In FY21, Amrutanjan’s revenues grew 27% to Rs.333 crore, but between FY13 and FY20, revenues grew in single digits from Rs.138 crore to Rs.261 crore. Whether the recent performance is a flash in the pan triggered by Covid related demand or something has fundamentally changed in the company is the moot question I am trying to understand. Strong growth has continued in H1 FY22, but that is also a Covid-impacted period and inferences can be misleading.

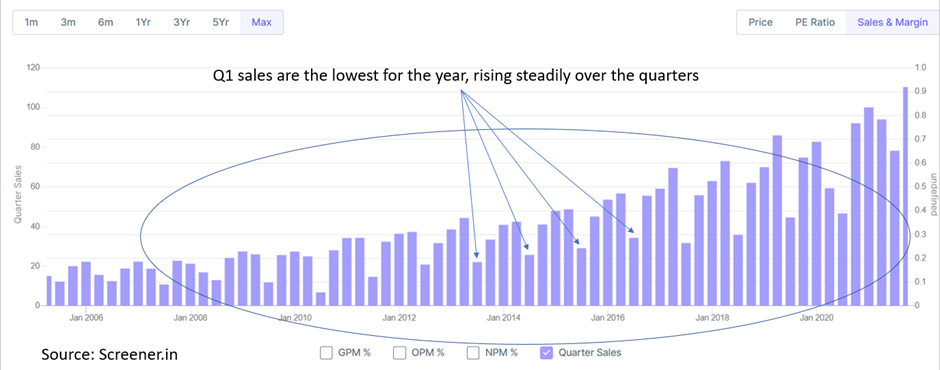

The business shows a clear seasonal pattern, with sales lowest during the first quarter of the financial year, and rising linearly in Q2-Q3-Q4. Ignoring the aberrations caused by Covid, past trends indicate around 15% of the annual sales happen in Q1, rising to 25% in Q2 and 60% in the second half of the year.

Most of the revenues continue to come from the flagship Amrutanjan Balm and its many variants and extensions around head, body, congestion etc. But this is a mature segment, not sure how fast it can grow sans support from events like Covid. If the recent jump in revenues is due to Covid, sales will retrace when Covid subsides and growth rate will revert to the earlier (low) mean.

The Beverages foray, after 10 years of nurturing has gone nowhere, clocking sales of just around Rs.17-18 crores per year last two years. It had registered revenues of Rs.20 crore in FY13. Fruitnik juice has been unable to dent established brands like Tropicana and Frooti. ORS Electro+ was introduced in FY17. It grew strongly in H1 FY22 and offers some hope for future, but it is too early and too small to celebrate.

The Services segment (Pain Management Center) is another drag on management time and energy, clocking just Rs.1-2 crore revenues per year. I am not sure if there are some intangible benefits coming out of this venture, otherwise I would like to see the company exit this totally, just as they exited chemicals business in the past.

Comfy – launched in 2011-12 - has done relatively well, growing from Rs.1 crore in FY14 to Rs.54 crore in FY21. Comfy now contributes 17% to the company sales. This is a high growth segment. Improving socio-economic conditions of women in India provides a natural tailwind to this business and is driving growth. Comfy can be scaled up significantly but will require good marketing acumen. Going forward, as Comfy grows faster and its proportion to Amrutanjan’s revenue increases, it will provide an automatic push to the company’s overall growth rate.

FMCG business is largely a marketing and distribution game. Amrutanjan’s distributor network has grown from around 1600 in FY13 to 2500+ currently. The management has spoken about taking it to 5000 but how much time that it will take is anybody’s guess. E-Commerce sales have begun but are currently small. Ad spends have increased in recent years, from single digits 7-8 years ago to around 15% of revenues presently. Olympic medallists Bajrang Punia and Mirabai Chanu have been signed up as Brand Ambassadors for pain products, and Shraddha Kapoor for Comfy. New products have been launched like Dental Pain Relief Gel. Prices of menthol crystal – the main raw material – have been benign in recent years, allowing company to invest in ASP without impacting profitability.

Based on the seasonal trends mentioned above and assuming Q2FY22 was a ‘normal’ quarter, Amrutanjan will clock sales of around Rs.125 crore in Q3 FY22 and Rs.130 crore in Q4 FY22. For the full year, the stock can report revenues of Rs.445 crore and at 17% PAT margin, is trading at a forward P/E of 35X. Views and counterviews are invited.

(Disc: Not invested)