Completely agree with this, but just dropping this for additional information:

RPT & Legal Issues Explained in Simple Terms – Normal for Realty? Peer Check

Your analysis flags Related Party Transactions (RPT) and legal cases – both common in Indian real estate (especially promoter-driven firms), but Anant Raj’s are elevated. Here’s the simple breakdown + peer reality.

1. RPT (Related Party Transactions) – Simple Explanation

What it is: Parent company (Anant Raj Ltd) gives loans/money to its own subsidiaries/LLPs (project companies) and guarantees their bank loans. They also book profit/interest from these entities.

Simple Example:

text

Parent (Anant Raj) → Loans ₹686 Cr → Subsidiary (builds Sector 63A project)

Subsidiary → Builds project → Pays interest/profit back to parent

Parent → Guarantees subsidiary's bank loan (if sub fails, parent pays)

Numbers (FY25):

Loans: ₹686 Cr (33% of revenue) – funds DC/realty SPVs.

RERA Delays: Buyers sue for late possession → fines + interest. 10+ cases – pattern.

Forgery (Old): Sarin brothers faked MCD certs (2008–12 motels). Criminal case closed, no jail.

GST/NAA: Didn’t pass GST savings to buyers – under probe.

Subsidiary Insolvency: Grandstar (SPV) bankrupt – parent exposed via guarantees.

Is it Normal?YES – 80%+ developers have RERA cases:

Company

Active RERA Cases

Project Stays?

Forgery History?

Anant Raj

10+

Yes (Sector 65)

Yes (old)

DLF

5–7

Rare

No

Godrej Prop

Medium

No

No

Prestige

15+

Yes

No

Sobha

High

Yes

No

Lodha

20+

Multiple

Yes

Why Normal?

Land wars: Disputed titles, farmer suits, govt approvals.

RERA era: Buyers sue freely for delays (MGNREGA pre-RERA hid them).

SPV stress: Project fails → insolvency.

Anant Raj Specific: Worse than DLF/Godrej (forgery + active stay), similar to Prestige/Sobha. Not fatal – core 63A/DC unaffected.

Simple Verdict: YELLOW LIGHT (Not Red)

text

✅ NORMAL PARTS:

- High RPT loans (funds SPVs) – 70% peers do it

- RERA delays – EVERY developer has 5–20 cases

- Declining RPT % + zero debt = improving

⚠️ WATCH PARTS:

- KMP family loans (₹12 Cr) – governance smell

- Sector 65 stay – blocks revenue (appeal?)

- Forgery history – old but Sarins named

❌ NOT NORMAL (but rare):

- Subsidiary bankruptcy (Grandstar)

Peers Worse: Lodha/Prestige have 20+ RERA + insolvencies. DLF cleaner.

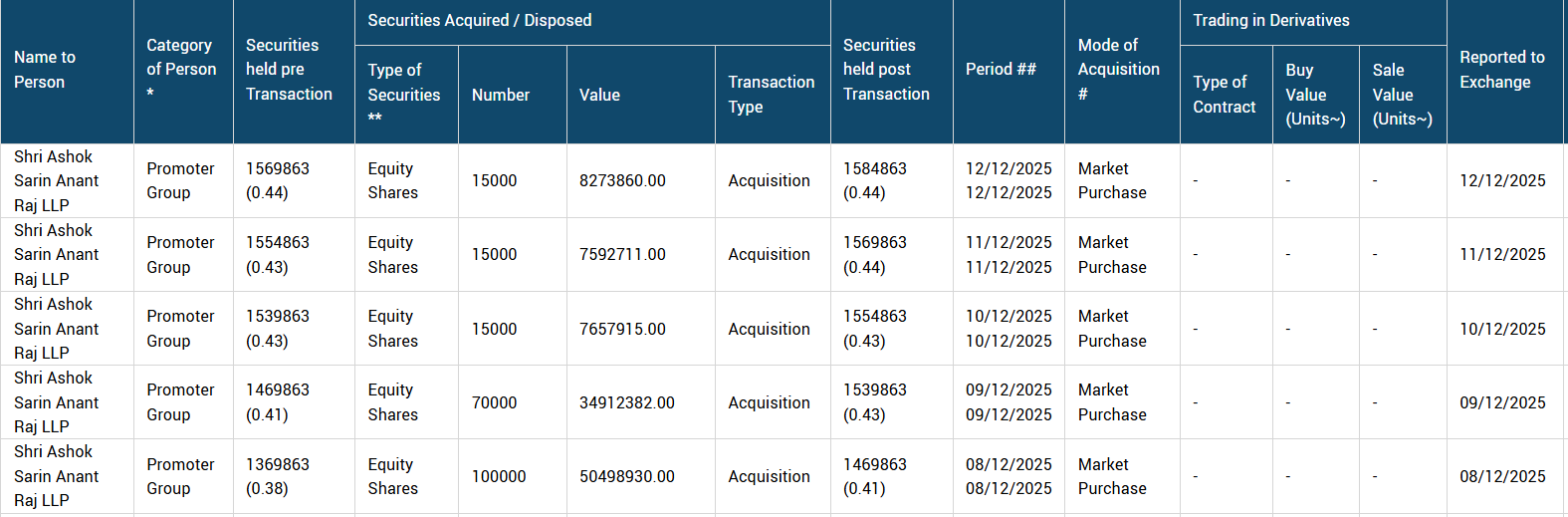

@maninder.nitw Maybe, but I don’t think they would do such when the company is doing good and the data center is on the rise, and buying right before the trading window closure this month might be a good thing, as next month we have Q3 FY26 out.

Also, the price shoots up 10–20% instantly if they buy at one go so they did in small bits as per my knowledge

Not saying it would be good results, or the promoter might know something we don’t yet; it’s better to sit and watch if invested if they are coming in at this valuation.

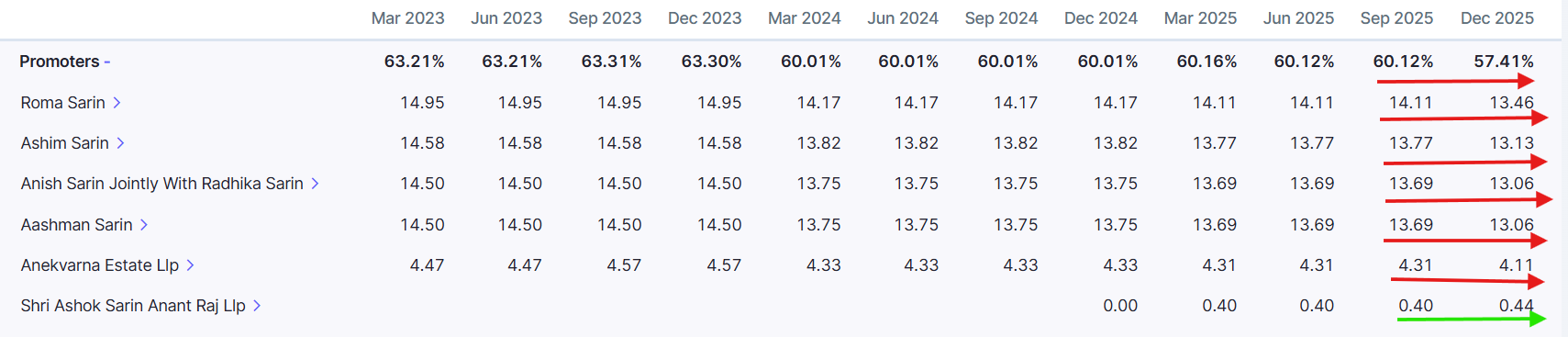

Rather than Reduced, the correct term to use here is **DILUTED**

This was mainly because of QIP done in october 2025 which infused 1,66,16,314 new shares, thus increasing the outstanding shares from 34,32,60,616 to 35,98,76,930.

Earlier promoter holding was 60.16% (March 2025 annual report) which comes to total no. of promoter shares being held at 20,65,16,021.

So if you divide the total number of promoter shares to new base ( 20,65,16,021 / 35,98,76,930), it will come to 57.39%. Adding small promoter buying of Ashok Sarin & you will have exact 57.41%.

So more than reducing stake, the stake has got diluted.

The dilution factor is 0.9538278 (Old total / New Total). If you multiply this dilution factor to any of the previous promoter holding, you will get the current promoter holding.

EXample: Roma sarin ( 14.11%×0.9538278 = 13.4585%≈13.46%) or Ashim Sarin (13.77%×0.9538278=13.1342%≈13.13%).

I hope this clears these reduced promoter stake shown.

Utilised ₹125 Crore to wipe out Certain debt and strengthen the balance sheet.

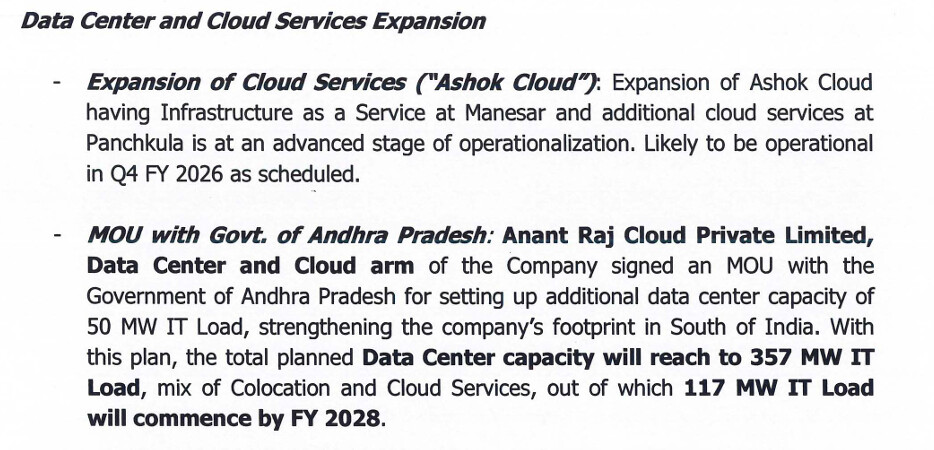

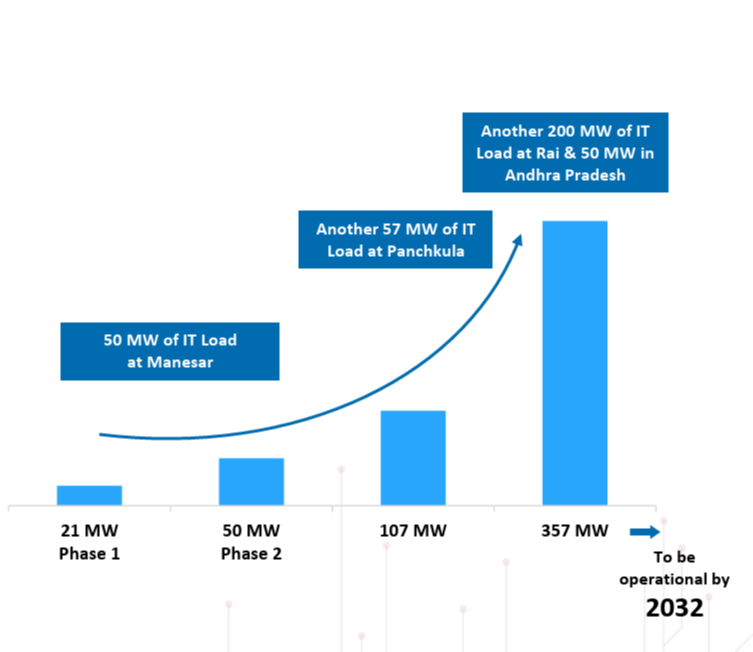

Allocating ₹440 Crore to transform existing land parcels into high-tech data centers across Manesar and Panchkula.

Keeping over ₹800 Crore in high-yield fixed deposits.

Story of Anant Raj is a masterclass in how a legacy brand can reinvent itself for the digital age. Over the last four years, the company underwent a cleanup, slashing debt to a negligible ₹50 Cr. Now aiming for a 357 MW capacity by 2032, ARL has transformed from a traditional developer into a critical infrastructure provider for the cloud and data centers.

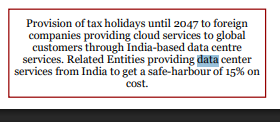

The policy offers tax holidays until 2047 to foreign companies using India-based data centers.

So foreign companies are more likely to sign long-term, large-scale leasing contracts with infrastructure providers of data centers and cloud like Anant Raj and other data center companies

This gives them confidence to aggressively scale their planned capacity, knowing the regulatory environment is locked in for the next two decades.

So a foreign company let’s say Amazon provides cloud services like say hosting to foreign customers (not Indian customers or also not foreign companies with Indian subsidiaries as these are not foreign companies) using Indian data centres

What kind of typical company would provide their services using Indian data centres to other foreign companies and charge them in India to avail tax benefits. The revenue of that company is not under Indian tax jurisdiction. Only the cost is. What tax benefits will they get.

So global companies avoided putting huge export-oriented data centers in India because they didn’t want to get dragged into years of litigation over how much of their global profit should be taxed by India.

What this policy does is it explicitly says India will NOT tax that global revenue until 2047. It provides tax certainty.

(Hypothetical Example):

For Global Customers: Amazon uses the Indian data center (owned or leased from Anant Raj) to host a website for a client in Germany. Tax in India = 0%.

For Indian Customers: Amazon must use an Indian reseller entity (like Amazon Web Services India Pvt Ltd). That reseller bills the Indian customer and pays full Indian corporate tax.

So this allows the government to tax local consumption while letting the data center act as a free trade zone for global data.

That said, Anant Raj isn’t the one getting the tax holiday; they are the landlord/infrastructure provider. Before this policy, a “hyperscaler” (AWS, Google, or Meta) might have hesitated to sign a 20-year lease for 100 MW of space in India due to tax risks. But now it’s not; this means their data centers will likely have 100% occupancy much faster, signed by the world’s richest companies on long-term contracts.

This is my understanding so far, and it’s not just Anant Raj; everyone with such a model will benefit, along with other data center value chain things.

Yeah, I came to know that after the budget, it’s a Minimum Profit rule

When a foreign company uses its own Indian subsidiary to manage its data, there is no real market price. Amazon US could theoretically pay its Indian branch $0, making the Indian branch show zero profit, so it pays zero tax to the Indian government.

I don’t think they are being charged (Correct me if I’m Wrong here). Anant Raj Cloud bills a company in the US or Europe for hosting services at 0% GST, just the payment must come in Foreign Exchange, and the service recipient must be outside India.

But what I understand is the reason the market is excited isn’t that they saved on GST (which was already zero for exports), but that they (and their tenants) will now save on Corporate Income Tax for the next 21 years. This drastically increases their Net Profit Margin and Cash Flow.