Nice write up! Revenue growth is commendable. Any idea what is the margin for the Comfy business? How has the profitability and margin trend been since 2014?

Are they playing a cheaper alternative to Whisper/Stayfree (MNC brands)?

Which segment are they targeting?

I think this sub segment of their business needs more dissection to understand the future course of overall business. Thanks

1 Like

Yes, that’s a valid point. They have not declared the financial metrics for Comfy other than admitting that margins are lower than balms. They started out with a Rs.20 pack targeting first time users and are gradually moving up the value chain with more variants and premium products. A Comfy Period Tracker app has been launched recently. There are also plans to get into other related products like menstrual cups and tampons.

Comfy is likely making losses, given the investments required in brand building and distribution. It is after all a low-priced product with intense competition. What we know is that the growth is coming from the Hindi belt rather than the South, with company’s focus on small towns of less than 10 lac population. Currently the production is done in a GMP certified unit owned by a European supplier with whom Amrutanjan has a technical collaboration. But the management has said they may set up their own plant in future. I guess only when the company announces their own plant, we can assume the product is breaking even.

7 Likes

New Advertisements for Pain relief category featuring Mirabai Chanu and Bajrang Punia.

5 Likes

I would say, a descent set of Q3 results from the company…specially the resilience in the OTC sales and profits despite the inflationary environment and the high base of last year.

Disc : invested, biased.

1 Like

So from FY 16 to FY 20 the profits were flat:

22 22 20 25 25

And the from FY 21 till TTM the profits suddenly became 3x to 61 in fy 21 and

63 in ttm basis!

What exactly changed in FY 21 that accelerated this growth? Is it a one time phenomenon driven by covid scenario?

What did they structurally did right after fy20 ?

4 Likes

One of the promoters Dr.Pasumarthi Sathya Narayana Murthi has sold 4.9 % of his holding on 7th of March, any idea on why he sold ?

@dpakag Inter-transfer

Amrutanjan RA.docx (46.9 KB)

Analysis of AHL

2 Likes

Thanks a lot for the response

1 Like

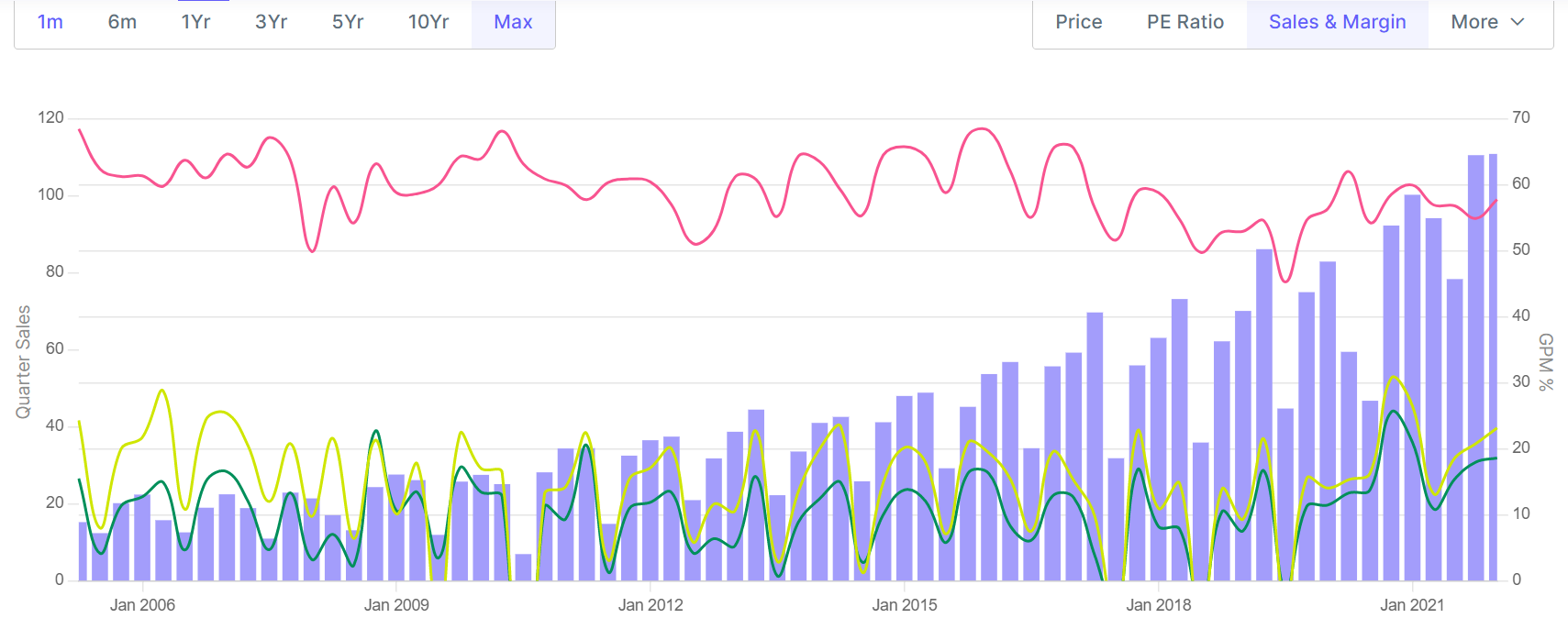

Came across this observation. Sales & margin in every June are lower.

Curious to know why their products are not sold well during one quarter in a year.

Checked if there is any relevant price movement to mirror the sales, but that’s not the case.

PS: Not invested / Came across this during my research

3 Likes

What scale are they using here? Height of the bar in the histogram more than doubles for 10% growth in profits!

This problem is there throughout the presentation.

9 Likes

@Karthic

Even this year Jun sales and margins are lower at Historical level. As per company presentation, Margin compressed due to increase in both Raw material and Packing cost. Only silver line in the results, comfy sales increased compared to 1QFY22 and decrease by only two cores compared to 4QFY22 with not much increase in advertisement cost.

4 Likes

Their products are probably used more in winter because methanol gives you a burning sensation and you don’t that burning in summer since we are already burning cos of the heat ![]()

1 Like

Curious to know if this is a good bet at CMP for long term. This is in my watchlist for past 2-3 weeks and I was waiting for it to go below 722 level. There is a strong multiple support at this level on monthly chart and 40% opportunity from all time high.

1 Like

Thanks for the links! Any views/ counter views on the company itself?

Views on the results uploaded today?

The company is more than 100 yrs old and was set up in 1893. Earlier the company used sell only the yellow pain balm. The company then diversified into several other businesses like textiles, chemicals etc. However none of these businesses work. Under the third generation of Mr Sambu Prasad, starting from 2005, the company started its focus on the core OTC range of pain balms

In 2011, the company acquired the fruitnik brand to foray into the beverages. Also the company saw a clear gap in the women sanitary napkin market and hence forayed with the launch of Comfy in 2013

Amrutanjan has the following product categories:

- Amrutanjan Pain Range

- Amrutanjan Back Pain+ Range

- Relief - Cough & Cold

- Women’s Hygiene

- Beverages

- Other Products

The cash cow remains the OTC products in the pain range bringing in ~180 cr of revenues. Women sanitary napkins bring in another 70 cr of revenues. Electro+ORS bought 30 cr of revenues up from 12 cr previous FY. Due to this growth, the beverage division became profitable this year

AMHL reaches 11.93 lac outlets in the country. Comfy reaches 3.5 lac outlets. Due to low penetration of sanitary pads, AMHL launched Project Disha where they have reached 1450 towns with less than 1 lac population to educate the customers and get them onboarded for sampling

For the cash cow (pain range and advanced pain range), the major raw material for the preparation of balms is menthol. Menthol is in turn derived from peppermint. To grow peppermint open, sunny situations without excessive rains during the growing period are congenial for the good growth. That is the reason the supply in India is concentrated in Punjab and hilly areas of Uttar Pradesh

Hence the vagaries of climate and rainfall adversely affects the raw material cost in balms. This is apparent in the operating margins of the company. Here’s the snapshot:

This shows that the company is unable to pass on the raw material cost to the customer due to the intense competition. The same opinion has been echoed by CRISIL in their ratings rationale as well (Link).

This justifies the company’s focus on distribution in the balm categories to increase their sales.

Along with re-branding, distribution re-vamp was also undertaken starting 2009. Over the years, the company moved from Pharma to FMCG distribution model

- Strategic Transformation of Amrutanjan Redistribution (S.T.A.R) was launched with emphasis on expanding direct distribution which facilitated the distribution of other products in the retail outlets which earlier used to sell only 9 ml balm

- Emphasis on balancing both wholesale and direct distribution routes to balance reach and costs. From the highs of 50%, the wholesale contribution is currently at 30% which the company feels is a healthy level

The Company invested in expanding its footprint to the lower town class, particularly in rural areas by appointing sub-stockists to improve last mile coverage of outlets. These initiatives have yielded results and the value contribution from rural has increased to 29% in FY22

Company’s working capital looks as follows:

This shows the improving brand recall and the demand from the customers. The company is able to take the advance payments from the customers and at the same time pay their suppliers after 3-4 months. The above chart shows that the company is able to collect the money 35 days before the product starts getting manufactured.

Hence their ROCE profile is stupendous. This is also evident from the following chart:

Amutanjan has three manufacturing facilities – two for OTC (one each in Tamil Nadu and Telangana) and one for Beverages in Tamil Nadu. Most of the OTC products, barring De-corn caps, Sanitary Napkin and Joint Muscle Spray are manufactured in-house.

While the company’s cash cow, i.e. body pain, headache and congestion management balms deliver a very moderate growth, the majority of growth is expected to come from Women’s hygiene (aka sanitary pads/period pain roll ons etc.) and beverage division.

Their women’s hygiene division grew by 82% CAGR since their inception in 2013 and till today they occupy less than 3% market share in sanitary pads. As a comparison, comfy pads cost 35% less than the competitors (J&J, P&GHH). Also the company has implemented ERP and automated the sales force completely which would help in obtaining more granular data and hence improving the coverage.

Regarding the addressable market, the sanitary pads market is currently valued at 5000 cr and is expected to reach at 8000 cr by 2027. Even if the company is able to achieve 10% market share, we are looking at the Mcap of 4800 cr for sanitary pads division considering 6 times sales multiple. PGHH trades at 10 times sales multiple in India. The same multiple values it currently at ~400 cr. Remaining 1700 cr is attributable to other divisions. Even the modest 12% increase in the sales of other division will make the other divisions valued at 3000 cr with the combined Mcap of 7800 cr

We might possibly look at the strong regional player emerging and competing with big MNC’s with the glocalization approach. Of course, all this is very simple to do on excel and hard to track and keep ourselves updated and free from bias. A lot would depend upon the execution and the leadership walking the big talk

Do follow me on twitter: https://twitter.com/manujindal2803/status/1589605408389599232

9 Likes

Is Comfy making profits? Unless it starts making profits, valuing that business will be difficult.

1 Like

Hi Chandra,

I agree with your opinion. However, IMHO, the branded plays are having a gestation period in which distribution and marketing expenses increases post which on stabilization, the brands become profit centers. See the case of electro+ in case of AMHL. It made the beverage division profitable. I am expecting it to turn profits in the next 3 quarters.

Any metric which you are tracking that makes you think it will turn around in the next 3 quarters? What is the basis of this expectation?