place only for 1 month and company clocked a turnover of 73 crores. So for Sep quarter, when effects of full expansion are reflected, one only needs to guess where the sales figures will go.

The promoters raised their stake by around 10 lac shares between March 10 to June 2010.

INVESTMENT ARGUMENT:

The company has completed its full expansion and is set to report good robust numbers going forward, following which profits also are expected to increase. The markets seem to have factored in the expansion benefits to some extent but I feel, that better results would lead to higher levels in this stock.

The company with capacity to handle 55% of total demand in India seems to be sitting in a nice position and due to economies of scale and operational efficiencies, is now able to compete with cheaper imports.

TECHNICAL VIEW:

The stock has been in an upward sloping rising channel with resistance pegged at around 26 and support at around 20 levels If and when the resistance of 25-26 is crossed, there could be significant upsides.