Good Results.

Stock has hit an upper circuit.

YoY Sales/PAT increased 15%/185%

Mentha Oil declined a bit, thus comforting the gross margin a bit; The company’s strategy to not to take price hike when Mentha oil prices were at record highs, seems to have worked. Consequently, OTC sales are up 24% YoY indicating some market share gains.

EBITDA margin improved from 14% to 21% led by lower Adv. Expenses. This was primarily due to lower Ad exp. in beverage expenses; Beverage segment turned EBITDA +ve for the first time (but sales in this segment went down 27%).

GM of 54% seems to be sustainable as it still lower than 60-65% GM that Amrutanjan has 2-3 yrs back.

Stock was volatile over the years due to entry of MFs: DSP MF has increased its stake to 2.9% (vs 0%) and WASATCH has taken a stake to 1.1% (vs 1.0%).

1 Like

Beverage segment success and Female Hygiene segment growth will play a significant role in business performance. No player has been much successful in dislodging the duopoly of J&J and PGHH. The below report (a bit old) gives good info on the female hygiene segment.

A presentation I gave in one of a VP Bangalore meetup is attached.

Amrutanjan Healthcare Presentation.pdf (1.3 MB)

Disc:- Small position at 280 levels

6 Likes

The Leadership is clean and have Skin in the game. The company doesn’t have a good MOAT but a brand recall is possible.

There is heavy competition from established players like Emami and P&G. The price is not so attractive.

I am a little skeptical about investing in the company currently but I would add this to watchlist and would like to do more analysis on its competitors (especially Emami).

Attached in the PDF with my Analysis of the Company. Please let me know.AmrutanjanHealth.pdf (339.2 KB)

6 Likes

Annual Report 2018-2019

https://www.amrutanjan.com/pdf/AR1819.pdf

Key Points

Group revenue growth from Rs. 249.27cr to Rs. 281.31cr; a growth of 12.85%

• OTC revenue growth from Rs. 215.30 cr to Rs. 255.93 cr; a growth of 18.87%

• The pain business grew by double digits led by Roll on format

• The roll on format touched Rs. 35 cr in revenue.

• Comfy sanitary napkin brand grew revenue from Rs. 19.62 cr to Rs. 35.30 cr

• The brand Comfy now enjoys a volume market share of 1.9% pan India.

• The company grew profits by double digits in spite of a Gross margin drop of 400 basis points. The drop was due to all time high menthol and essential oil prices. The operating profit impact due to the price inflation is to the tune of Rs. 13.49 cr.

We were able to introduce a completely revamped body pain product range with positive market acceptance. We also launched an orange flavored ORS drink under the Electro+ brand. The sanitary napkin business saw the launch of a longer pad offering (Comfy XL) along with a family pack(20 units pack). These launches are testament to the execution ability of the organization especially across varied categories. We have plans to launch premium range of sanitary pads in the 1st quarter of FY 20. We will continue to introduce new variants in the categories we operate to drive market share growth.

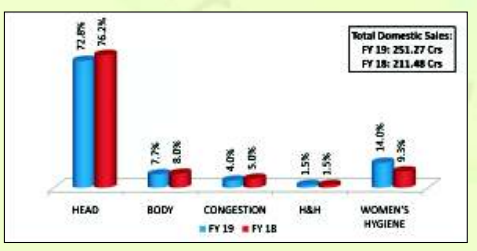

In domestic sales, Head segment continues to be the top most contributor at 72.8% of the total sales. With our continued focus on Comfy expansion, the contribution of Women’s Hygiene has increased significantly from 9.3% to 14% of the total sales.

Electro+ has seen 32% growth over the previous year. Orange variant was launched in addition to the existing Apple variant during the last quarter. Further, it enjoys a Gross Margin of 60% which brings in profitability to the overall beverage division.

Exports- In 2018-19, we have entered Mozambique and Zambia markets.

The following will continue to be the growth drivers for the company in

the coming year:

• Expansion of pain business in Western and Northern Zones

• Further strengthening the existing markets by introducing new products

• Continue improving distribution reach across town class with specific milestones for stockist appointment, chemist/wholesale reach, product reach etc.,

• Offering availability across channels, including Online

• Scaling up of new categories launched in the past 3-5 years

• Focus on maintaining the Gross margin ~60%

• Investing in brands and positive consumer experience

• Building on secular trends which are driving the Women’s hygiene category

10 Likes

Noticed the healthy ROCE from past 10 years

| Mar 2008 | Mar 2009 | Mar 2010 | Mar 2011 | Mar 2012 | Mar 2013 | Mar 2014 | Mar 2015 | Mar 2016 | Mar 2017 | Mar 2018 | Mar 2019 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| ROCE % | 34% | 30% | 18% | 14% | 19% | 20% | 24% | 26% | 29% | 28% | 25% | 25% |

Reckitt Benckiser: RB to expand market share in pain relief segment - The Economic Times?

Is Amrutanjan the leader in topical pain relief segment? or is it RB (Moov)?

1 Like

Notes from Amrutanjan ltd AGM ( my interpretation from MD speech and discussion. Possible that I may have misinterpreted some of the points mentioned below)

Only few companies have survived more than 100 yrs. Amrutanjan is one of them with strong fundamentals.

we only make natural products keeping customer health in mind. No plan of entering into allopathy products. Will remain loyal to Ayurveda. Not venture into chemical based pain killer products like diclofenac which has side effects.

Amrutanjan brand is one of the top 5 OTC brands.

OTC revenue grew 18% and we remain bullish on growth for fy20.

Focus on profitable long lasting business institute, creating shareholders wealth and remain debt free.

Last 5 year net profit did not grow much due to various issues but next few years bottom growth will be good.

Head and body pain category will have decent growth. Last year gross margins are impacted by 5% due to high menthol and other oil prices.

Base business of white and yellow balm have decent growth including volume and value:12% growth. We have not lost market share to competitor.

ROLL ON: (head and body segment): last yr sales 20 cr…this year good growth is expected …will continue spend on ad.

Lotion form was launched in Q4 to complete the portfolio…its preferred by elderly people.

Menthol is around 8-9% of RM cost for OTC products. last year price has reached peak and correcting now. Gross margins will improve for fy20.

Backward integration for menthol oil to convert oil to crystal form to save RM cost.

Other oil used prices have risen over the past one year. (karpoor 3% of RM) price up 3 times…gandhapur and eucalyptus oil (5% of RM) also high.

APMC: 1.7 Cr …Loss of 1.5 cr…spending ads …volumes should pick up.

Comfy sales : 35 cr revenue and very good growth for FY19…Orissa we have doubled sales…other states like KA/AP/MH/UP and WB sales are improving.

Importing raw material and outsourced the production…spending on R&D for better product.

Taken small price hike of Rs.2 in Q1… 2more variants XL and ultra variant (at Rs.39) …?premium pack introduced last quarter.

Comfy was successful due to better product,price and wholesalability.

Removal of gst input credit has impacted ad spend input credit , otherwise we would have been profitable.

1.8 lac outlets presently.

Beverages:

Difficult business to build…will take few years for brand to recognise and show benefit.

Electro+ is profitable with good margins.

we have integrated electro+ with fruitink distributors…giving almost 25% margins to distributors .

aim is to reach 1lac outlets. Ban of 200 ml bottle by MH state will affect the local players.

Target is south India market for beverages.

Beverage segment likely break-even for fy20

Profit: around 6% improvement due to tax benefit.

Discl: invested around 3% of portfolio.

8 Likes

While all divisions are sustaining their edge over their competitors, their beverage sales is tepid. I have tasted the drink which tastes like a sugar syrup. They are struggling for the past few years to increase the sales with little success. I have not seen their beverage in any of the kirana outlets.Management has to seriously think whether they have to continue the product which is costing their profitability.

I have a lazy question - I haven’t gone through the AR or company presentations. Why is a company involved in “ayurvedic pain relief” products, getting into fruit juices and soft drinks?

A company expanding into un-related businesses is a red flag.

2 Likes

Agree. Maybe because the pain relief market is estimated to be around Rs 4,200 crore, which includes all forms of products in cream, gel, spray and balm and they are trying diversification.

Amrutanjan makes OTC (over the counter) ayurvedic items. After pain segment, juice and juice electrolyte is a choice they opted. I am not sure about the shelf life and the success factors deciding it. Nothing forces a customer to buy a juice from a medical shop, an electrolyte (maybe yes but Gatorade (Pepsico) is available in supermarkets - easy reach and is well known)

Fruitnik Electro+ disclaimer states it is not recommended for diarrhoea treatment, only facilitates recovery

https://www.amrutanjan.com/Electro+.html

1 Like

Q2 2019 Results

Investor Presentation

1 Like

Q3 FY20 results. Good numbers.

Investor presentation- Not formatted properly

I got the right ppt from site… results good… can it be maintained… I am not sure why they are focussing on beverages - as it looks dragging.

1 Like

Amrutanjan Q4 results.

Revenue degrowth of -31% in Q4( 59 Cr vs 86 Cr) leading PBT degrowth of 10 cr vs 20 cr in Q4.

In the past,Q4 was generally big quarter for Amrutanjan contributing more than 33% of revenue.

With ongoing lockdown at Chennai things may not improve significantly in Q1 also. Only good thing is menthol price which is key raw material for OTC products is likely to remain low as I read.

Discl: invested

4 Likes

Amrutanjan investor presentation:

33Cr of revenue loss during March due to covid. Revenue would have grown by 14% instead of 2.7%( bottom line wound have grown disproportionately)

Company seeing improvement during May and June.

Cash reserve of 105 Cr.

Relaunch of NOGERMS hand sanitizer.(Management must be sensing some opportunity here. Not sure if they are manufacturing or outsourced like comfy)

No mention of comfy growth which was expected to be good.

Discl: exited.

1 Like

Any particular reason for exit? Results look down on account of lockdown etc. But do you see anything more to it?

Nothing particular. My sense is even Q1 will be impacted due to reintroduction of lockdown at Chennai and few more districts of Tamilnadu during last week. Moved capital to pharma companies. Amrutanjan will be under my watchlist for reentry.

Q1 traditionally is always weak for Amrutanjan.Infact they report bottom line losess in Q1 quarter and covid 19 will make things worse.P&L statement will have a bleak picture for this quarter.My Assumption is that Q2 also will have the ripple effect.

Disc : Not invested but tracking

Thanks,

Deb

1 Like

I am wondering why is that so, does late summer and onset of monsoon got to do anything with pain management?

Hi,

They have now 4 segments which drive the revenue

1->OTC

2->Comfy

3->Beverages

4->Electro Plus

Out of these 4 segments,OTC segment(Products of pain management, congestion management,cold & cough related) segment garners almost 80% of total revenue.And that is the traditional product for them and they usually have more market in winters than summer.So their revenue and profit gets hit due to this in Q1.

Thanks,

Deb

4 Likes