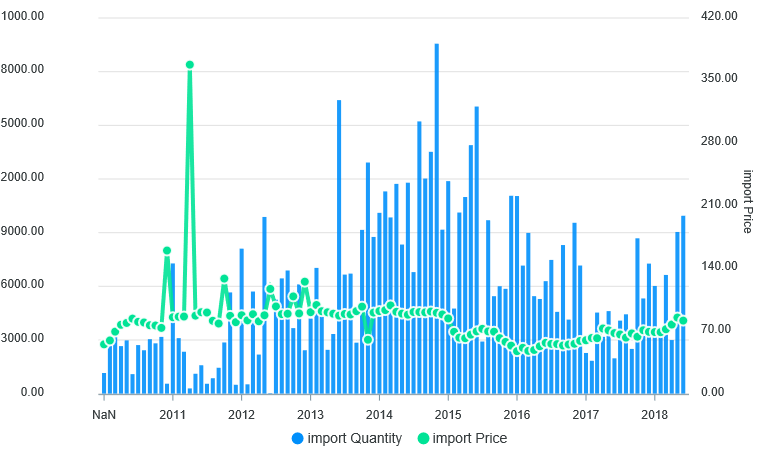

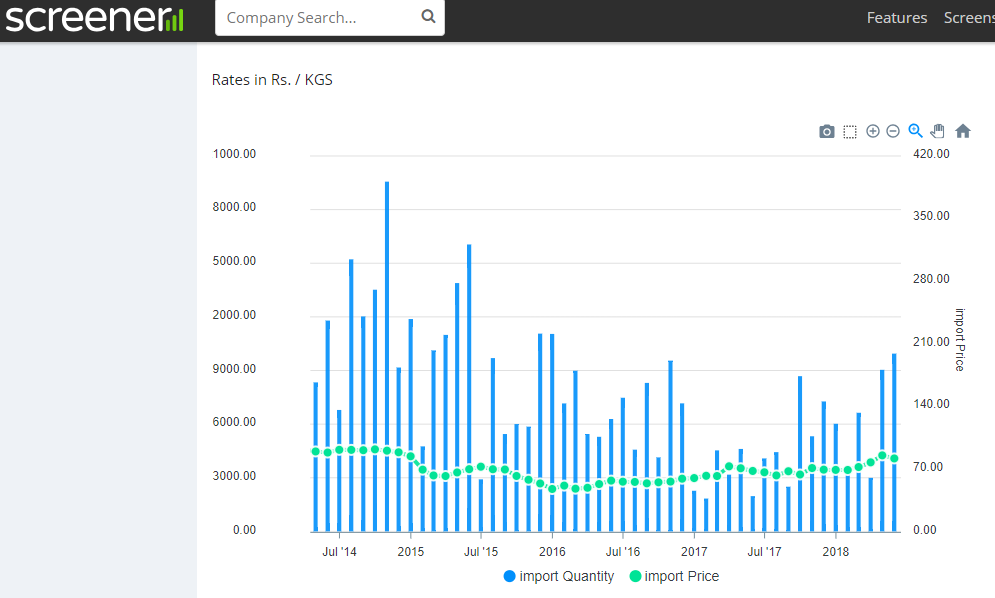

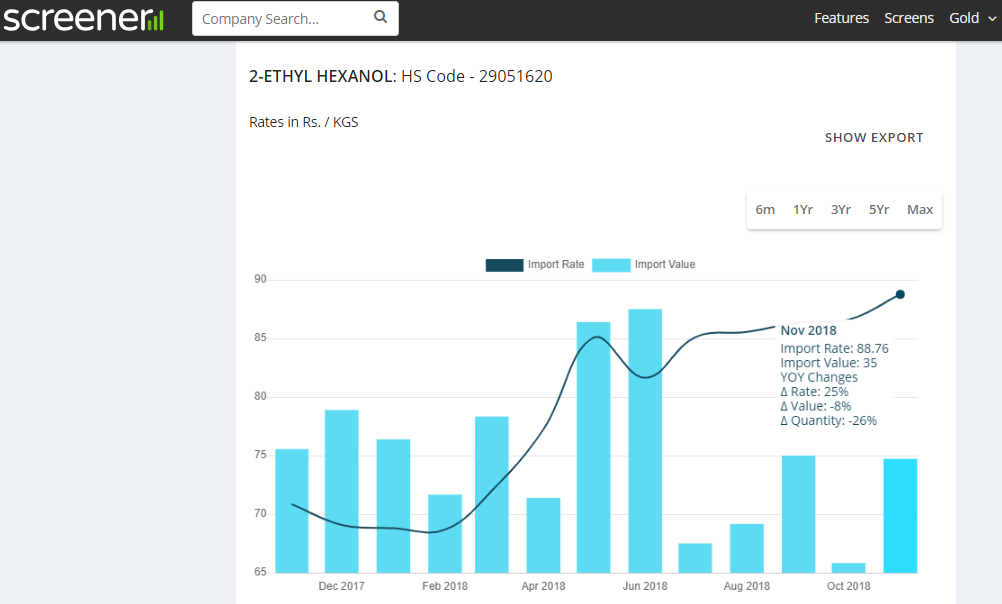

Another interesting thing to observe from above is that despite 35% increase in price over the 1 year, the imports seem to have dipped in the recent months.

The Andhra Petro stock has taken a beating post the Q2 results as the Co. clearly could not pass on the increased raw material costs. One has to understand that companies like Andhra Petro do not have pricing power & the price is determined by the landed cost of its products (Imports). The increase in raw materials cost is usually passed on, but with a lag. This is possibly what is happening at the moment, as the prices of all its products are higher currently than they were in Q2, even as crude is correcting rapidly. Q2 results were impacted not due to fall in Sales, which continued to grow, but due to the Co.'s inability to pass on the RM price hike. This trend of Sales growth should continue in the second half of the year as well.

The valuations are supportive, & even if the Co. does no better in the second half than it did in the first, it should still manage an EPS of about Rs. 11, after getting back to paying taxes again. The current price of Rs. 66 presents a good opportunity in my view. Another positive is the aggressive reduction of debt should see the Co. becoming debt free in the current year itself.

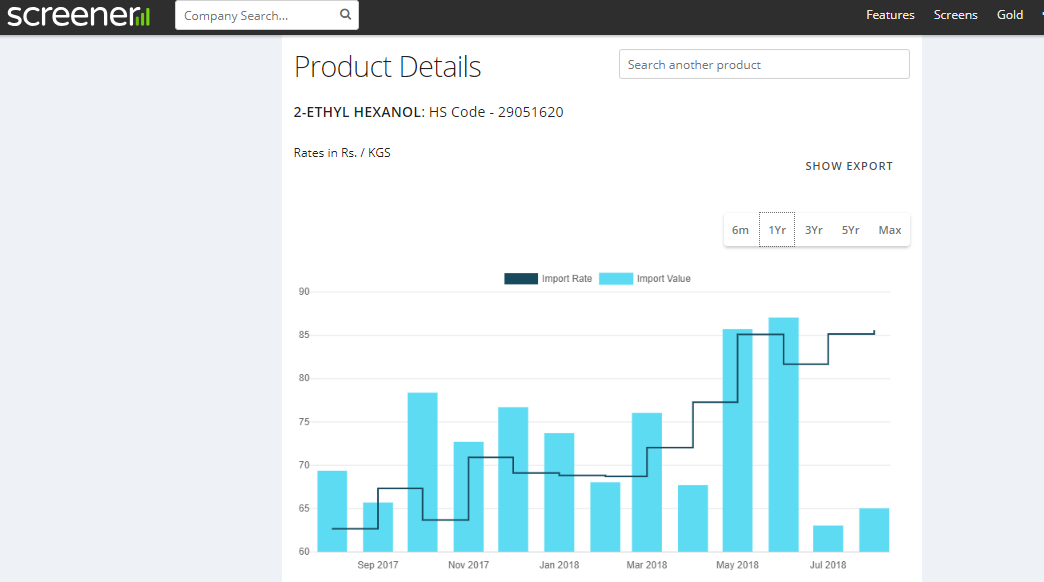

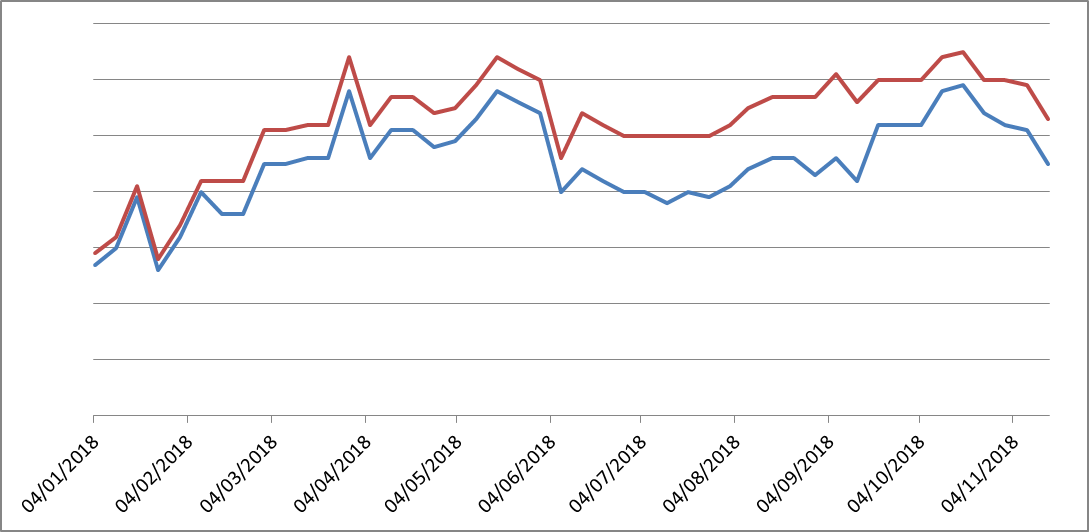

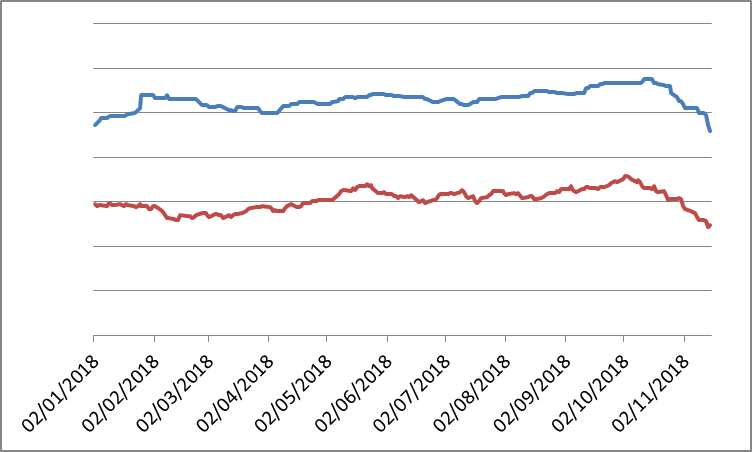

@bikedi These graphs seem to be positive for the stock. While propylene prices are lower than a year ago, prices of 2 EH, the main product of Andhra Petro are up 20% from a year ago prices. The SE Asia prices for 2 EH were quoting at 995 USD/MT as on 16/11/17 are now quoting at 1195 USD/MT on 12/11/18 after correcting from a high of 1225 USD/MT

Thanks for the immediate response sir. I have a small query here since the prices of end product s have come down the topline is going to come down . Will it be considered as a negative qoq? or as we expect the margins to be better coz of fall in RM prices

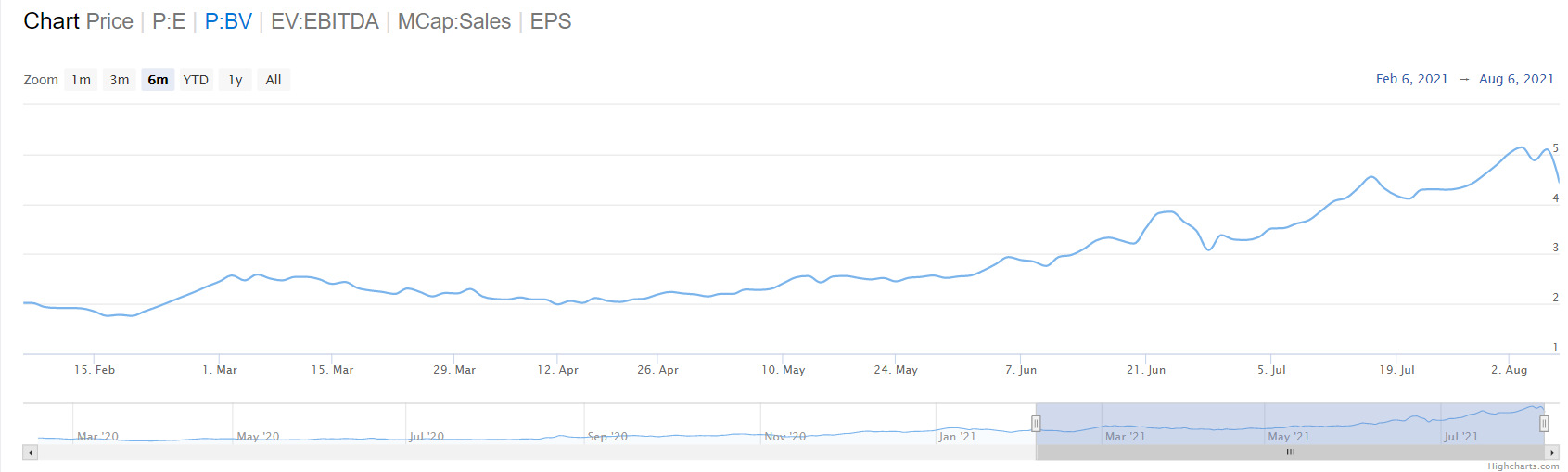

Thanks to @amishra for sharing this. This is new to me. I had not thought of this. While i was using PBV as one indicator to pick up stocks, I did not realise that PBV can also be treated as a chart and stocks should be avoided if the PBV is going too much up. Good time to get into stocks is when it is trading at almost flat or marginal increase in Price to Book value because then it means that when the price of the stock is going up, the book value is going up too. And since Book value is the net value of a firm’s assets found on its balance sheet, the price of the stock would be more stable at a low flat PBV than at a high PBV.