I saw there is an existing new thread on Ami Organics which is closed. The person who started is not updating the same so that it can be opened, I guess. Since I intend to provide more information I am hoping this one remains open. Alternatively I can move this information there if that thread is opened

Introduction

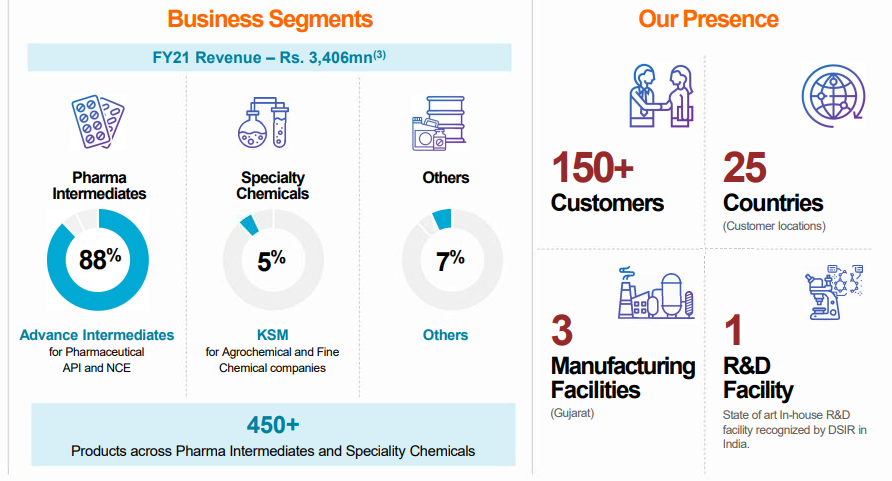

Incorporated in 2004, Ami Organics is an R&D (R&D) driven manufacturer of specialty chemicals with varied end usage, focused on pharma intermediates for regulated and generic APIs and new chemical entities (NCE) and key starting material for agrochemical and fine chemicals, especially from recent

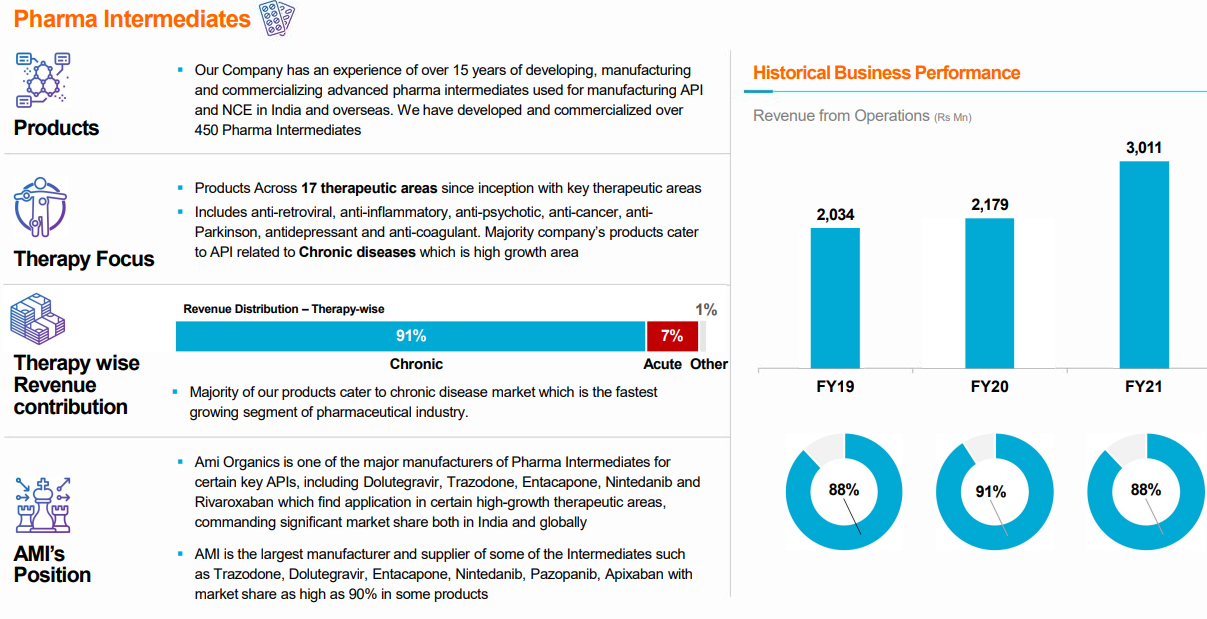

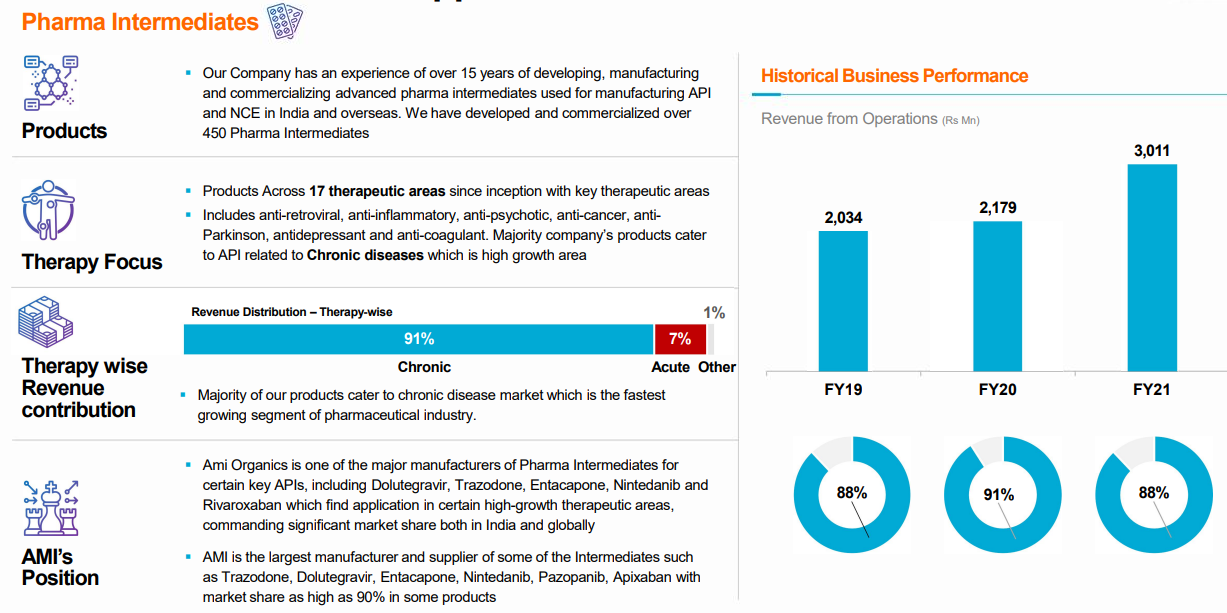

acquisition of the business of Gujarat Organics Ltd. It is one of the major manufacturers of pharma intermediates for certain key APIs, including Dolutegravir, Trazodone, Entacapone, Nintedanib and Rivaroxaban. It has three manufacturing units at Sachin, Ankleshwar and Jhagadia

Company IPO happened in September 2021 at Rs610. Stock currently at Rs1130/share

Industry Analysis

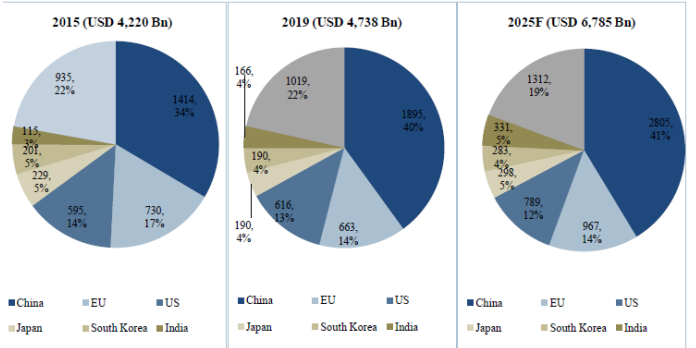

The global chemicals market is valued at around US$4,738 bn in 2019 with China accounting for major market share (40%) in the segment followed by European Union (14%) and US (13%). India accounts for ~3.5% market share in the global chemicals market. The global chemicals market is expected to grow at 6.2% CAGR; reaching US$6,785 bn by 2025.

Going forward, APAC is anticipated to grow at the fastest rate of 7-8% during the forecast period (2019-25F). The chemicals markets in Western Europe, North America and Japan are relatively mature and, hence, are expected to record slow growth rates of around 3-4%.

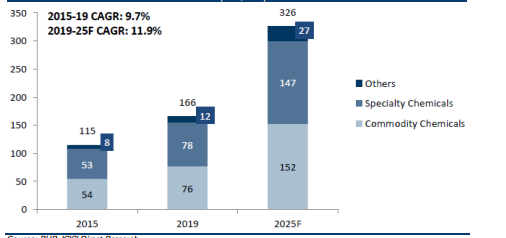

The Indian chemicals market is valued at US$166 bn (~4% share in the global chemical industry) in 2019. It is expected to reach ~US$326 bn by 2025, with an anticipated growth of ~12% CAGR. The specialty chemical industry forms ~47% of the domestic chemical market, which is expected to grow at a CAGR of ~11-12% over the same period.

Company Analysis

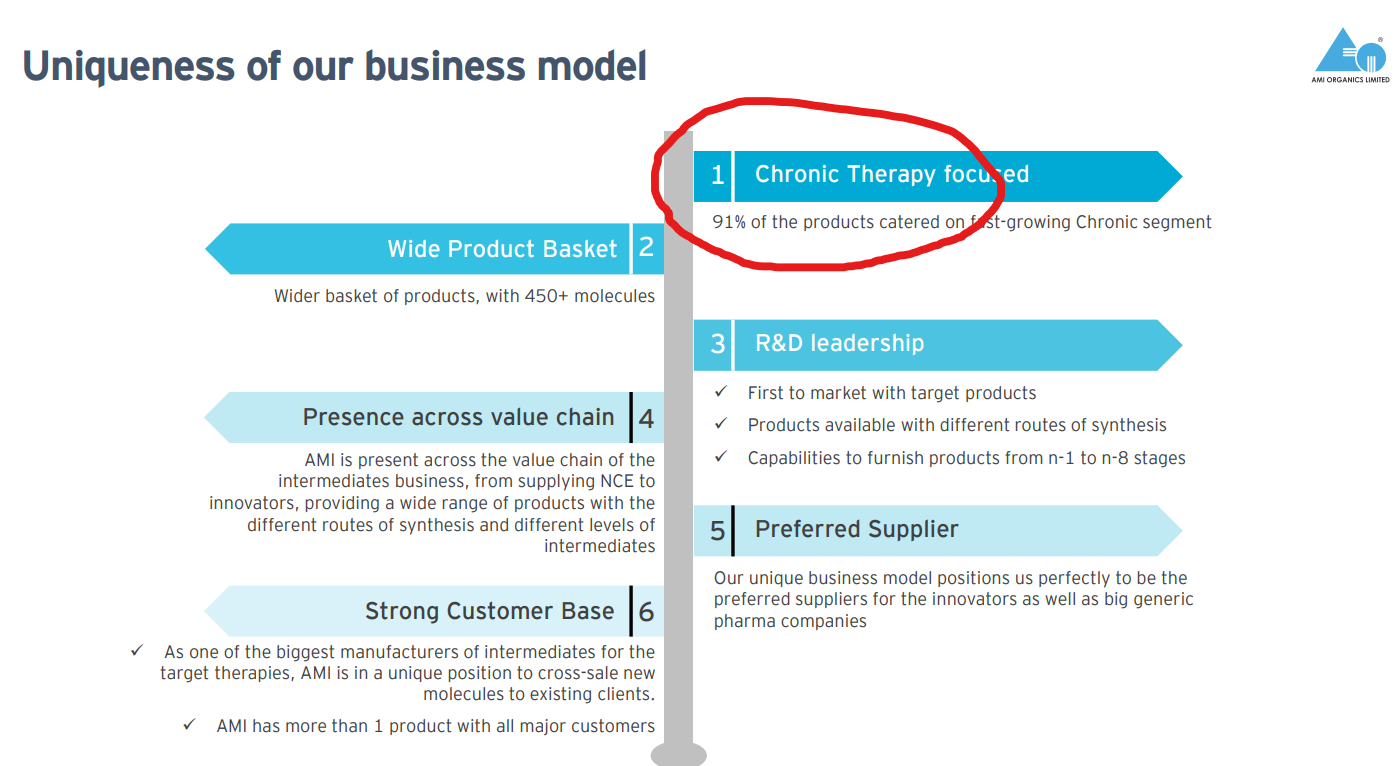

Some of the AMI’s products such as Pharma Intermediates command a significant market share both in India and globally

![]() AMI recently completed the acquisition of two additional manufacturing facilities operated by Gujarat Organics Limited which has added preservatives other specialty chemicals in our existing product portfolio, which command significant market share globally in the supply of certain paraben derivatives.

AMI recently completed the acquisition of two additional manufacturing facilities operated by Gujarat Organics Limited which has added preservatives other specialty chemicals in our existing product portfolio, which command significant market share globally in the supply of certain paraben derivatives.

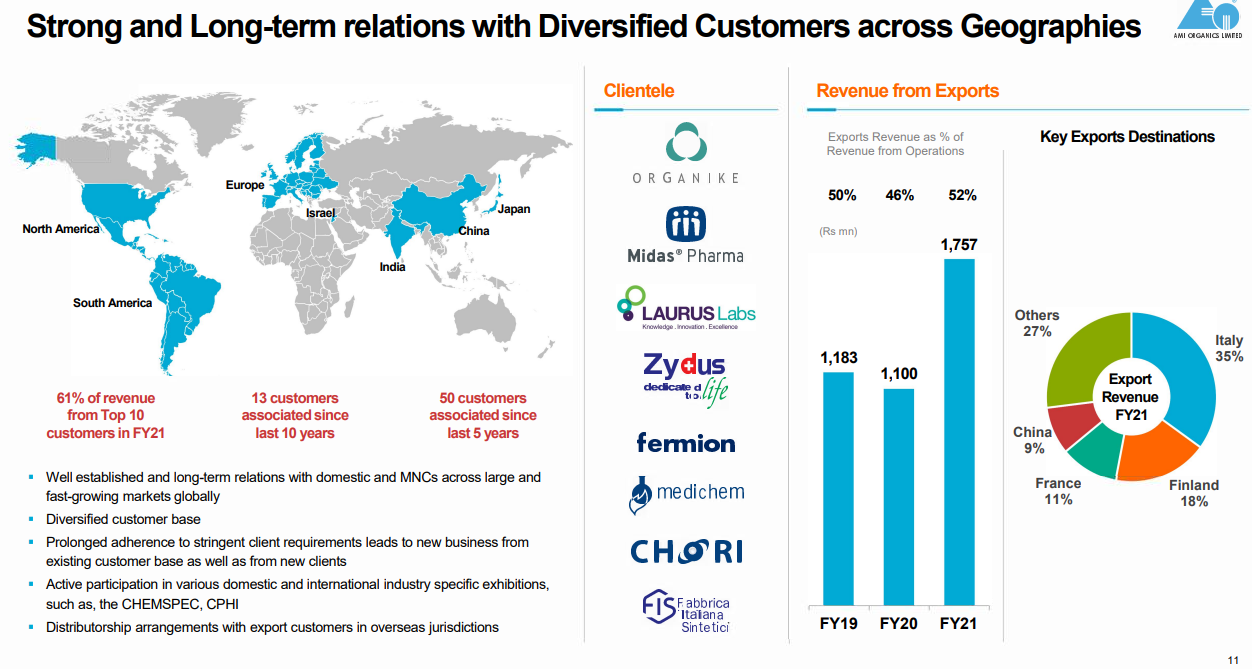

![]() Company has a Strong and long-term relationships with numerous domestic and global pharmaceutical companies

Company has a Strong and long-term relationships with numerous domestic and global pharmaceutical companies

![]() During FY21 Company export contributed to 52% of revenue from operations

During FY21 Company export contributed to 52% of revenue from operations

![]() 8 process patents published(1) along with 3 additional pending process patents(2)

8 process patents published(1) along with 3 additional pending process patents(2)

![]() Raw Material Sourcing: ~73% of RM is sourced from domestic vendors as of FY21

Raw Material Sourcing: ~73% of RM is sourced from domestic vendors as of FY21

Key risks & concerns

Higher RMAT cost, inability to pass on to impact performance: The company’s primary raw materials include ethyl alcohol, dimethylformamide, isopropyl alcohol and toluene. It does not have long term agreements with most raw material suppliers. The company’s inability to correctly forecast demand and supply may have a material adverse impact on working capital, business and results of operations

Loss of customer to impede performance – Loss of customer or lower business growth from large customers owing to intense competition can impede the growth of the business

Regulatory related challenges for any plant to hurt performance – Since the company operates in intermediates for pharma API, it has to follow stringent norms as per USFDA and REACH certification.

Any irregularities can result in a ban on manufacturing activities and thereby impact the financial performance of the company

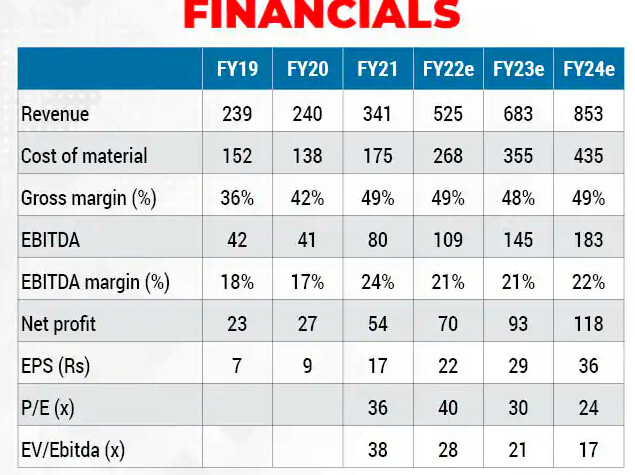

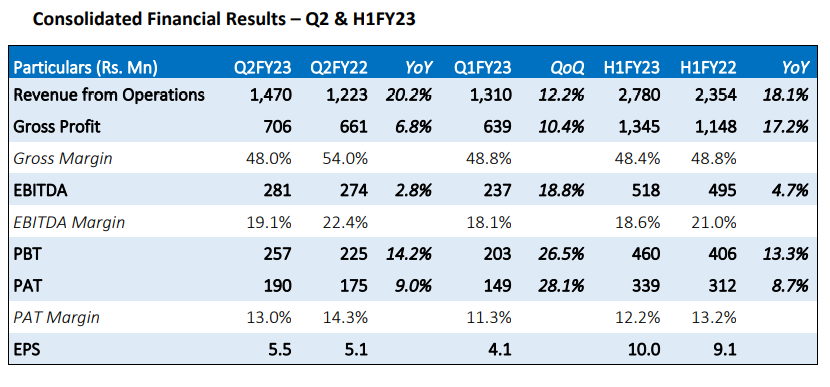

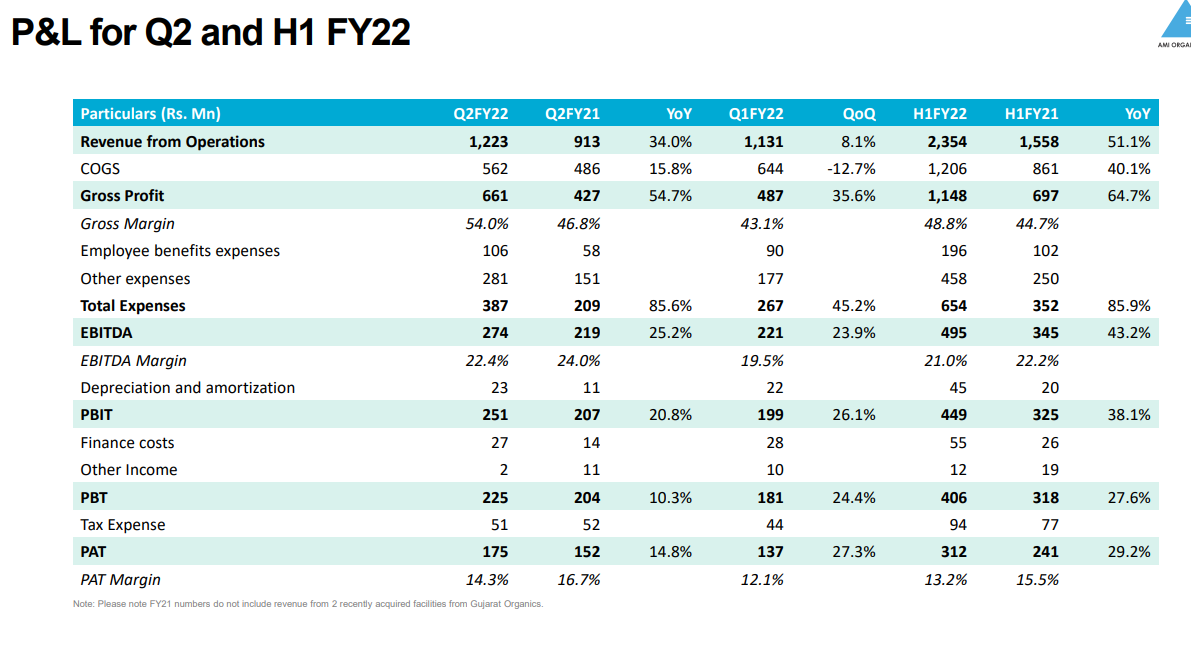

Financials

Latest PPT

Publically available broker research

Red herring prospectus

Latest management interview

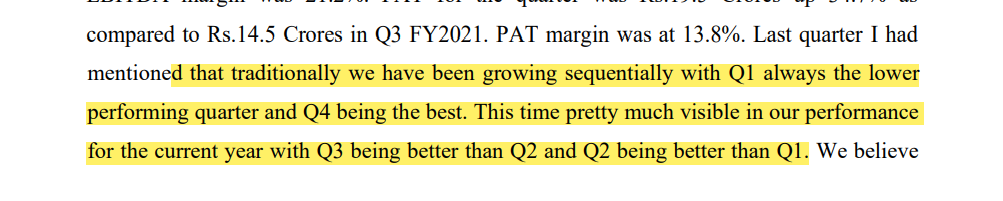

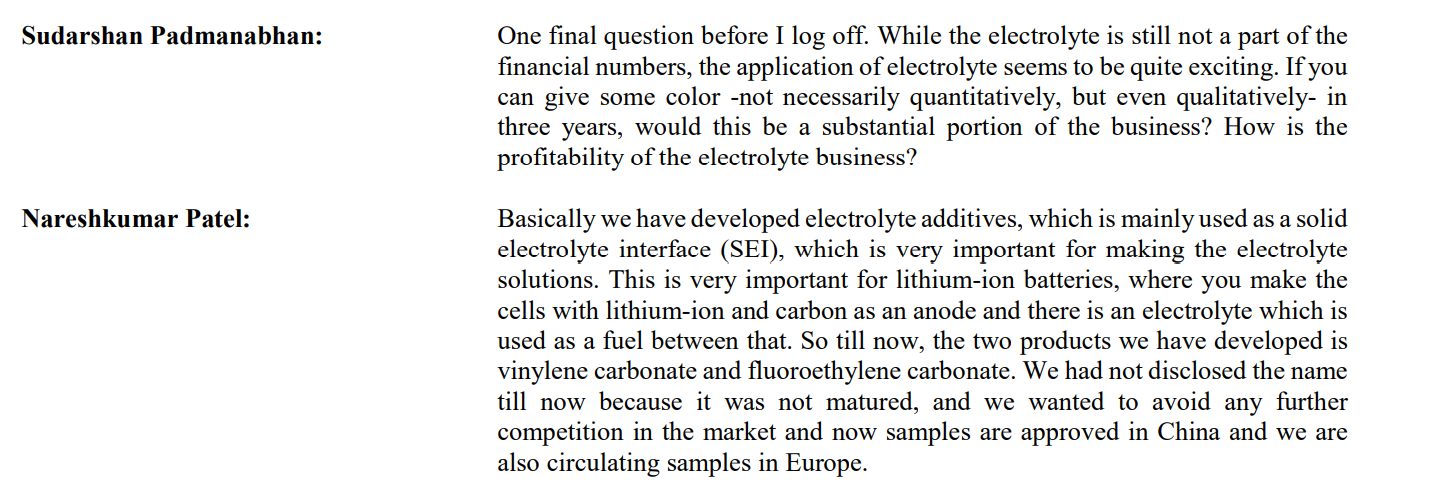

Latest results conference call transcript

Disclosure: Invested