Amrutanjan - can it repeat the success of small champ theme of marcelleous like in GMM / Alklyn Amines? Though it is having potential consumer brand in compfy and proven balm product… Will the sales catch up post covid unlock in souther states? Knowledgeable forum members - can you share your views?

3 Likes

More than balms product, the growth trigger that Marcellus expects for Amrutanjan is sanitary napkins in rural areas, where they have priced products very aptly. This could be a big ‘bottom of the pyramid’ market. The growth trigger for Amrutanjan is not balms. They have always been very winter heavy and have a good Q2/Q3. So there could be a rerating in the months to come

7 Likes

Am invested hoping the recent growth prospects with Women’s health foray with doubts on the Fruit Juices category showing de-growth. Some pertinent questions are

- Why did it take so long for the company to start building a distribution reach being solely concentrated in the south so far? Laudable that they’re thinking out of the box having tied up with Amazon, etc. but sill the question remains.

- The profits have stagnated for the last 5 years growing from 22 to 25 Crores, Know the price of their main raw material Mentha Oil fluctuates and reached highest levels recently but this could pose similar problems in the future. @spartan - could you please possibly throw some light on this.

1 Like

Hi,

These are my 2 cents of my understanding of the business model

Amtrutanjan is a very old company and they never compromised on quality of their product.

However they have mostly remain conservative and operated mostly in south region.However their products are readily available in other parts of INDIA,specially in eastern India.I belong to eastern India and I am using Amrutanjan from my childhood days.

The Moat they use to have in terms of OTC segment is kind of getting challenged. Market is flooded with similar products with less price and almost all have the similar kind of effect. And they know it, that might be the reason for them to diversify to other segments like Women Hygiene products and Juices. But those markets also have large number of players and the competition is high.

So would not be surprised the time wise correction to extend further until some significant change happens in the business model or in the market.

Thanks,

Deb

3 Likes

Hi, can anyone following Amrutanjan share some details on specifically the women hygiene part of their portfolio - such as Strategy, product quality/acceptance, target segment, geographical distribution, QoQ growth and percentage share of revenue/profits?

I believe that this segment has huge runway in India and therefore I am a buyer in P&G Hygiene even at current levels for long term. I wanted to know these details as a competition to my current investment and also to look at Amrutanjan as a new investment candidate in case this new segment Strategy and execution is promising.

I am sure their pricing would be very less/competitive as compared to market leaders. How big is that a threat to P&G Hygiene and how big is that an opportunity for Amrutanjan? Point to be noted is that price is not the main factor in women hygiene eventually but yes in a target audience where even basic hygiene/essentials is missing, this would be welcome from the those consumer’s benefit/awareness perspective. Any insights to this welcome!

Thanks

i am also investor - based on hygiene foray and it is growing well. my concern is beverages business - which might take time to deliver… and risky area. but considering the indian population and product positioning, it may be a future business may not profitable for next 3 years at least. but women healthcare side there could be more growth around 30 to 40%. Standard balm growth will be a cusion for investors. if they turn around/make the beverges a good candidate, it will be bonus for the investors… (thinking like manpasand kind of junk companies had a huge market share, amrutanjan a good conservative company can capture 10% of market share in long run).

1 Like

A quick check on Amazon shows me that contrary to my initial thought, there is not much price difference between a comfy and a Whisper (1 pad of whisper costing rs 6.8 and 1 pad of Comfy costing rs 6.5 approx for similar style). It is indeed amazing that they charging so close to a global leader and still selling well? Anyone aware of how well their product is accepted and in performance?

Pls correct me if I am wrong on the pricing part. I am aware that in diapers, even small compromise on quality would make a huge difference and same would hold for women pads. Is Amrutanjan trying to play an eventual premium best quality product or a cheaper alternative? What is the entry barrier in this segment? A small diaper/pad product to be efficient lot of R&D and testing would go behind it. I would not assume that P&G is global leader only because of their distribution and marketing might.

Big question, Can Comfy take on a Whisper??

Also, if an Amrutanjan can enter this niche segment - why not a Dabur or Marico ever ventured into this as it has greater synergies to them as well. I believe Godrej did have a women hygiene pad brand which it had sold out. What went wrong for them and why did they came out of such a promising segment…need to check…

5 Likes

Can anyone share AGM notes?

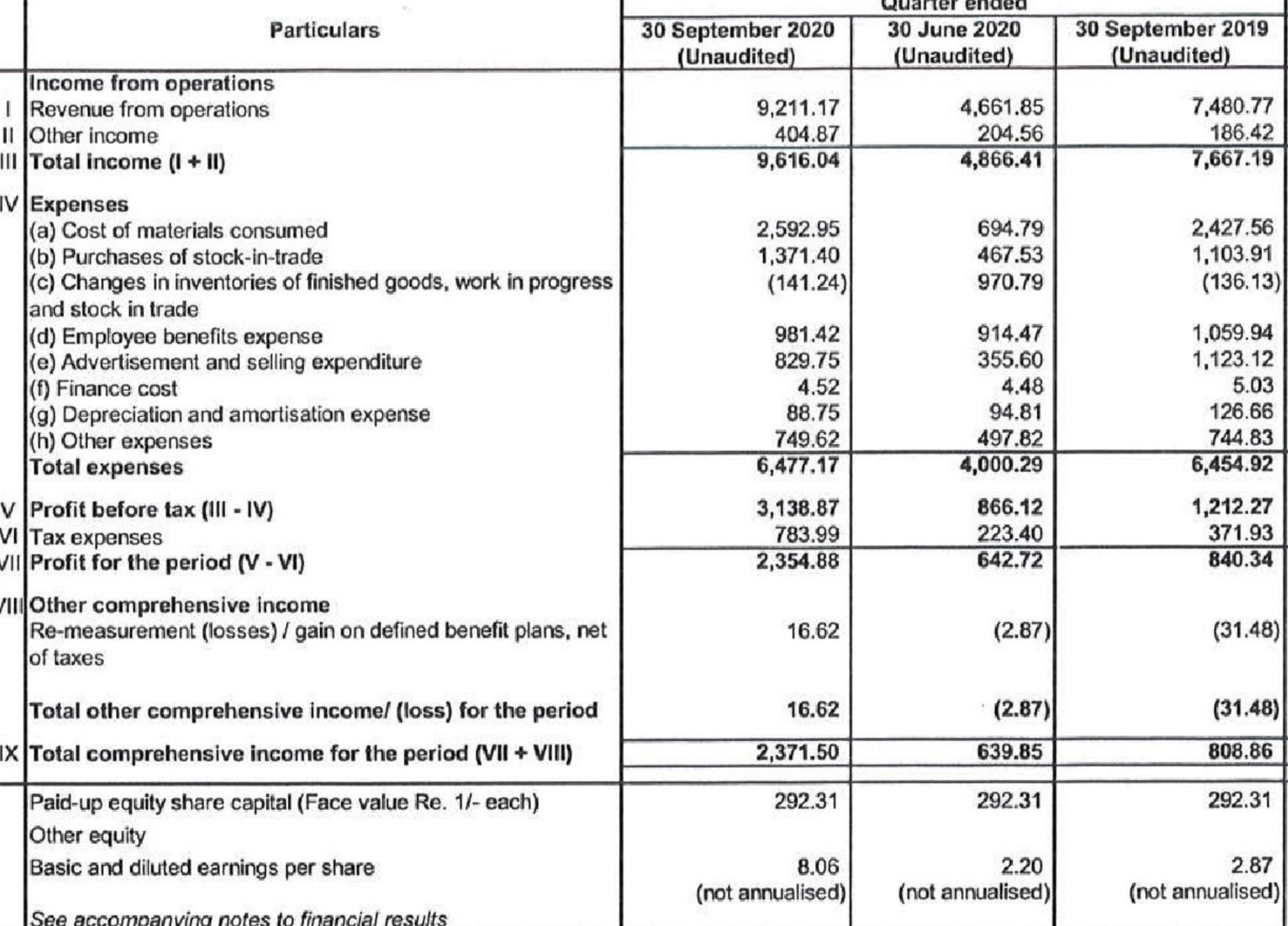

Q2 FY 21

RECORD Profits - Typical Annual Profits are 25 Cr and this Quarter’s profits are ~23.7 Cr ! Operating Leverage comes in play as the expenses remained more or less the same as previous quarter for ~20 Cr of additional revenues.

3 Likes

Good to see such 100 year old company shows some sparkle… the beverages - really a drag again… they can have more focus on money spinners than the draggers…

1 Like

Amrutanjan sales has grown by 18% to 263Cr for 9M FY21 lead OTC product growth of 22%.

Net profit showed 200% growth to 50 Cr for 9MFY21 due to gross margin expansion and low ad spend.

Along with top line growth reduction in cost of key raw material menthol has contributed to gross margins expansion. Channel checks do suggest that menthol price is around Rs.1400 per/ kg compared to more than Rs.2000 per kg around 5-6 quarters back.

Menthol is primarily grown in UP, MP,Biha,rPunjab and Haryana. UP state accounts for almost 80% of the country’s total production. In 2020 mentha production was highest due to increased acreage (+40%) of mentha cultivation as farmers were encouraged by good prices in the previous year. New variety of mentha also aided in high yield. Subsequently in 2020 prices have dropped significantly due to oversupply and reduced export from India due to pandemic.

This may lead to farmers moving away from mentha cultivation and prices may increase again which can impact gross margins for Amrutanjan for next FY. (Any feedback from UP state about present menthol crop will be helpful)

2 Likes

Yes, they have shown decent growth in net profit and it would have happened last year in March-20 itself but for corona.

In addition to the points you make, They have also limited the losses on their juice business ( fruitnik) and started focusing on the juices that provide hydration ( electrolyte drinks that you take when you are dehydrated) this has helped stop the drag on the profits from balms and pain relief

Their comfy brand ( sanitary napkins)is now 16percent of sales while balms and pain releif is still in excess of 70 percent.

If they can grow comfy strongly, this will be a stock to watch.

They also issued esops to employees recently.

Have started digitising sales force and Focus on North and West India where they are traditionally weaker

Disc: Invested recently from lower levels.

4 Likes

A VARIANT PERCEPTION :

To me the Amrutanjan story is playing out similar to ITC. Where the balm segment is the cash cow (just like cig business in ITC) and the management is foraying into areas of deploying this capital where the ROCE will be lesser than that from its main business segment. (Venturing into FruitNik like ITC ventured into FMCG or even hotels, maybe)

Comfy is a good business compared to the great balm business, unlike the gruesome beverage business at least it is giving satisfactory returns on capital. (Just like ITC foraying into packaging and notebooks where it can be called good as compared to the gruesome hotel business)

Disc : Not invested. Variant perceptions from connecting similar stories. (To be taken with a pinch of salt)

2 Likes

This observation is logical, however (just my perception) Amrutanjan diversification does make some sense, compared to ITC. They already have a good distribution network to pharmacies as part of their core product (pain balm). The new ventures like sanitary products, ORS can/may leverage that network. FruitNik seems a bit of a stretch, similar to ITC.

Disclosure : invested since 2017. No recommendation.

4 Likes

Amrutanjan is spotlighted in marcellus newsletter.

3 Likes

Found this report on Amrutanjan

5 Likes

Another set of good results from Amrutanjan with superb growth in all divisions(consider some extent of low base in Q4 of last year).

Margins continue to expand due to low raw material cost and low ad spend.

Investor presentation ( not sure why do they mention gross sales in presentation)

The best thing about the Q4 results is the steep bump up in the sales of Comfy @ 14 cr vs 7 cr and Electro Plus @ 6.8 cr vs 3.8 cr yoy

Both these are the brands that can really be scaled up meaningfully

This is indeed encouraging

Disc: invested

2 Likes

Not sure why we should look at Q4 20 for comparison and be happy. Compare it with Q4 19. Operating Profit is down by a 3rd. So it PAT. Even compared to Q3 21, things are bad.

Disc: Invested around 600. 1.5% of Portfolio.

1 Like

not too pumped up after looking at the results. The OPM and NPM have nearly halved compared to last two quarters. YoY it looks good because of low base of previous year’s quarter.

Will need to find reason for reduction in margins given that mentha oil is still at lower level.

disc

invested